This problem is a continuation of P533. Pie Corporation acquired 75 percent of Slice Companys ownership on

Question:

This problem is a continuation of P5–33. Pie Corporation acquired 75 percent of Slice Company’s ownership on January 1, 20X8, for $96,000. At that date, the fair value of the noncontrolling interest was $32,000.

The book value of Slice’s net assets at acquisition was $100,000. The book values and fair values of Slice’s assets and liabilities were equal, except for Slice’s buildings and equipment, which were worth $20,000 more than book value. Accumulated depreciation on the buildings and equipment was $30,000 on the acquisition date. Buildings and equipment are depreciated on a 10-year basis.

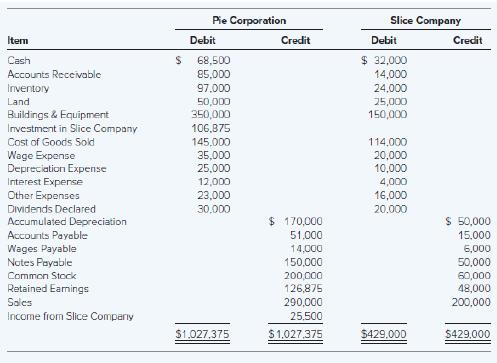

Although goodwill is not amortized, the management of Pie concluded at December 31, 20X8, that goodwill from its purchase of Slice shares had been impaired and the correct carrying amount was $2,500. Goodwill and goodwill impairment were assigned proportionately to the controlling and noncontrolling shareholders. No additional impairment occurred in 20X9. Trial balance data for Pie and Slice on December 31, 20X9, are as follows:

Required

a. Give all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20X9.

b. Prepare a three-part consolidation worksheet for 20X9 in good form.

c. Prepare a consolidated balance sheet, income statement, and retained earnings statement for 20X9.

Data from P5-33

Pie Corporation acquired 75 percent of Slice Company’s ownership on January 1, 20X8, for $96,000. At that date, the fair value of the noncontrolling interest was $32,000. The book value of Slice’s net assets at acquisition was $100,000. The book values and fair values of Slice’s assets and liabilities were equal, except for Slice’s buildings and equipment, which were worth $20,000 more than book value. Accumulated depreciation on the buildings and equipment was $30,000 on the acquisition date. Buildings and equipment are depreciated on a 10-year basis.

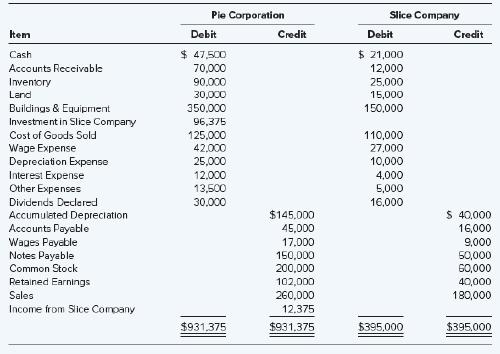

Although goodwill is not amortized, the management of Pie concluded at December 31, 20X8, that goodwill from its purchase of Slice shares had been impaired and the correct carrying amount was $2,500. Goodwill and goodwill impairment were assigned proportionately to the controlling and noncontrolling shareholders. Trial balance data for Pie and Slice on December 31, 20X8, are as follows:

Step by Step Answer:

Advanced Financial Accounting

ISBN: 9781265042615

13th International Edition

Authors: Theodore E. Christensen, David M. Cottrell, Cassy Budd