Question: For Example 9.15, experiment with the Holt-Winters Additive Model for Seasonality and Trend spread-sheet model to find the best combination of , , and

For Example 9.15, experiment with the Holt-Winters Additive Model for Seasonality and Trend spread-sheet model to find the best combination of α, β, and γ to minimize MSE.

Data from Example 9.15

We will use the data in the Excel file New Car Sales, which contains three years of monthly retail sales data. Figure 9.20 shows a chart of the data. Seasonality exists in the time series and appears to be stable, and there is an increasing trend; therefore, the Holt-Winters additive model with seasonality and trend would appear to be the most appropriate model. We arbitrarily select α = 0.3, β = 0.2, and γ = 0.9. Figure 9.21 shows the Excel implementation (Excel file Holt Winters Additive Model for Seasonality and Trend). The level and seasonal factors are initialized using formulas (9.13) and (9.14). The trend factors are initialized using formula (9.22):

bt = [(42,227 - 39,810)>12 + (45,422 - 40,081)>12 + ... + (49,278 - 44,186)>12]>12 = 462.48, for t = 1, 2, ..., 12

Using Equation (9.20), the forecast for period 13 is

F13 = a12 + b12 + S1 = 45,427.33 + 462.48 + (-5,617.33) = 39,810.00

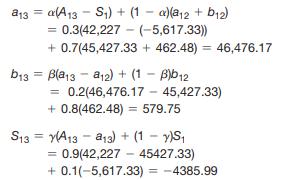

We may now update the parameters based on the observed value for period 13, A13 = 42,227:

Other calculations are similar. To forecast period 37, we use formula (9.21):

F36 + 1 = a36 + b36(1) + S36 - 12 + 1 = 49,267 units

Notice from the chart that the additive model appears to fit the data extremely well. Again, we can easily experiment with different values of the smoothing constants to find a best fit using an error measure such as MAD or MSE.

a13 a(A13 S) + (1 a)(a12 + b12). 0.3(42,227-(-5,617.33)) - +0.7(45,427.33 + 462.48) 46,476.17 b13= B(a13a12) + (1-B)b12 = = 0.2(46,476.17 - 45,427.33) +0.8(462.48) = 579.75 S13 (A13a13) + (1 - y)S = 0.9(42,227-45427.33) +0.1(-5,617.33) = -4385.99

Step by Step Solution

3.39 Rating (149 Votes )

There are 3 Steps involved in it

02 02 1 Month Period t Units Level a Trend b Seasonality S Forecast F MSE Jan 1 39810 4542733 46248 561733 Feb 2 40081 4542733 46248 534633 Mar 3 47440 4542733 46248 201267 Apr 4 47297 4542733 46248 1... View full answer

Get step-by-step solutions from verified subject matter experts