New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

integrated accounting

Fundamentals Of Oil And Gas Accounting 4th Edition Rebecca A. Gallun, Ph.D. Wright, Charlotte J, Linda M. Nichols, John W. Stevenson - Solutions

Tyler Company operates the Salt Creek Field. Along with oil this field produces large quantities of saltwater. The saltwater is highly corrosive and, as a result, the downhole production equipment is subject to frequent replacement. During the first half of 2004, Tyler must replace the tubulars in

Mr. Davis owns the mineral rights in some land in Texas. He leases the land to Aggie Oil Company, reserving a 1/ 5 royalty. During 2006, Aggie Oil Company makes the following assignments:a. To Mr. Jones, an ORI of 1/7 of Aggie’s interest.b. To Mr. Brown, a PPI of 30,000 barrels of oil to be paid

Blow Out Oil Company owns 100% of the WI in Lease A. Lease A is burdened with a 1/6 royalty. During the month of June, 12,000 barrels of oil were produced and sold.Assume the selling price of the oil was $24/bbl and the production tax was 5%. Give the entry required to record the sale of the oil

Ebert Oil Company sold 1,000 Mcf of gas at \($3.00/Mcf.\) The lease provides a 1/5 RI. The WI owner receives 100 percent of the revenues (net of 5% severance tax) and then distributes the amount due to the RI owner. Give the entry by Ebert to record the sale of the gas.

Deep Hole Oil Company used 100 Mcf of gas obtained from Lease A and valued at \($2.10/Mcf\) for gas injection on Lease B. Assume production taxes are 5% and the RI on Lease A is a 1/6 RI.a. Give the entry necessary to record the transfer of the gas.b. Give the entry assuming 100 percent of the gas

Fortunate Oil Company sold or used the gas produced on Lease A during January as follows:a. 300 Mcf used as fuel to operate lease equipment.b. 800 Mcf sold to R Company at \($3/Mcf.\)Assume a 1/ 7 RI and a production tax of 5%, and assume that the lease agreement has a free fuel clause, but

Big John Oil Company purchased 200 barrels of oil from JD Operator. The gross value of the oil was \($5,000.\) The severance tax rate was 4 percent. Give the entry to record revenue for JD, assuming Big John disbursed the royalty and remitted all taxes and assuming a division order as follows:

Gusher Oil Company has a working interest in a property. In addition to the 1/5 royalty, Gusher agreed to pay the royalty owner a minimum royalty of \($400\) per month. Gas production on the lease began in the third month after the lease contract was signed. Total sales revenue during the third

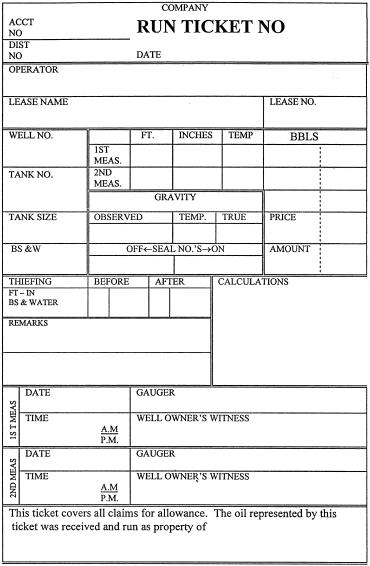

Complete the run ticket on p. 341 and give the entry to record the sale of the oil at \($30/bbl\) assuming a severance tax rate of 5% and a 1/5 RI. Use the tables given in the chapter. The tank number is 1, the observed temperature is 73° and the observed gravity is 33°. The first tank

Information from a run ticket shows that 1,000 net barrels of oil with an API gravity of 36° were sold. The selling price is based on a contract price of \($22\) per barrel, adjusted downward 4¢ for each degree of gravity less than 40. Compute the selling price for the 1,000 barrels. 2ND MEAS IST

Cameron Oil Company produced 2,000 barrels of oil in June 2007. The expected selling price was \($20\) per barrel. The purchaser pays the severance taxes and the royalty interest owner and remits the remainder to Cameron Oil. The royalty interest is 1/5 and the severance tax rate is 10%.a. Prepare

Whitmire Oil Company owns a working interest in the Carpenter Lease in Texas. The lease is burdened with a 3/16 royalty interest. During February, 3,000 bbl of oil are sold at \($22/bbl\) to a refinery owned 100 percent by Whitmire Oil. Assume the severance tax rate is 5% in Texas.Prepare entries

Cameron Oil Company operates Leases X and Y. Cameron Oil transfers 50 barrels of oil from Lease X to Lease Y to be used as fuel on Lease Y. The current spot oil price is \($22/bbl\) and the severance tax rate is 5%. Cameron owns 100% working interests in Lease X and Lease Y. Lease X has a 1/8

Stephens Oil Company produces 2,000 bbl of oil in June that is sold in July. The posted field price and the actual selling price is \($22/bbl.\) The severance tax rate is 5%. The purchaser of the oil will pay the severance tax to the state and also will pay the royalty interest owner. The royalty

Knight Oil Company has the following transactions in 2006.a. Minimum royalty payments of \($200\) per month are paid during the months of January through March. The minimum royalty payments are recoverable from future royalty payments.b. Production was sold in April 2006, and the royalty payable in

Mr. Dube owns some mineral rights in Texas that he leases to Seagull Oil Company, reserving a 1/8 royalty interest. During 2006, Seagull Oil made the following assignments:a. To Mr. Hall, an ORI of 1/6.b. To Mr. Irwin, a PPI of 10,000 barrels of oil to be paid out of 1/5 of the working interest’s

Joyner Oil Company sells 10,000 Mcf of gas at \($1.50/Mcf.\) The lease provides for a 1/6 RI, and the WI owner has distributed an ORI of 1/10. The severance tax rate is 7%.Record the entries for the RI owner, ORI owner, and WI owner, assuming:a. The purchaser assumes responsibility for distributing

Gusher Oil Company’s production for Leases A and B is gathered into a common system and sold. Total Sales for the month are 6,562 barrels. Assume the following data for Leases A and B:Measured production from Lease A is 3,300 barrels and 3,500 barrels from Lease B.REQUIRED:a. Allocate production

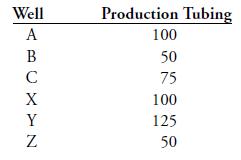

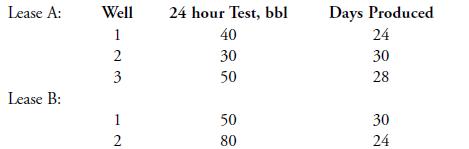

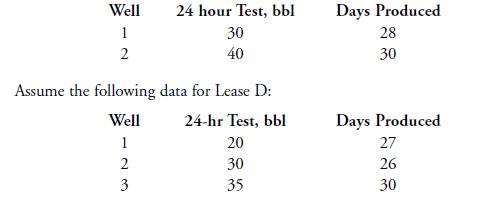

Dube Company’s production from each well on Lease C and Lease D is estimated based on a 24-hour test. Oil produced from each well on each lease is commingled and measured before leaving each lease. The oil produced from each lease is then commingled and delivered to a central tank battery. Assume

Cameron Company and Adams Company own 70% and 30% of the WI of the Dowling Field, respectively. There is a 1/8 royalty owner. The 1/8 royalty is shared proportionally by Cameron and Adams. Cameron and Adams agree that Cameron’s purchaser will take March’s gas production and Adam’s purchaser

Ramsey Company has a 100% WI in some property in Texas. The property is burdened with a 1/8 royalty. Ramsey produces and sells a total of 130,000 Mcf of gas from the property during July. Of the 130,000 Mcf, 50,000 Mcf of gas is sold to a pipeline for \($2.00/Mcf.\) Ramsey sells the remaining

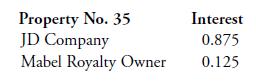

Fossil Oil Company has production on a lease in Louisiana with the following ownership interest: RI—1/5 RIORI—1/ 16 of 4/ 5 of gross productionJoint WI: Lomax Company (40%) and Fossil Company (60%)During April, 10,000 barrels of oil (after correction for temperature, gravity, and BS&W)were

Churchwell Company, a successful-efforts company located in California, sold 2,500 Mcf of gas with a heat content of 1.030 MMBtu/Mcf. The selling price of the gas was \($2.00\) per MMBtu.REQUIRED:a. Determine the MMBtu’s for the gas sold.b. Determine the total sales price.c. Determine the unit

During September, 2010, Fortunate Oil Company sold 2,000 Mcf of gas at 14.65 psia with a heat content of 1.030 MMBtu/Mcf at 14.73 psia. The selling price of the gas was \($2.20\) per MMBtu.REQUIRED:a. Convert Mcf to a standard pressure of 14.73 psia and determine the MMBtu’s for the gas sold.b.

Fossil Field is jointly owned by Allen Company (70% WI) who acts as field operator, and Garza Company (30% WI). There is a 1/6 royalty. The 1/6 royalty is shared proportionally by Allen and Garza. The two working interest owners have agreed that Allen’s purchaser will take gas produced in July

Sherwood Field, located in East Texas, is jointly owned by Kelly Company (60%) and Tiger Company (40%). Kelly, who is the operator, estimates that gas production during July will be 40,000 Mcf. Kelly Company makes confirmed nominations of 30,000 Mcf and Tiger Company makes confirmed nominations of

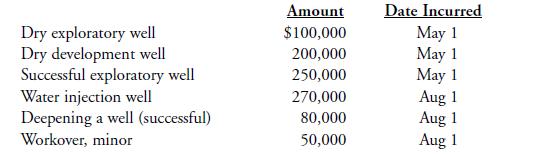

Basic Oil Company incurred intangible costs during 20XA related to the following:a. Assuming Basic is an independent producer, how much IDC can it deduct for 20XA?b. How much IDC could Basic deduct as an integrated producer? Amount Date Incurred Dry exploratory well $100,000 May 1 Dry development

On January 1, 20XA, Core Oil Company bought a developed lease for \($300,000.\) During 20XA, Core Oil Company incurred \($600,000\) of IDC. Reserves of 400,000 barrels were discovered, and 100,000 barrels were produced and sold. Gross income from production was \($2,000,000.\) On January 4, 20XB,

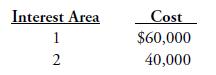

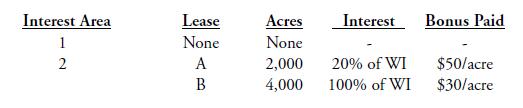

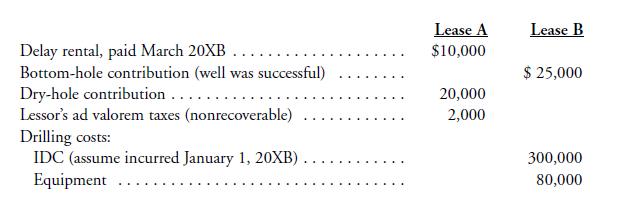

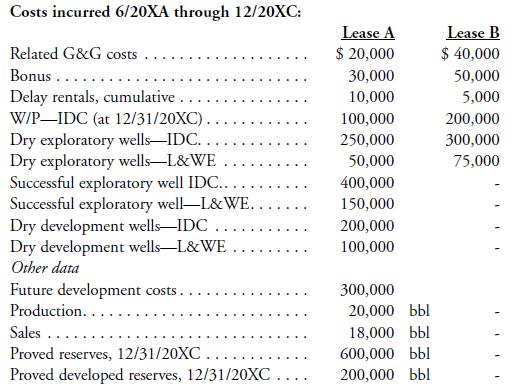

During 20XA, Gravity Oil Company incurred G&G costs of \($20,000\) for Project Area 15. Two areas of interest were identified. Detailed seismic studies were conducted on the areas of interests at the following costs:As a result of the detailed seismic studies, the following leases were

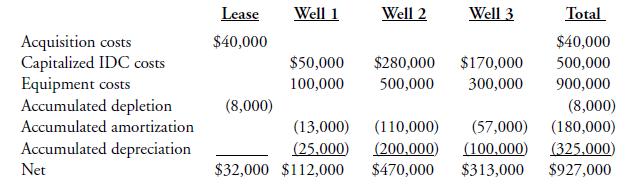

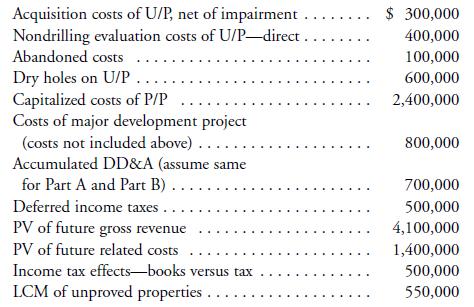

Universal Oil Company, an independent producer, began operations in June 20XA.During the first 21/2 years of operation, Universal acquired only two U.S. properties, which were noncontiguous. Costs incurred on those properties during that 21/2 years are given below, net of accumulated DD&A.

How does amortization of leasehold costs differ under the three methods? Include in your answer a discussion of the reserves used (PR or PDR), which costs are amortized, and the cost center used (i.e., are property costs amortized separately or by some type of grouping?).

Hard Times Oil Company, an integrated producer, has an unproved property with acquisition and capitalized G&G costs of \($35,000.\) Hard Times also has a proved property with the following costs:Determine the amount of the tax loss in each of the following situations:a. Hard Times drilled a dry

On March 1, 20XA, Jerry Barnes purchases mineral rights for \($30,000.\) On June 1, 20XA, he leases the mineral rights to Brown Oil Company retaining a 1/5 royalty interest. Brown Oil Company pays Barnes a lease bonus of \($10,000.\) On June 1, 20XB, a delay rental of \($1,000\) is received by

Jones Oil Company paid the following amounts in 20XD:Determine the tax basis of any assets and the amount of any tax deductions. Shut-in royalty payments (not recoverable).. Shut-in royalty payments (failure to make payments terminates lease) $1,200 4,000

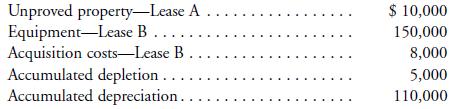

Davenport Energy Company, an independent producer, has the following account balances at 1/1/20XA:Determine the amount of the tax loss on the following dates:a. On March 1, 20XA, the unproved property is abandoned.b. On April 2, 20XA Lease B is abandoned with salvageable equipment in the amount of

Aggie Oil Company has the following information:The lease is subleased to Acme Oil Company for \($300,000,\) and Aggie retains an 1/16 ORI. At the date of the sublease, the FMV of the equipment is 180,000.REQUIRED: Determine the tax basis of Aggie’s and Acme’s assets and the amount of any tax

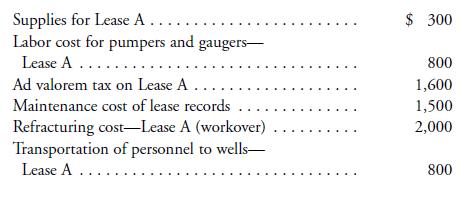

During 20XB, Dixie Company incurs the following costs relating to Lease A, a producing property: Supplies for Lease A...... Labor cost for pumpers and gaugers- Lease A..... Ad valorem tax on Lease A.. Maintenance cost of lease records Refracturing cost-Lease A (workover) Transportation of personnel

Aggie Oil Company, an independent producer, has average production from Lease A of 100 barrels per day in 20XA from Lease A. The average selling price of oil in 20XA is \($23\) a barrel. Net income from Lease A in 20XA is \($325,000\) and taxable income of the company is \($800,000.\)Compute

Define the following:a. IDCb. elected capitalized IDCc. sublease

Dowling Company, an integrated producer, incurs IDC costs in the following years as indicated. The IDC marked with an asterisk (*) relate to dry hole IDC.REQUIRED: Compute the amount that may be deducted for IDC in the years 20XA, 20XB, 20XC, and 20XD. Date Date Incurred Amount Incurred Amount

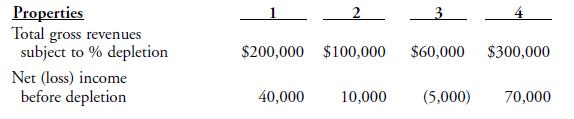

Isaac Company owns and operates four oil and gas properties that are classified for tax purposes as four separate properties. Data for the four properties are presented below:REQUIRED: Compute the amount of percentage depletion that could be deducted on Isaac’s tax return. Properties Total gross

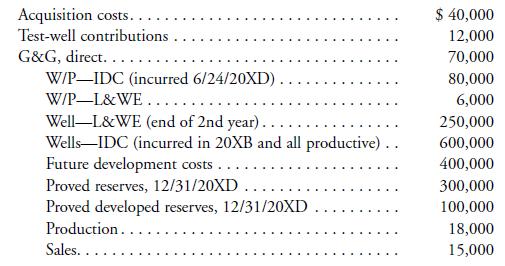

Aggie Oil Company owns only one lease in the United States, Lease Q. The following information for Lease Q, which is burdened with a 1/6 royalty, is as of 12/31/20XD. All reserve, production, and sales data apply only to Aggie Oil Company.Additional data: Aggie also placed in service on 8/1/20XB a

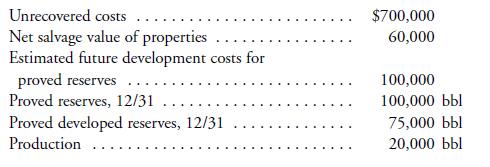

Given the following, compute DD&A, assuming no exclusions from the amortization base. Unrecovered costs Net salvage value of properties Estimated future development costs for proved reserves Proved reserves, 12/31 Proved developed reserves, 12/31 Production $700,000 60,000 100,000 100,000 bbl.

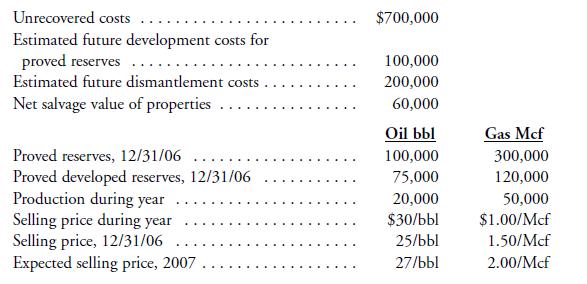

Data for Pride Oil Company for 12/31/06 are as follows:a. Compute DD&A using a common unit of measure based on BOE.b. Compute DD&A using the unit-of-revenue basis.c. Which would be the appropriate basis? Unrecovered costs $700,000 Estimated future development costs for proved reserves ....

Wildcat Oil Company began operations January 1, 2005. Transactions for the first three years include the data below. Using that data:a. Prepare journal entries assuming FC (ignore revenue entries and assume no exclusions from the amortization base).b. Prepare income statements under FC and SE for

Aggie Oil Company began operations in 2006. Give the entries, assuming the following transactions in the first three years of operations. Calculate DD&A twice, once assuming no exclusions and once assuming all possible exclusions from the amortization base.Ignore the ceiling test for 2006, but

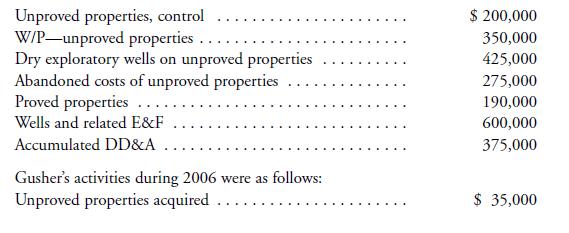

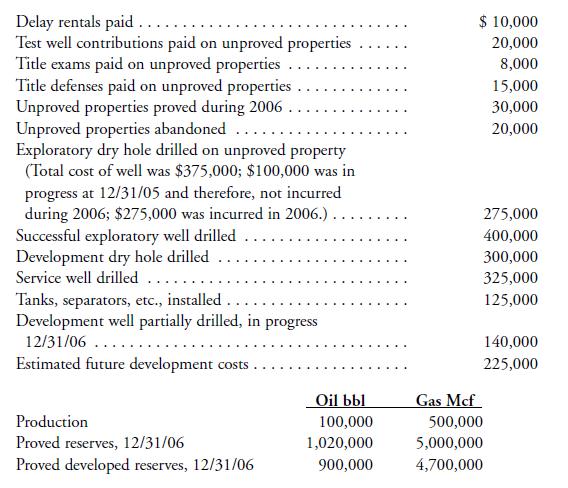

Data as of 12/31/05 for Gusher Oil Company’s U.S. properties are as follows:a. Use T accounts to accumulate costs.b. Calculate DD&A for 2006, assuming no cost exclusions and using a common unit of measure based on BOE.c. Calculate DD&A for 2006, assuming all possible cost exclusions and

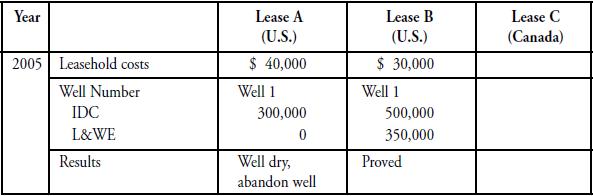

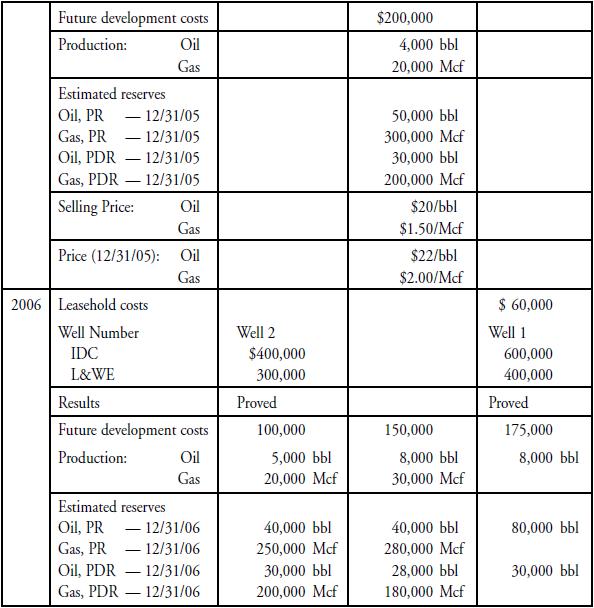

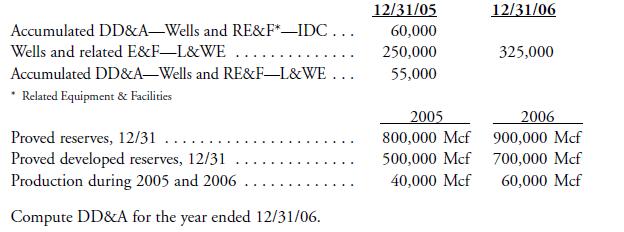

The Jones Oil Company started its oil and gas exploration and production business in 2005. During the year 2005 and 2006, the company provided the following information relating to leases located both in the U.S. and in Canada:a. Record the above information for both years. Ignore revenue

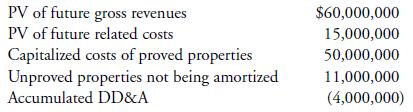

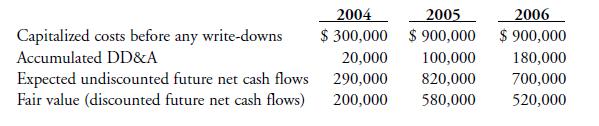

The Ebert Oil Company provides the following information for the year ended December 31, 2007:REQUIRED:a. Prepare a ceiling test and an entry, if necessary, for the write-off of capitalized costs.Ignore income taxes.b. Assuming the PV of future gross revenues is \($70,000,000,\) repeat item a’s

Cruser Oil, a full-cost company, incurs the following costs during 2006:During 2007, the following costs were incurred:Delay rentals were paid on Leases A & B of \($2,000\) and \($3,000\) respectively.In the latter half of 2007, drilling operations were commenced on both leases, and costs were

The Hard Luck Oil Company incurs unproved property (Lease A) costs of \($60,000\) on April 1, 2005. An 8% loan is obtained on April 1, 2005, for \($500,000\) to finance a drilling program. Hard Luck started a well on Lease A on June 1, 2005, and the well is still in progress at 12/31/05. Drilling

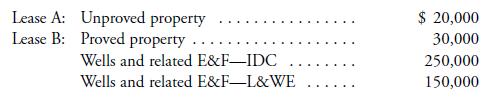

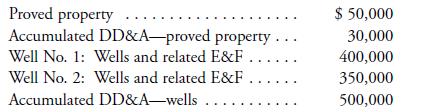

Hays Oil Company has the following account balances at 12/31/05:The above properties are abandoned in 2006. Record the abandonment entry. Lease A: Unproved property Lease B: Proved property Wells and related E&F-IDC Wells and related E&F-L&WE $ 20,000 30,000 250,000 150,000

Wildcat Oil Company has the following account balances at 12/31/05:At 12/31/05, Lease A is considered to be 40% impaired. Wildcat Company’s estimated abandonment rate of insignificant unproved properties is 60% (i.e., the impairment rate is 60%).Prepare entries to record impairment. Unproved

Use the same facts as Problem 19 and prepare entries using the following independent assumptions:a. Lease A is abandoned in 2006.b. Lease A is proved in 2006.c. Insignificant Lease Y, with a cost of \($3,000\) is abandoned.d. Insignificant Lease X, with a cost of \($5,000\) is proved.

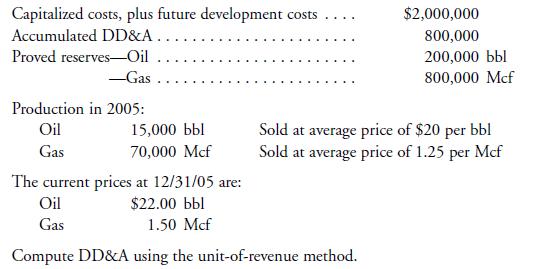

Roberts Oil Company has the following information at 12/31/05: Capitalized costs, plus future development costs Accumulated DD&A.. Proved reserves-Oil $2,000,000 800,000 200,000 bbl 800,000 Mcf -Gas Production in 2005: Oil 15,000 bbl Gas 70,000 Mcf Sold at average price of $20 per bbl Sold at

Basic Company started operations on 1/1/05. At 12/31/05, the company owned the following leases in Canada:The production was sold at \($24/bbl\) and \($1.50/Mcf.\) Current prices at 12/31/05 are \($25/bbl\) and \($2.00/Mcf.\)Compute DD&A for Canada as follows assuming:a. No exclusions from the

Data for Lucky is as follows for all U.S. properties:a. Apply the FC ceiling test and record any entries necessary, assuming that all possible costs are excluded from amortization.b. Apply the FC ceiling test and record any entries necessary, assuming that all possible costs are being amortized.

Big John Oil Company, located in Southern California, has been operating for three years. Big John uses full-cost accounting and excludes all possible costs from the amortization base. The following account balances are as of the end of 2010:REQUIRED: Give any entries necessary for the following

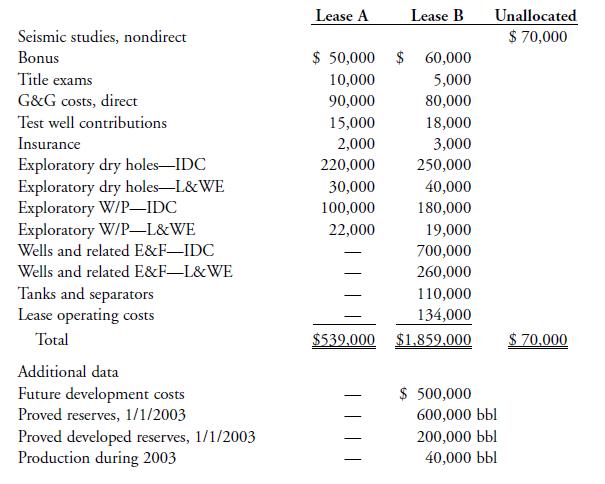

Gusher Oil Company began operations on 1/5/2001 and has acquired only two properties.The two properties, which are both considered significant, are located in different states. Lease B was proved on 1/1/2003. Costs incurred from 1/5/2001 through 12/31/2003 are as follows:Other information:The

Bonnel Company uses the full-cost method. Recently, the company acquired a truck costing \($60,000\) with an estimated life of five years (ignore salvage value). The foreman drives the truck to oversee operations on seven leases all in the same general geographical area but on multiple reservoirs.

Define the following:future dismantlementrestoration and abandonment costscommon unit of measure based on energy

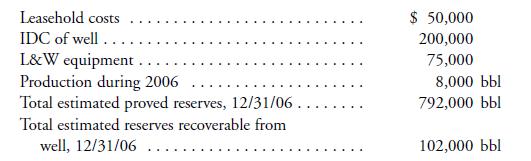

Duster Oil Company drilled its first successful well on Lease A in 2006. Data for the Lease A as of 12/31/06 are as follows:REQUIRED: Compute amortization for 2006. Leasehold costs IDC of well L&W equipment.. Production during 2006 Total estimated proved reserves, 12/31/06. Total estimated reserves

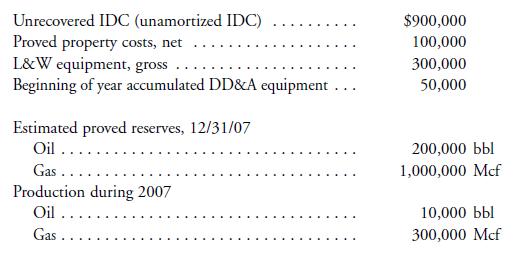

Both oil and gas are produced from BlowOut Oil Company’s lease in Texas. Additional information, 1/1/07:Assuming the lease is fully developed, compute amortization:a. assuming oil is the dominant mineralb. using a common unit of measure based on BOE Unrecovered IDC (unamortized IDC) Proved

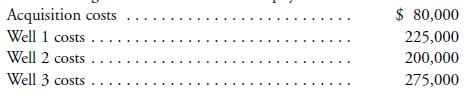

The following are costs incurred on Murphy lease:Treat each of the following independently:a. A fourth well, an exploratory well, was drilled at a cost of \($175,000\) and was determined to be dry. Give the entry to record the dry hole.b. Give the entry to record abandonment of Well 2. Equipment

During 2005, Young Oil completed the last well from their drilling and production platform off the coast of Texas. Unrecovered costs on December 31, 2005, were \($25\) million, including \($5\) million in acquisition costs and \($20\) million in drilling and development costs. Total proved

Describe the two methods currently used by oil and gas companies to account for future dismantlement, restoration and abandonment costs. Discuss the financial statement consequences of the use of each method.

Droopy Oil Company just completed (December 28, 2007) the successful testing of a tertiary recovery pilot project and as a result has determined that 900,000 barrels of oil should be classified as proved developed reserves. However, 200,000 of the 900,000 barrels will be produced only after

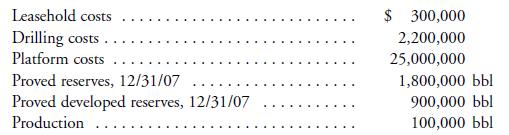

During 2007, Wildcat Oil Company constructed an offshore production platform at a cost of \($25,000,000.\) A total of 16 wells are planned. As of 12/31/07, only 2 out of the 16 wells had been drilled. Calculate DD&A given the following information. Leasehold costs Drilling costs. Platform costs

The following information as of 12/31/06 relates to the first year of operations for Basic Oil Company. From the data, (1) prepare entries and (2) prepare an income statement for Basic Oil Company for 2006, assuming revenue to the company from oil sales is \($200,000.\) Expense lifting costs as

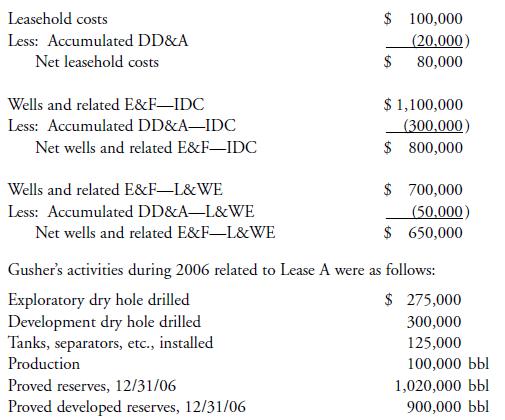

Balance sheet data for Gusher Oil Company as of 12/31/05 is as follows for Lease A:Calculate DD&A for 2006 assuming Lease A constitutes a separate amortization base. Leasehold costs Less: Accumulated DD&A Net leasehold costs Wells and related E&F-IDC Less: Accumulated DD&A-IDC Net wells and

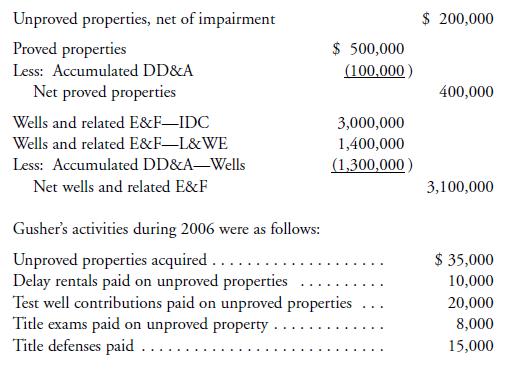

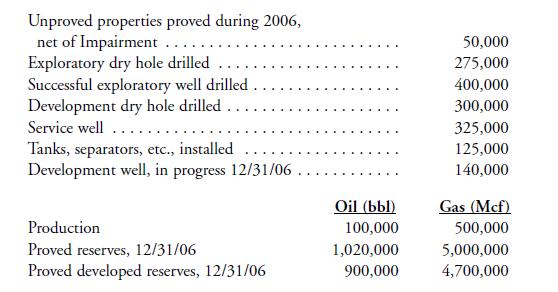

Gusher Oil Company computes DD&A on a field-wide basis. Balance sheet data as of 12/31/05 for Gusher’s Macon field are as follows:REQUIRED: Using BOE,a. Calculate DD&A for 2006.b. Calculate DD&A for 2006, assuming that part of the field, a proved property with gross acquisition costs

King Oil Company has the working interest in a fully developed lease located in Texas.As of 12/31/07, the lease had proved developed reserves of 1,200,000 barrels and unrecovered costs of \($12,000,000.\) During the third quarter of 2008, a new reserve study was received that estimated proved

Roberts Oil Company had the following account balances for the years shown relating to a proved property: Proved property cost Accumulated DD&A-proved property Wells and Related E&F-IDC.... 12/31/05 $ 30,000 6,000 350,000 12/31/06 $ 30,000 450,000

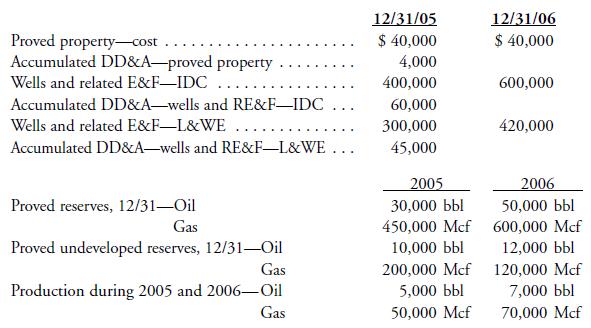

Dixie Oil Company had the following information and account balances for the years shown relating to Lease No. 1.REQUIRED: Compute DD&A for the year ended 12/31/06 using:a. a common unit of measure based on equivalent Mcfb. gas as the dominant mineralc. same relative proportion Proved

Sharon Montez purchases a 1/8 ORI for \($10,000.\) Proved reserves at year-end 2006 are 20,000 barrels and production for 2006 was 3,000 barrels. Prepare journal entries for Sharon and compute DD&A for 2006.

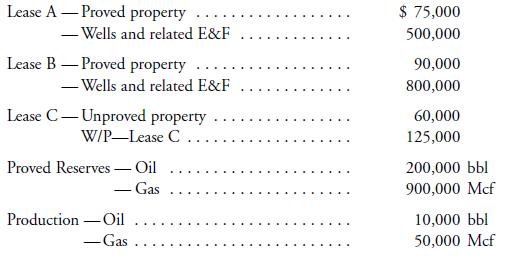

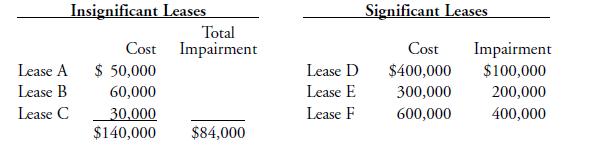

Duncan Oil Company has capitalized costs on Lease R, Lease S, and Lease T as of 12/31/2003 as follows:Duncan has no other capitalized costs. The leases are located in different counties in Texas.REQUIRED: If necessary, test the assets for impairment and make any necessary journal entries assuming

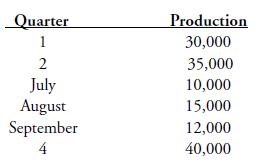

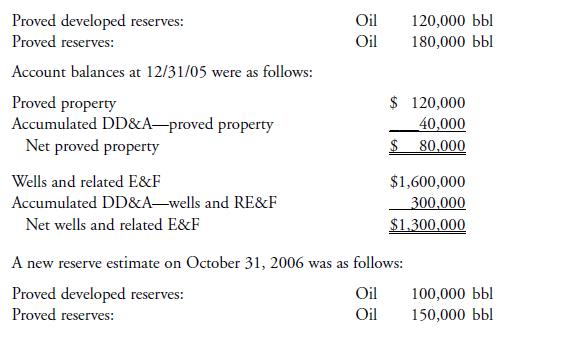

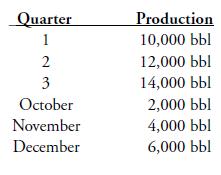

Sure Thing Company has a working interest in Lease A. As of 12/31/05, the lease had reserves as follows:Calculate DD&A for each quarter of 2006, assuming the following production, using both methods described in the book. Proved developed reserves: Proved reserves: Account balances at 12/31/05

The Bryant Company had the following costs at 12/31/05 relating to Lease A:In January, 2006, Well No. 1 quit producing and was abandoned. In March, 2006, Well No. 2 quit producing, and the well and the lease were abandoned.REQUIRED: Prepare journal entries for the abandonments. Proved property

On January 1, 2008, Mary Mabel purchased a 40,000 barrel PPI from Bad Luck Company for \($700,000.\) The PPI will be paid out of 1/5 of the WI’s share of production from Lease number 1003. The lease is burdened with a 1/7 RI. Gross production from Lease number 1003 during 2008 was 28,000 barrels.

Hopeful Company entered the oil and gas business in 2004 with the acquisition of one field. Hopeful proved the field during 2004. At the end of 2004 prices were high and costs low. During 2005, Hopeful continued exploration and development activities in the field, but towards the end of 2005, oil

Bonnel Company uses the successful-efforts method. Recently, the company acquired a truck costing \($60,000\) with an estimated life of five years (ignore salvage value). The foreman drives the truck to oversee operations on seven leases all in the same general geographical area. The foreman keeps

Define the following terms:dry holewells and related E&F—lease and well equipmentwells and related E&F—IDCday-rate contractfootage-rate contractturnkey contractAFE

Royalty Oil Company drilled an exploratory well on a lease located in a remote area. The well found reserves, but not enough to justify building a necessary pipeline. The company does not plan to drill any additional exploratory wells at this time. How should the costs of the well be handled?

Universal Oil Company drilled an exploratory well that found reserves, however, the reserves could not be classified as proved at that time. No major capital expenditure was required. How should the costs of the well be handled?

Near the end of 2007, King Oil Company drilled an exploratory well that found oil, but not in commercially producible quantities unless the price of oil went up from $25 per barrel to $30 per barrel. King decided to defer classification of the well for up to one year because its financial advisors

a. Aggie Oil Company drills an exploratory well during 2006 that finds oil, but not in commercially producible quantities at current oil prices. Since proved reserves are not found, Aggie expenses the cost of the well in 2006. Early in the next year, but after Aggie’s financial statements have

Tiger Oil Company had an exploratory well in progress at the end of 2008. Total costs incurred by 12/31/08 were \($300,000.\) During January of 2009, drilling was continued and costs of \($200,000\) were incurred. Total depth was reached and the well was determined to be dry by the end of January.

Hard Luck Oil Company incurred the following costs during 2008:a. began drilling an exploratory-type stratigraphic test well, incurred \($50,000\) of IDCb. began drilling an exploratory-type stratigraphic test well, incurred \($80,000\) of IDC and \($10,000\) in equipment costsc. began drilling a

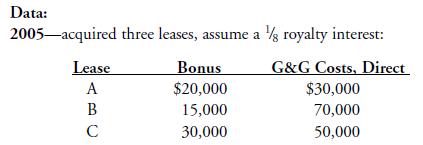

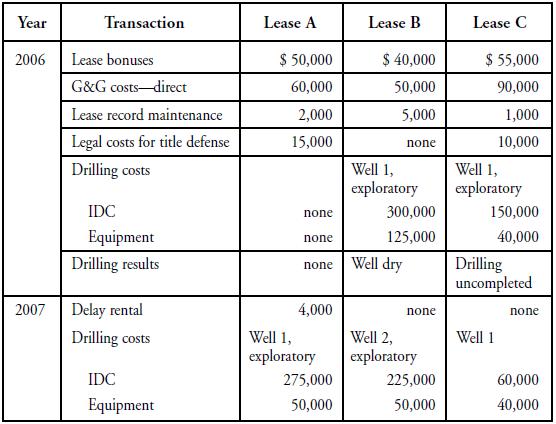

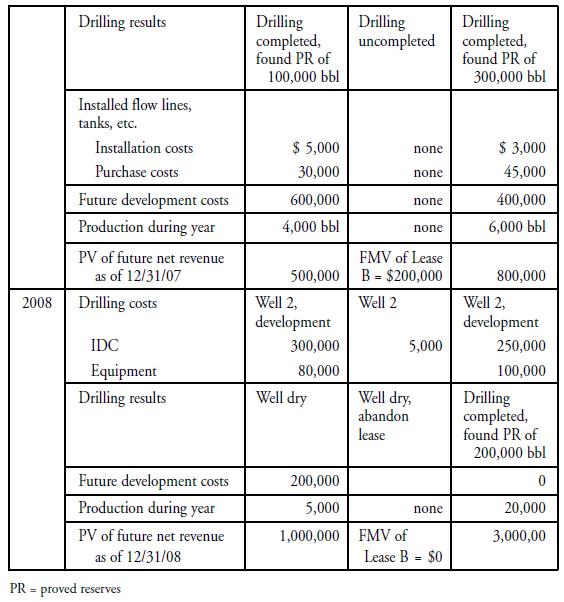

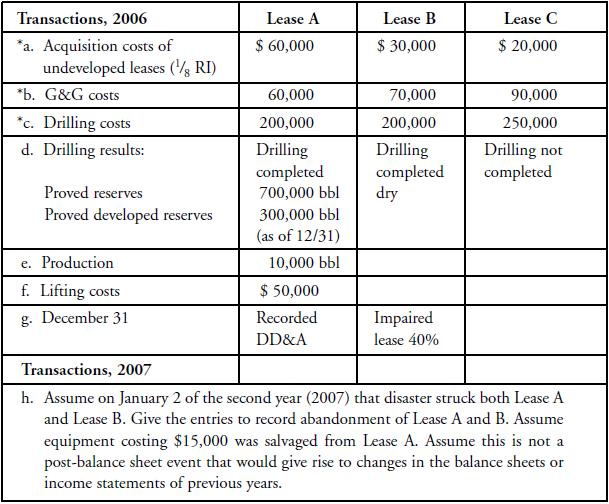

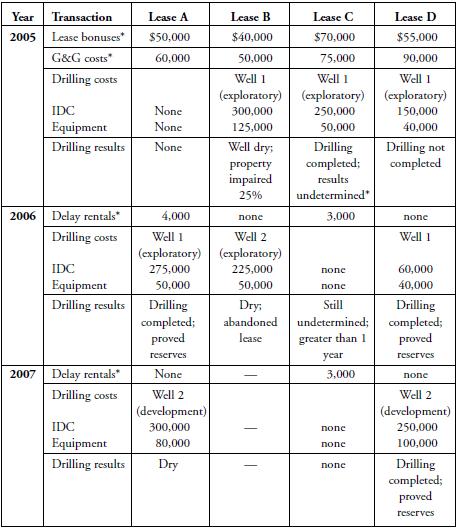

Formation Oil Company began in 2005 with the acquisition of four individually significant unproved leases. Give the entries, assuming the following transactions.You may combine entries for items marked with an asterisk (*) Year Transaction Lease A Lease B Lease C Lease D 2005 Lease bonuses* $50,000

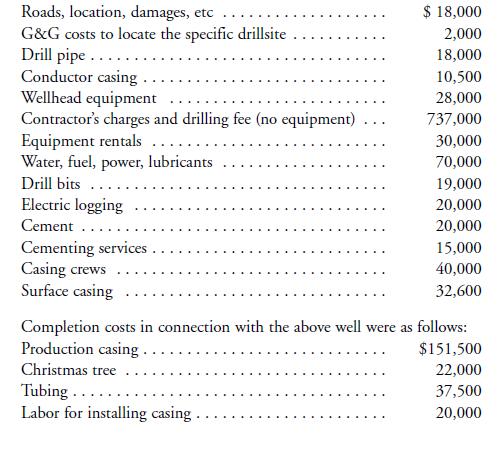

Record the following transactions:a. Brock Oil Company incurred costs of \($30,000\) in preparing a drillsite.b. The contractor was paid \($400,000\) on a day-rate contract (all intangible).c. Equipment (casing) costs of \($75,000\) were incurred.d. Costs of \($70,000\) were incurred in evaluating

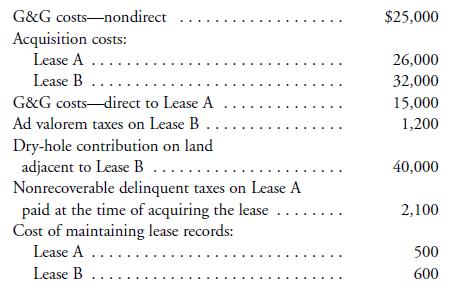

Hard Luck Oil Company incurred the following costs during the years 2006 and 2007.2006a. Contracted and paid \($50,000\) for G&G surveys during the year.b. Leased acreage in four areas as follows:1) Miller lease—500 acres @ \($50\) per acre bonus; other acquisition costs, \($2,000\)2) Ebert

During the calendar year, 2005, Garza Company had the following transactions on an unproved property:a. Drilled Hays #1 with IDC costs of \($310,000\) and equipment cost of \($42,000.\)b. The well was determined to be dry and was plugged and abandoned at a cost of \($10,000.\) Salvaged equipment

During 2005, Willis Oil Company incurred the following costs in connection with the Grove lease.a. Acquired the 800 acres Grove lease at a lease bonus of \($70\) per acre and other acquisition costs of \($10,000.\)b. Incurred the following costs in connection with Grove #1:Record the above

The Allen Oil Company incurred the following costs and had the other transactions shown below for the years 2005 and 2006. The company uses the successful efforts method of accounting.2005a. Paid \($100,000\) for G&G costs during the year.b. Leased acreage in three individually significant

Support equipment used to drill a development well cost \($13,000\) and has a 10-year life with a salvage value of \($1,000.\) The equipment was used for three months in drilling Hope #1. Record depreciation. Ignore the wells-in-progress account and use the appropriate final account.

An exploratory well that was later determined to be dry had the following costs that are appropriately assigned to the well: Depreciation on support equipment Operating costs of the support equipment (including fuel, maintenance, labor, etc.) Record the above amounts. $ 3,000 10,000

Cruser Company paid a seismic crew \($2,000\) to complete a G&G survey to select a drill-site where Hope #1 would be spudded-in. Record the above transaction.

Knight Company had the following transactions in 2005. Record the transactions.a. Acquired an undeveloped lease, \($40,000\)b. Paid a drilling contractor as follows:c. Paid costs in evaluating the well, \($20,000\)d. Completion costs for fracturing and perforating, \($25,000\) Footage rate for

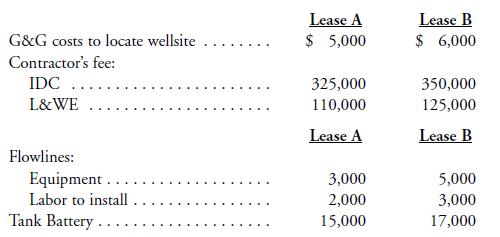

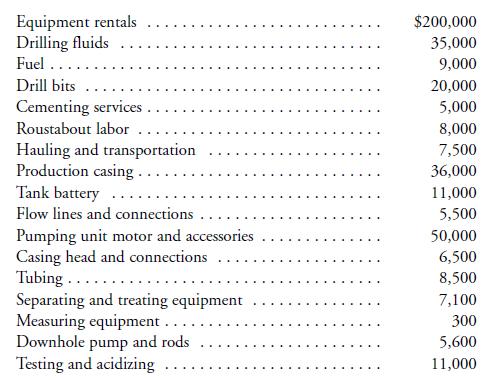

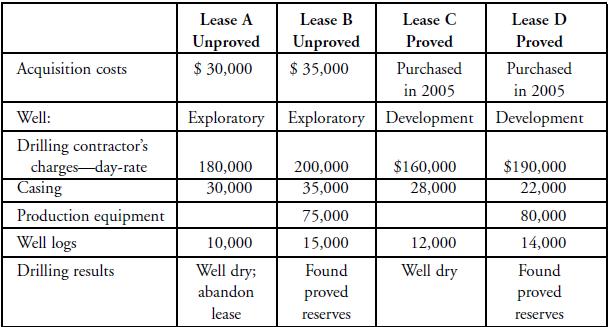

Aggie Oil Company incurred and paid the following costs during 2006:Record the above transactions. Lease A Unproved Lease B Unproved Lease C Proved Lease D Proved Acquisition costs $ 30,000 $ 35,000 Purchased Purchased in 2005 in 2005 Well: Exploratory Exploratory Development Development Drilling

The Willis Company has unproved property costs of \($40,000\) at January 1, 2006. During the year 2006, Willis incurred \($400,000\) drilling costs on Lease A. An 8%, \($500,000\) note is outstanding during the entire year and was obtained to finance the drilling program.Compute the interest

Showing 200 - 300

of 845

1

2

3

4

5

6

7

8

9

Step by Step Answers