New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting financial analysis

Detecting Accounting Fraud Analysis And Ethics Global Edition 1st Global Edition Cecil W. Jackson - Solutions

The Secondary Mortgage Market Enhancement Act of 1984:(a) Allowed the GSEs (Fannie Mae and Freddie Mac) to sell MBSs (mortgagebacked securities) backed by FHA and VA loans.(b) Allowed institutional investors such as pension funds and insurance companies to invest in non-GSE guaranteed

A credit-default swap:(a) Is a form of derivative financial instrument.(b) Is a financial instrument that gives the holder of the instrument the right to receive payment from the writer of the instrument if investments in specified loans suffer defaults or losses.(c) Could give the holder of the

The Commodities Futures Modernization Act of 2000 and the repeal of the Glass-Steagall Act in 1999:(a) Effectively ended the separation of commercial banking from investment banking.(b) Ended the prevention of commercial banks from trading in securities.(c) Excluded the regulation of derivative

Which one of the following statements regarding pay-option ARM loans is not correct?(a) Some borrowers of pay-option ARM loans choose to make monthly payments that are not large enough to cover the interest that accrues on the loans each month.(b) If a borrower chooses to make monthly payments that

Which one of the following statements does not describe the transformation in Countrywide’s reported loan portfolio?(a) In 2004, conventional conforming loans dropped to 38.2 percent.(b) Subprime loans increased from 2004 to 2006.(c) By 2006, 31. 9% percent of Countrywide’s loan originations

A shift toward riskier loans could be evidenced by disclosure of an increase in the percentage of:(a) High LTV loans.(b) Pay-option ARM loans.(c) 80/20 loans.(d) All of the above.

The indications of troubled loans include:(a) Loan delinquencies.(b) Nonperforming loans.(c) Loans with negative amortization.(d) All of the above.

Which of the following attributes of loans is not an indication of an increased risk of repayment default?(a) Conforming to GSE underwriting standards.(b) Having a loan-to-value ratio of 95 percent or higher.(c) Having reduced documentation or no documentation.(d) Being a stated income loan.

Discuss the role of the government sponsored-enterprises (GSEs) in the funding and issuance of mortgage loans.

Describe the role of tranching in the granting of easy credit that fueled the housing bubble.

As the mortgage industry evolved from making loans that conformed to GSE standards to making and selling subprime loans, what were some of the changes in underwriting standards that occurred?

What is meant by negative amortization?

Explain the “reset” clause in the pay-option ARM loan agreement.

What were the main risks of pay-option ARM loans?

How were credit-default swaps expected to act as hedges against the risk of investing in mortgage-backed securities?

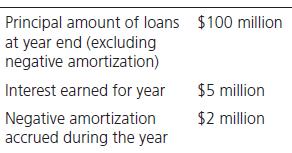

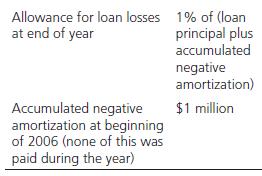

Murky Mortgage Corp. is a mortgage lender. The following information relates to Murky Mortgage’s portfolio of loans held for investment at December 31, 2006:What is the amount of loans held for investment net of allowance for loan losses on the balance sheet at December 31, 2006? Principal amount

One of the loans included in Sloppy Mortgage Corporation’s loans at January 1, 2006, was a pay-option ARM loan of \($900,000\) taken out on January 1, 2006, when the value of the house was \($900,000\).The interest earned (or accrued) on this loan for the year was \($54,000.\) The principal

Moldy Mortgage Corp. has a loan portfolio with the following loans at December 31, 2013:Moldy Mortgage wants to have an allowance for loan losses comprised of the following:0.1 percent of prime conforming loans6.0 percent of subprime 80/20 loans0.5 percent of pay-option ARM loans without negative

One of Sunbeam’s fictitious financial reporting schemes was formally recording a revenue item in the financial statements in an earlier or later period than the period in which the item should have been recorded.True/False

When a company solicits bill and hold orders from its customers and recognizes the sales in its income before delivery of the goods, this represents improper timing of revenue recognition.True/False

Acceleration of future quarters’ sales of Sunbeam into the present quarter provided a correct impression of the company’s results of operations in the present period.True/False

Revenue recognition refers to the process of recording a transaction in the financial statements, indicating that the conditions have been met for the earning of revenue.True/False

Sunbeam overstated its income by failing to maintain large enough provisions for doubtful debts.True/False

Sunbeam enticed customers to place future periods’ sales orders early and recorded these as current-period sales as part of its financial reporting scam.True/False

Despite the conditional and indeterminate nature of a sales agreement, Sunbeam still recorded sales and profit in its books of accounts.True/False

The “due diligence” study by Morgan Stanley on Sunbeam picked up information on overstocked customers and slow moving sales in the first quarter of 1998.True/False

When a previously overstated reserve is reversed in a later period, this increases operating income but not net income in the later period.True/False

For a some quarters during the time of Sunbeam’s bill and hold sales and heavily discounted sales, it reported positive operating income but negative CFFO.True/False

Sunbeam created big _________________ for the write-down of assets and for future losses or liabilities in order to boost future profits.

Sunbeam’s fictitiously recorded sale remains as accounts receivable and does not turn into _________________ like an honest sale.

Quality and track record of company leaders should be combined with an analysis of whether the business plan outlined by management is likely to produce the reported results in the published _________________ .

An indicator of illegitimately reported sales is a sudden change in the _________________ .

To coax even more orders for sales, Sunbeam increasingly gave customers the right to return goods, yet Sunbeam did not increase the _________________ for _________________ in the its accounting records.

Sunbeam’s cash flow from operations (CFFO) was negative, but at the same time the company was operating at a great profit, which signaled of inappropriately recorded _________________ .

The recording of sales when the customer has a right to return the product is a signal of the _________________ of sales.

Sunbeam captured extra sales revenue by extending its ______–______ date by two days.

With an improper use of reserves, companies usually over-accrue a liability in one period and then reduce the _________________ reserves in later periods.

When creating a false reserve, companies often recognize the future expense in the current period as a(n) _________________ charge.

Ace Company is a manufacturer of electrical appliances. The following transaction occurred near Ace Company’s December 31 fiscal year-end date:A packing case containing products costing $10,000 was found in Ace’s branch office warehouse when the physical inventory count was taken on December

Bolt Company is a clothing manufacturer.The following items relate to transactions that occurred close to Bolt’s December 31 fiscal year-end date.Item I: Merchandise costing $5,000 was shipped to a retail customer on December 27. The merchandise is part of a consignment agreement with the

Push Company is a lawn mower manufacturer.Push was falling short of meeting its sales estimates for its December 31 fiscal year end. The company expected to receive a large order for $40,000 of lawn mowers from Pull Company, a major customer, in April the next year, for goods to be delivered to

On December 20, Zee Company, an office-supply company, placed an order for goods from Papyrus Company, a paper manufacturer.Zee wanted the goods to be shipped only in March the next year (FOB destination), and a clause to that effect was included in the sales contract. Zee placed the order early to

If XYZ goes ahead and secures the backdated order and recognizes it as a bill and hold sale in its December 31 financial statements, which of the following is correct?(a) Operating income would be overstated by \($6,000,\) and sales would be overstated by \($10,000.\)(b) Cash flow from operations

If XYZ goes ahead and secures the backdated order and recognizes it as a bill and hold sale, which of the following is correct?(a) This would cause operating income to exceed CFFO by \($10,000\.(b) This would cause CFFO to be \($6,000\) smaller than operating income.(c) This would have the same

If Mac goes ahead and recognizes a sale of \($15,000\) in its December 31 financial statements for this inconclusive agreement, which of the following is correct?(a) CFFO will increase by \($15,000\).(b) CFFO will increase by \($10,000\).(c) Operating income will increase by

If Mac goes ahead and recognizes a sale of \($15,000\) in its December 31 financial statements, which of the following is correct?(a) The accounts receivable balance will be stated as \($65,000\).(b) Operating income will be stated as \($40,000\).(c) CFFO will be stated as \($39,000\).(d) Operating

With reference to Sunbeam’s financial statements, in the period that Sunbeam overstated its restructuring expense and restructuring reserves, what was the effect?(a) Increased net income.(b) Decreased total liabilities and reserves.(c) Increased operating income.(d) Decreased net income.

Which of the following was not a method used by Sunbeam to recognize future periods’ sales in current periods?(a) Inventing fictitious customers.(b) Recording contingent sales as current-period sales.(c) Offering deep discounts and extended payment terms.(d) Using bill and hold sales.

Perpetrators of improper revenue recognition schemes often attempt to offer the defense that recognizing future periods’ revenue in the current period is only a “timing” error. Discuss whether the fact that the overstated revenue will likely be earned in later periods reduces the impact of

What is the incentive for managers to overstate a restructuring reserve in the current period in order to reverse it in future periods, since overstating the restructuring reserve decreases net income in the current period?

Explain how a company’s overstatement of its restructuring reserve may not cause it to understate its operating income in the period that it overstates the reserve.

Explain why a bill and hold sale causes cash flow from operations (CFFO) to lag behind operating income.

Explain why downsizing a company by closing segments or product lines that report an accounting loss often leads to a decrease in profits rather than an increase.

Why is an “increase in accounts receivable as a percentage of sales” a signal of improper revenue recognition?

Why do overstatements of restructuring reserves sometimes cause gross margin percentages to change suddenly?

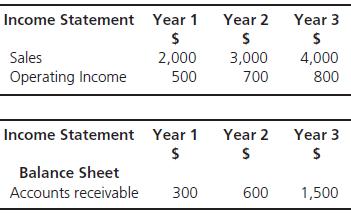

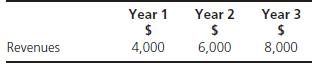

Examine these extracts from Moonshine Company’s income statement and balance sheet for the previous three years:Now calculate the ratio of accounts receivable as a percentage of sales for Years 1, 2, and 3. Income Statement Year 1 Year 2 Year 3 $ S $ Sales 2,000 3,000 4,000 Operating Income 500

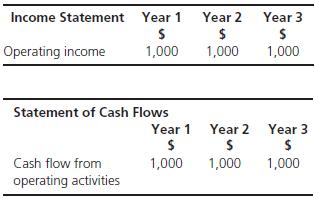

Saturn Company’s income statement for the current year shows \($100,000\) as its net income. Its depreciation expense is \($5,000\).The only changes to its working capital balances over the last year were that accounts receivable increased by \($40,000,\) inventory decreased by \($10,000,\) and

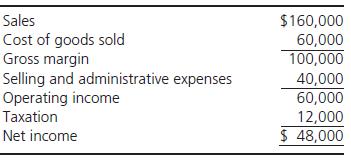

Before finalizing its financial statements for the year, Jupiter Company decides to create a restructuring reserve of $20,000 in preparation for a downsizing to be implemented the following year. Jupiter’s income statement for the year before it created the restructuring reserve was as

A leading sign of an overstatement of sales in Sensormatic’s fictitious reporting schemes is the increase of accounts receivable as a percentage of sales.True/False

Sensormatic also overstated its revenues by shipping goods before the customer needed them and instructing the carrier to delay delivery.True/False

Sensormatic overstated its earnings by creating false reserves in one period and reversing those reserves into earnings in future periods.True/False

In Sensormatic’s case, it is normal for the company to operate at a profit even if it is not generating a CFFO at a similar pace.True/False

Xerox was able to increase its reported earnings fictitiously by changing estimates of residual values of the leased assets through the choice of a particular discount rate.True/False

Xerox had sold approximately $400 million of its accounts receivable in order to reduce the reported CFFO.True/False

If Xerox’s revenue recognition is delayed over the life of the contract, it could be a signal that the company is trying to shift its revenue to accelerate its recognition.True/False

When a company sells its accounts receivable, it is important to deduct the amount received on the sale from CFFO before comparing CFFO to operating income when looking for signals of overstatement of revenues.True/False

When a company overstates its earnings via the use of top-side adjustments, the general ledger balances do not reflect the amounts shown in the financial statements.True/False

Insignia’s understatement of its allowance for returns is an example of improper valuation of revenue.True/False

According to AAER 1017, at Sensormatic shortly before midnight on the last day of the quarter, the computer system that ___________ and ___________ shipments was manipulated to change the date and time on the computer clock.

Sensormatic shipped goods that customers had ordered for the next period to Sensormatic’s own ___________ at the end of the current period.

Xerox presents an example of the misuse of multiple-element contracts or ___________ contracts.

For sales-type leases, GAAP requires the financing revenue to be recognized over the of the ___________ .

When CUC precisely ___________ analysts’earnings and revenue expectations quarter after quarter, it is often a sign that things may be too good to be true.

When CUC’s major expense items remain identical quarter after quarter as a percentage of revenues, it is a signal that the reported expenses and revenues are being ___________ .

A significant decrease in Insignia’s allowances for returns as a percentage of sales is a signal that the allowance for returns may be ___________ .

Insignia’s financial statements reporting a change in accounting policy, with respect to the method of recognizing the ___________ or any changes in estimates for returns, that lead to decreasing the allowance indicates a fictitious reporting scheme.

In a company that sells membership subscriptions, deferred revenue ___________ as a percentage of total revenue is an indication that the company may be overstating revenues.

Insignia subtracted its allowance for ___________ from its gross revenue to arrive at net revenue.

Sensormatic’s overstatement of earnings via holding its books open after the close of a reporting period is an example of:(a) Recording fictitious revenue.(b) Improper timing of revenue.(c) Improper valuation of revenue.(d) None of the above.

Xerox’s bundled sales were improperly recorded in its financial statements because:(a) All of the revenue streams for its leases should have been recorded over the life of the leases.(b) Some of the revenue relating to the finance charges included in monthly lease payments over the life of the

Sensormatic instructed employees to withhold certain bills of lading from the auditors because of:(a) Indication of a practice of unrealized revenue recognition.(b) Improper recognition of revenue on out-of-period shipments.(c) Intention to disguise revenue that should not be recorded in the

One of the signals of Xerox’s fictitious reporting is the lagging of CFFO behind net income, and it should be flagged through the following activities:(a) Reduction in CFFO, from 25% of net income in 1995 to 18% in 1997.(b) In 1998, a negative CFFO of \($1,165\) million was generated compared to

CUC’s use of top-side adjustments to overstate its earnings is an example of:(a) Improper timing of revenue recognition.(b) Recording of fictitious revenue.(c) Improper valuation of revenue.(d) None of the above.

When CUC transferred some amounts for deferred club membership revenues to current period revenues, it had the following effect on CUC’s financial statements.(a) Increasing the deferred revenue amount on the balance sheet.(b) Decreasing the prepaid asset amount on the balance sheet.(c) Decreasing

According to the SEC’s AAER, which of the following was a method used by CUC to overstate its earnings?(a) Falsification of sales documents.(b) Side agreements with customers that were not recorded.(c) Creation of cookie-jar merger reserves.(d) All of the above.

Insignia’s understatement of its allowance for returns is an example of overstating revenue via:(a) Improper valuation of revenue recognition.(b) Improper timing of revenue recognition.(c) Recording of fictitious revenue.(d) None of the above.

Another sign of Xerox’s fictitious reporting scheme is that the notes to the financial statements reflect the following:(a) Reclassification of revenue stream.(b) Change in the estimates of discount rates.(c) Change in the estimates of the residual values.(d) All of the above.

When Xerox factored or sold its accounts receivable to avoid reclassifying them as operating leases instead of sales-type leases, this had the effect of:(a) Decreasing the amount of revenue it reported.(b) Increasing the amount of revenue it reported.(c) Decreasing its reported CFFO.(d) None of the

Issuers of financial statements that fail to disclose that accounts receivable have been sold or factored sometimes attempt to offer the defense that this is only a disclosure issue that does not affect earnings.If the nondisclosure of the sale of accounts receivable does not affect earnings, does

Xerox sold $400 million of its South American lease agreements. Explain Xerox’s possible incentive for selling those accounts receivable.

If a company sells or factors a material portion of its accounts receivable, what adjustments must you make to accounts receivable before doing your test to see whether the financial statements contain any signals indicating an overstatement of sales? Explain why.

Explain why overstating sales by holding books open after the close of a period would cause CFFO to lag behind operating income.

If a company sells a significant portion of its accounts receivable, what adjustments must you make to CFFO before testing whether the financial statements contain signals of overstatement of earnings?Explain why these adjustments should be made.

Why are multiple-element lease contracts a fertile ground for overstating revenue?

Explain how deferred revenue can be misused to overstate earnings.

XYZ Co. is an equipment leasing company.The following is an extract from its income statement for the previous three years.The following is an extract from XYZ’s notes to its financial statements:Note: Revenues All revenues reported are in respect of sales type leases. Included in the majority of

Examine the following extracts from Blake Co.’s income statement and balance sheet for the previous three years.You also read in the financial press that Blake Co. sold $2,000 of its accounts receivable in year 3.Requireda. Calculate the ratio of accounts receivable as a percentage of sales for

Examine these extracts from Collin Company’s income statements and statements of cash flow for the previous three years.You also read in the notes to the financial statements that Collin Company sold $1,000 of its accounts receivable in year 3.Adjust for the sale of accounts receivable in year 3

Bowie and Velasquez discussed ethical issues, which are uncertainties and the ability to execute a project during decision making.True/False

Ethical evaluation is considered a waste of time when the project is forecast to succeed.True/False

Showing 500 - 600

of 858

1

2

3

4

5

6

7

8

9

Step by Step Answers