New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

finance with monte carlo

International Finance 5th Edition Maurice D Levi - Solutions

9. What is meant by weak-form, semi-strong form, and strong-form market efficiency?

8. Why is doing nothing when importing or exporting tantamount to speculation on exchange rates?

7. How would you short the euro via a swap?

6. What is required to go long in euros vis-à-vis the US dollar via a swap?

5. What is the main advantage of options versus forwards or futures as an instrument of currency speculation?

4. Are futures more or less liquid than forwards for a currency speculator?

3. Taking into account transaction costs,what does a speculator compare when deciding whether to go short in a particular foreign currency via a forward contract?

2. Taking into account transaction costs, what does a speculator compare when deciding whether to go long in a particular foreign currency via a forward exchange contract?

1. Why are speculation, market efficiency, and forecasting closely related issues?

8. Suppose that as the money manager of a US firm you faced the following situation:n rB$9.0%n rI$ 8.0%n rB C$ 10.5%n rI C$ 9.5%n S(C$/ask$) 1.0400 n S(C$/bid$) 1.0350 n F1(C$/ask$) 1.0600 n F1(C$/bid$) 1.0550 Here, rB$and rI$ are the one-year interest rates at which you can, respectively, borrow

7. Assume that you are importing German transformers and that you face the following:n rB$6%n rIÛ 4%n S($/askÛ) 1.5000 n F1–2 ($/askÛ) 1.5400a. How would you hedge? Would you buy euro forward or would you borrow dollars, buy euro spot, and invest in euro for six months?b. Would it make any

6. Why is the cost of forward hedging half of the difference between the forward bid–ask spread and the spot bid–ask spreads?

5. If a currency can be sold forward for more than the currency’s expected future value because of a risk premium on the currency, do the sellers of that currency enjoy a “free lunch”?

4. It has been said that expected bankruptcy costs can help explain the use of equity versus debt in corporate financial structure, even though interest but not dividends are tax deductible. Can bankruptcy costs also explain hedging practices that on average reduce expected earnings?

3. Why might managers’ motivations to hedge against foreign exchange exposure differ from those of company shareholders?

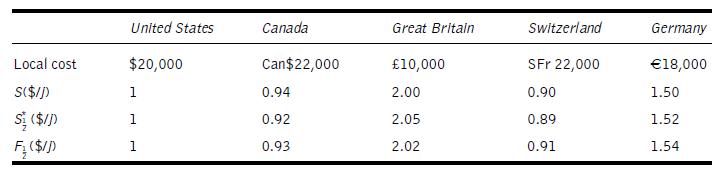

2. Suppose that you were importing small electric transformers, that delivery from all suppliers would take approximately six months, and that you faced the situation shown in the table below:a. Where would you buy if you decided on forward hedging?b. Where would you buy if you decided on being

1. In what sense are the forward risk premium and the bid–ask spread on forward contracts both related to risk?Does the fact that the bid–ask spread is always positive and yet the forward risk premium can be positive or negative suggest that the nature of the two risks is different?

14. Why do you think financial engineering has been referred to as a “LEGO© approach” to decision-making?

13. What is meant by “sourcing”? Should this be used as a method of hedging foreign exchange exposure?

12. Name two composite currency units.

11. What is a composite currency unit?

10. Can importers and exporters both hedge by selecting the currency of invoicing, and are there any compromise invoicing currency strategies?

9. What type of swap would an American importer of Japanese yen-invoiced products use?

8. How does the risk of hedging via futures compare to that of hedging via forward exchange?

7. Would a typical hedger be willing to pay a risk premium in order to hedge by buying foreign currency forward?

6. How does the expected cost of hedging forward relate to spot versus forward exchange-rate spreads?

5. Why might expected bankruptcy costs be higher for firms that do not hedge than for those that do?

4. What types of products might enjoy higher sales when managers hedge foreign exchange exposure?

3. Are there informational gains to managers if they hedge foreign exchange exposure? How might the information be obtained without hedging?

2. How is the manager versus shareholder hedging choice influenced by economies of scale when buying or selling forward exchange?

1. How is the manager versus shareholder hedging choice influenced by progressivity of the corporate income tax rate?

15. Due to the North American Free Trade Agreement, NAFTA, the operations of many firms are more integrated across the continent with, for example, manufacturers sourcing parts from US, Canadian, and Mexican factories.How might such integration influence operating exposure of a firm that integrates

14. The “maquiladoras” are manufacturing facilities located on the Mexican side of the US–Mexican border, including factories owned by US firms assembling goods for sale in the United States. What factors influence the size of operating exposure of these maquiladoras for their US parent

13. What would the availability of very close substitutes for an import mean for the e1asticity of demand of the firm that competes with imports? Who will bear the burden of devaluation in this case?

12. Reconcile a rising domestic currency price and a falling foreign currency price for an imported good after a devaluation of the domestic currency. Why does this mean that the domestic currency price rises by less than the percentage of devaluation?

11. Redraw Figures 14.6 and 14.7 to show the effect of a revaluation on revenues, costs, and profits.

9. Redraw Figure 14.2 to show the effect of devaluation-induced cost increases when amounts are measured in foreign currency.10. Why does devaluation simultaneously raise export prices as measured in home currency and lower them as measured in foreign currency?

8. Redraw Figure 14.4 to show the effect of a revaluation of the dollar on a US exporter selling in an imperfectly competitive market.

7. Redraw Figure 14.2 to show the long-run effect of a dollar revaluation on the profits of a perfectly competitive US exporter.

6. Redraw Figure 14.2 to show the short-run effect of a dollar revaluation on the profits of a US exporter that sells in a competitive market.

5. As in Question 4, assume that Aviva’s jeans face an elasticity of demand of –2 with constant costs, and assume also approximately half the total cost is accounted for by denim cloth,which is imported.To an approximation, what will this mean for your answers in Question 4?

4. Assume that the elasticity of demand for Aviva’s jeans is –2. Assume that production costs are constant and that there is a 10 percent dollar depreciation.a. By how much will the quantity sold increase?b. By how much will dollar revenues increase?c. By how much will foreign exchange revenues

3. Do you think that the United States is a sufficiently large importer of products in general so that the effect of a dollar depreciation would be eliminated by pressure on nominal wages from tradable-goods price increases? How about Canada, Fiji, or Iceland?

2. Rank the industries in Question 1 according to the effects of a devaluation/depreciation on profits. You may assume that there are different amounts of tradable inputs, different elasticities of demand, and so on.

1. Rank the following export industries according to the amount of increase in sales volume you would expect to result from a fall in the value of the US dollar.a. wheat farming;b. automobile production;c. foreign travel to the United States;d. computer hardware.Use diagrams in your answers.

15. What happens to an importer’s total revenue after a devaluation of the importer’s currency?

14. What happens to the quantity imported after a devaluation of the importer’s currency?

13. How does change in domestic currency price of an import compare to the size of devaluation?

12. How does the effect of a revaluation on an importer’s domestic currency price depend on the elasticity of demand for the product that is imported?

11. Why might an exporter care about the effect of a change in an exchange rate on the exporter’s revenue, cost, and profit measured in terms of the currency of the buyer of the exporter’s product?

10. Does the exporter’s demand curve shift after devaluation when the curve is drawn against the exporter’s home currency, and if not, what does happen?

9. Does the demand curve for an imperfectly competitive firm’s product shift after devaluation if the demand curve is drawn against the currency of the buyer, and if so how does it shift?

8. How is exposure of a perfectly competitive exporter affected by the exporter’s country being and remaining only a tiny part of the world supply of the product the exporter sells?

7. How does the importance of tradable versus non-tradable inputs affect an exporter’s exposure?

6. How does free entry in an industry affect operating exposure in the short run versus the long run?

5. How does an exporter’s operating exposure depend on the flexibility of production?

4. In what way does an exporter’s operating exposure depend on the elasticity of demand facing the exporter?

3. Are all imported inputs “tradable”?

2. What is a “tradable input”?

1. What is meant by “operating exposure”?

10. Redo the analysis in this chapter of the effect of exchange-rate changes on an exporter by allowing the quantity sold,q, to change with the exchange rate instead of holding it constant.Use calculus to make the problem easier, and note that pUK and q should be at profit-maximization levels in

9. By studying the stock price of a US-based publicly traded company you have noticed that when the dollar drops against various currencies the company’s value on the stock exchange increases. By averaging the link between exchange rates and the company’s value you have determined the size of

8. Would the distinction between real and actual changes in exchange rates be important if inflation and interest rates were everywhere the same and were also small?

7. If a company has used its currency of debt denomination and/or forward contracts to make its exposure zero, what would measured exposure be from the b of a regression line, if in calculating b the debt and/or forward contracts were omitted from the regression equation?

6. What is the problem in using the standard deviation of exchange rates as a measure of foreign exchange risk?

5. Would it make sense to add a firm’s exposures in different currencies at the spot exchange rate to obtain a measure of the firm’s aggregate exposure? If not, why not?

4. How does PPP relate to:a. Exposure on real, fixed assets?b. Operating exposure?

3. If the Bank of Canada “leans against the wind,” which means increasing interest rates when the Canadian dollar depreciates and lowering interest rates when the Canadian dollar appreciates,what would this mean for the exposure ofa. Canadian residents holding Canadian dollar-denominated

2. How can exposure exceed the face value of a foreign currency-denominated asset or liability?

1. In what sense is the sign – positive versus negative – of the slope coefficient which measures exposure relevant for exposure versus risk, and in what sense is it irrelevant?

12. How does operating exposure relate to the PPP condition?

11. How does foreign exchange exposure on real assets relate to the PPP condition?

10. Can a domestic currency-denominated asset face foreign exchange exposure?

9. Can an asset face exposure larger than the foreign currency value of the asset?

8. What is “foreign exchange risk”?

7. How does the sign associated with exposure – positive versus negative – relate to whether exposure is “long” or“short”?

6. What are the units of measurement of exposure to a particular exchange rate: for example, euros per US dollar?

5. What variables go on the axes of an “exposure line”? How do these variables relate to those used for drawing payoff profiles?

4. What is meant by a “systematic relationship”?

3. What is a “reference currency”?

2. What is a contractual asset or liability?

1. What is “foreign exchange exposure”?

5. Would it be easier to cure the joint problems of unemployment and inflation when international capital flows are extremely sensitive to interest rates rather than being insensitive to interest rates?

4. Would it be easier to cure the joint evils of unemployment and inflation with flexible exchange rates than with fixed (pegged) exchange rates?

3. If your company produces nontraded goods such as newspapers and local magazines,would you expect a sales increase or cost increase to result from a devaluation of the currency in your country? Could you be hurt by devaluation?

2. If international capital flows are very sensitive to changes in interest rates, how would the BB curve compare to the situation where international capital flows are insensitive to interest rates?

1. If you were an exporter,would you expand your productive capacity if the government in an export market began to use an expansionary monetary policy and the exchange rate was fixed? Would you expand capacity after the introduction of an expansionary monetary policy if the exchange rate was

6. What policy mix would you adopt to correct unemployment and a balance-of-payments deficit?

5. Can devaluation or import tariffs/export subsidies increase employment?

4. With flexible exchange rates, does fiscal policy work?

3. With fixed exchange rates, does fiscal policy work?

2. With flexible exchange rates, does monetary policy work?

1. With fixed exchange rates, does monetary policy work?

16. Do you think that problems might arise out of a difficulty for Americans to accept a relative decline in economic power? What form might these problems take?

15. Which argument for fixed exchange rates do you think would be most compelling for Fiji? [Hint: Fiji’s major“export” is tourism, and most manufactures and other consumer goods are imported.]

14. Why have central bankers frequently intervened in the foreign exchange market under a system of flexible exchange rates? If they have managed to smooth out fluctuations, have they made profits for their citizens?

13. Do you think North America should adopt a common currency?

12. Do you think that coastal China and western China should have separate currencies?

11. Why do you think some European countries maintained pegged exchange rates after the collapse of the Bretton Woods system? Relate your answer to optimum currency areas?

10. How would you go about trying to estimate the seigniorage gains to the United States? [Hint: They depend on the quantity of US dollars held abroad,the competitive rate of interest that would be paid on these, and the actual rate of interest paid.]

Showing 100 - 200

of 485

1

2

3

4

5

Step by Step Answers