New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting reporting

Intermediate Accounting 16th Edition Donald E. Kieso - Solutions

Hilo Company has land that cost $350,000 but now has a fair value of $500,000. Hilo Company decides to use the revaluation method specified in IFRS to account for the land.Which of the following statements is correct?(a) Hilo Company must continue to report the land at$350,000.(b) Hilo Company

Which of the following statements is correct?(a) Both IFRS and GAAP permit revaluation of property, plant, and equipment.(b) IFRS permits revaluation of property, plant, and equipment but not GAAP.(c) Both IFRS and GAAP do not permit revaluation of property, plant, and equipment.(d) GAAP permits

Francisco Corporation is constructing a new building at a total initial cost of $10,000,000. The building is expected to have a useful life of 50 years with no residual value. The building’s finished surfaces (e.g., roof cover and floor cover) are 5% of this cost and have a useful life of 20

Mandall Company constructed a warehouse for $280,000 on January 2, 2017. Mandall estimates that the warehouse has a useful life of 20 years and no residual value. Construction records indicate that $40,000 of the cost of the warehouse relates to its heating, ventilation, and air conditioning

Under IFRS, agricultural activity results in which of the following types of assets?I. Agricultural produce II. Biological assets(a) I only.(b) II only.(c) I and II.(d) Neither I nor II.

Assume that Darcy Industries had the following inventory values.Inventory cost (on December 31, 2017) $1,500 Inventory market (on December 31, 2017) $1,350 Inventory net realizable value(on December 31, 2017) $1,320 Under IFRS, what is the inventory carrying value on December 31, 2017?(a)

Starfish Company (a company using GAAP and the LIFO inventory method) is considering changing to IFRS and the FIFO inventory method. How would a comparison of these methods affect Starfish’s financials?(a) During a period of inflation, working capital would decrease when IFRS and the FIFO

All of the following are key differences between GAAP and IFRS with respect to accounting for inventories except the:(a) definition of the lower-of-cost-or-market test for inventory valuation differs between GAAP and IFRS.(b) average-cost method is prohibited under IFRS.(c) inventory basis

All of the following are key similarities between GAAP and IFRS with respect to accounting for inventories except:(a) costs to include in inventories are similar.(b) LIFO cost flow assumption where appropriate is used by both sets of standards.(c) fair value valuation of inventories is prohibited

Which of the following statements is true?(a) The fair value option requires that some types of financial instruments be recorded at fair value.(b) The fair value option requires that all noncurrent financial instruments be recorded at amortized cost.(c) The fair value option allows, but does not

Under IFRS:(a) the entry to record estimated uncollected accounts is the same as GAAP.(b) loans and receivables should only be tested for impairment as a group.(c) it is always acceptable to use the direct write-off method.(d) all financial instruments are recorded at fair value.

Which of the following statements is false?(a) Receivables include equity securities purchased by the company.(b) Receivables include credit card receivables.(c) Receivables include amounts owed by employees as result of company loans to employees.(d) Receivables include amounts resulting from

Under IFRS, receivables are to be reported on the balance sheet at:(a) amortized cost.(b) amortized cost adjusted for estimated loss provisions.(c) historical cost.(d) replacement cost.

Under IFRS, cash and cash equivalents are reported:(a) the same as GAAP.(b) as separate items.(c) similar to GAAP, except for the reporting of bank overdrafts.(d) always as the first items in the current assets section.

A company has purchased a tract of land and expects to build a production plant on the land in approximately 5 years.During the 5 years before construction, the land will be idle.Under IFRS, the land should be reported as:(a) land expense.(b) property, plant, and equipment.(c) an intangible

Franco Company uses IFRS and owns property, plant, and equipment with a historical cost of $5,000,000. At December 31, 2016, the company reported a valuation reserve of $690,000.At December 31, 2017, the property, plant, and equipment was appraised at $5,325,000. The valuation reserve will show

Companies that use IFRS:(a) may report all their assets on the statement of fi nancial position at fair value.(b) are not allowed to net assets (assets − liabilities) on their statement of fi nancial positions.(c) may report non-current assets before current assets on the statement of fi nancial

Current assets under IFRS are listed generally:(a) by importance.(b) in the reverse order of their expected conversion to cash.(c) by longevity.(d) alphabetically.

Which of the following statements about IFRS and GAAP accounting and reporting requirements for the balance sheet is not correct?(a) Both IFRS and GAAP distinguish between current and non-current assets and liabilities.(b) The presentation formats required by IFRS and GAAP for the balance sheet are

Which of the following is not an acceptable way of displaying the components of other comprehensive income under IFRS?(a) Within the statement of retained earnings.(b) Second income statement.(c) Combined statement of comprehensive income.(d) All of these choices are acceptable.

The non-controlling interest section of the income statement is:(a) required under GAAP but not under IFRS.(b) required under IFRS but not under GAAP.(c) required under IFRS and GAAP.(d) not reported under GAAP or IFRS.

Which statement is correct regarding IFRS?(a) An advantage of the nature-of-expense method is that it is simple to apply because allocations of expense to different functions are not necessary.(b) The function-of-expense approach never requires arbitrary allocations.(c) An advantage of the

Which of the following statements is correct regarding income reporting under IFRS?(a) IFRS does not permit revaluation of property, plant, and equipment, and intangible assets.(b) IFRS provides the same options for reporting comprehensive income as GAAP.(c) Companies must classify expenses by

Which of the following is not reported in an income statement under IFRS?(a) Discontinued operations.(b) Extraordinary items.(c) Cost of goods sold.(d) Income tax.

The purpose of presenting comparative information in the transition to IFRS is:(a) to ensure that the information is a faithful representation.(b) to be in accordance with the Sarbanes-Oxley Act.(c) to provide users of the financial statements with information on GAAP in one period and IFRS in the

When converting to IFRS, a company must:(a) recast previously issued financial statements in accordance with IFRS.(b) use GAAP in the reporting period but subsequently use IFRS.(c) prepare at least three years of comparative statements.(d) use GAAP in the transition year but IFRS in the reporting

The transition date is the date:(a) when a company no longer reports under its national standards.(b) when the company issues its most recent financial statement under IFRS.(c) three years prior to the reporting date.(d) None of the above.

Information in a company’s first IFRS statements must:(a) have a cost that does not exceed the benefits.(b) be transparent.(c) provide a suitable starting point.(d) All the above.

Which statement is correct regarding IFRS?(a) IFRS reverses the rules of debits and credits, that is, debits are on the right and credits are on the left.(b) IFRS uses the same process for recording transactions as GAAP.(c) The chart of accounts under IFRS is different because revenues follow

With respect to the IASB conceptual framework project:(a) work is being conducted to produce separate discussion papers.(b) work is being conducted with the FASB.(c) work is being conducted to result in a discussion paper covering all the identified areas.(d) the framework will not address elements

The issues that the FASB and IASB must address in developing a conceptual framework include all of the following except:(a) should the characteristic of relevance be traded-off in favor of information that is verifiable?(b) should a single measurement method such as historical cost be used?(c) what

Companies that use IFRS:(a) must report all their assets on the statement of financial position (balance sheet) at fair value.(b) may report property, plant, and equipment and natural resources at fair value.(c) may refer to a concept statement on estimating fair values when market data are not

Which of the following statements is false?(a) The monetary unit assumption is used under IFRS.(b) Under IFRS, companies may use fair value for property, plant, and equipment.(c) The FASB and IASB are no longer working on a joint conceptual framework project.(d) Under IFRS, there are the same

Which of the following statements about the IASB and FASB conceptual frameworks is not correct?(a) The IASB conceptual framework does not identify the element comprehensive income.(b) The existing IASB and FASB conceptual frameworks are organized in similar ways.(c) The FASB and IASB agree that the

Which of the following statements is true?(a) The IASB has the same number of members as the FASB.(b) The IASB structure has both advisory and interpretation functions, but no trustees.(c) The IASB has been in existence longer than the FASB.(d) The IASB structure is quite similar to the FASB’s,

The authoritative status of The Conceptual Framework for Financial Reporting is as follows:(a) It is used when there is no standard or interpretation related to the reporting issues under consideration.(b) It is not as authoritative as a standard but takes precedence over any interpretation related

IFRS is comprised of:(a) International Financial Reporting Standards and FASB Financial Reporting Standards.(b) International Financial Reporting Standards, International Accounting Standards, and International Accounting Interpretations.(c) International Accounting Standards and International

The major key players on the international side are the:(a) IASB and FASB. (c) SEC and FASB.(b) IOSCO and the SEC. (d) IASB and IOSCO.

IFRS stands for:(a) International Federation of Reporting Services.(b) Independent Financial Reporting Standards.(c) International Financial Reporting Standards.(d) Integrated Financial Reporting Services.

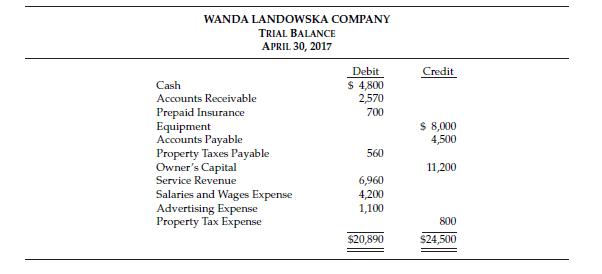

E3-2 (L02) (Corrected Trial Balance) The following trial balance of Wanda Landowska Company does not balance. Your review of the ledger reveals the following. (a) Each account had a normal balance. (b) The debit footings in Prepaid Insurance, Accounts Payable, and Property Tax Expense were each

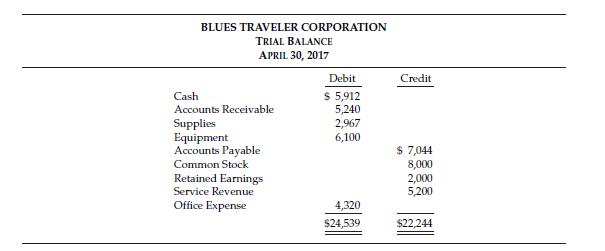

E3-3 (L02) (Corrected Trial Balance) The following trial balance of Blues Traveler Corporation does not balance.An examination of the ledger shows these errors.1. Cash received from a customer on account was recorded (both debit and credit) as $1,380 instead of $1,830.2. The purchase on account of

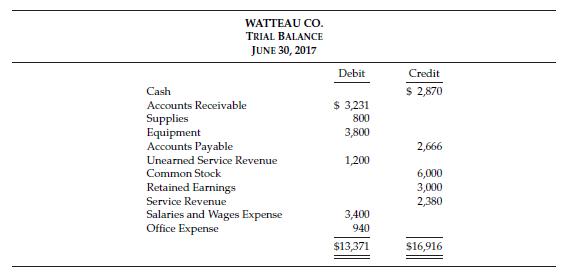

E3-4 (L02) (Corrected Trial Balance) The following trial balance of Watteau Co. does not balance.Each of the listed accounts should have a normal balance per the general ledger. An examination of the ledger and journal reveals the following errors.1. Cash received from a customer on account was

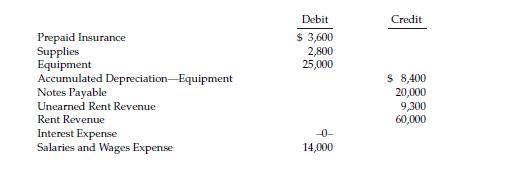

E3-5 (L03) EXCEL (Adjusting Entries) The ledger of Duggan Rental Agency on March 31 of the current year includes the following selected accounts before adjusting entries have been prepared.An analysis of the accounts shows the following.1. The equipment depreciates $250 per month.2. One-third of

E3-7 (L03) (Analyze Adjusted Data) A partial adjusted trial balance of Piper Company at January 31, 2017, shows the following.Instructions Answer the following questions, assuming the year begins January 1.(a) If the amount in Supplies Expense is the January 31 adjusting entry, and $850 of supplies

E3-9 (L02,3) (Adjusting Entries) Selected accounts of Urdu Company are shown below.Instructions From an analysis of the T-accounts, reconstruct (a) the October transaction entries, and (b) the adjusting journal entries that were made on October 31, 2017. Prepare explanations for each journal entry.

E3-10 (L03) (Adjusting Entries) Greco Resort opened for business on June 1 with eight air-conditioned units. Its trial balance on August 31 is as follows.Other data:1. The balance in prepaid insurance is a one-year premium paid on June 1, 2017.2. An inventory count on August 31 shows $450 of

E3-11 (L04) (Prepare Financial Statements) The adjusted trial balance of Anderson Cooper Co. as of December 31, 2017, contains the following.Instructions (a) Prepare an income statement.(b) Prepare a statement of retained earnings.(c) Prepare a classified balance sheet. ANDERSON COOPER CO. ADJUSTED

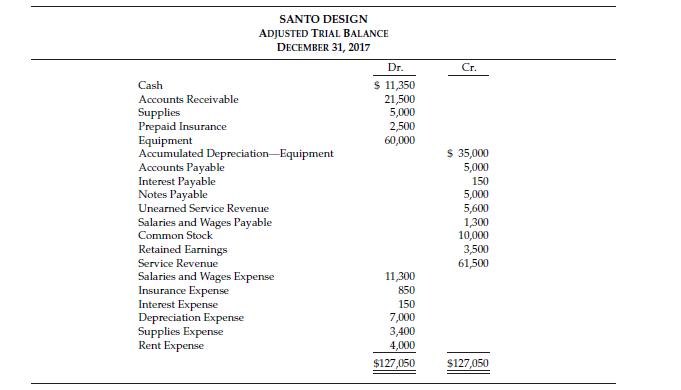

E3-12 (L03,4) (Prepare Financial Statements) Santo Design was founded by Thomas Grant in January 2011. Presented below is the adjusted trial balance as of December 31, 2017.Instructions (a) Prepare an income statement and a statement of retained earnings for the year ending December 31, 2017, and

E3-14 (L05) (Closing Entries) Presented below is information related to Gonzales Corporation for the month of January 2017.Instructions Prepare the necessary closing entries. Cost of goods sold $208,000 Delivery expense 7,000 Insurance expense 12,000 Rent expense 20,000 Salaries and wages expense

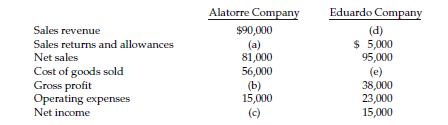

E3-15 (L06) (Missing Amounts) Presented below is financial information for two different companies.Instructions Compute the missing amounts. Alatorre Company Eduardo Company Sales revenue $90,000 Sales returns and allowances (a) Net sales 81,000 (d) $ 5,000 95,000 Cost of goods sold Gross profit

E3-16 (L05) (Closing Entries for a Corporation) Presented below are selected account balances for Homer Winslow Co. as of December 31, 2017.Instructions Prepare closing entries for Homer Winslow Co. on December 31, 2017. (Omit explanations.) Inventory 12/31/17 $ 60,000 Cost of Goods Sold $225,700

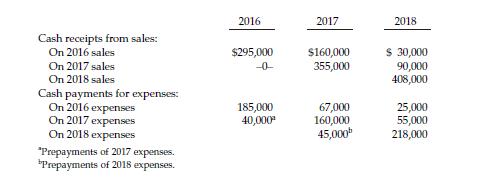

*E3-19 (L07) (Cash and Accrual Basis) Wayne Rogers Corp. maintains its financial records on the cash basis of accounting.Interested in securing a long-term loan from its regular bank, Wayne Rogers Corp. requests you as its independent CPA to convert its cash-basis income statement data to the

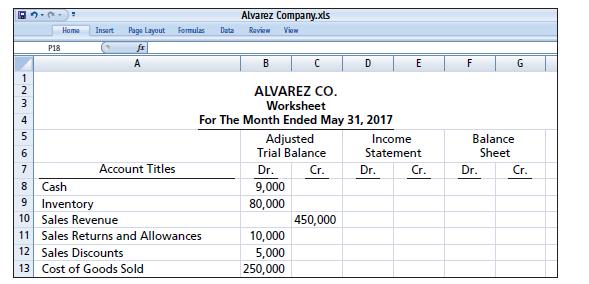

*E3-21 (L09) (Worksheet) Presented below are selected accounts for Alvarez Company as reported in the worksheet at the end of May 2017.Instructions Complete the worksheet by extending amounts reported in the adjusted trial balance to the appropriate columns in the worksheet.Do not total individual

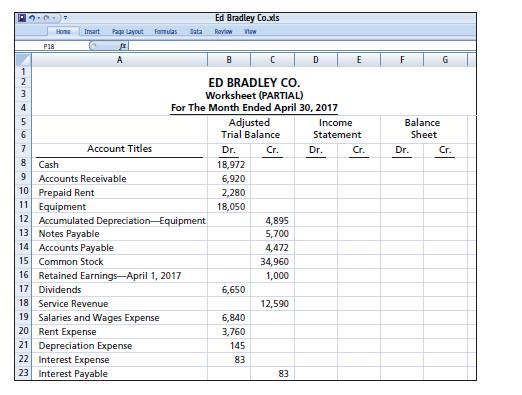

E3-22 (L09) (Worksheet and Balance Sheet Presentation) The adjusted trial balance for Ed Bradley Co. is presented in the following worksheet for the month ended April 30, 2017.Instructions Complete the worksheet and prepare a classified balance sheet. Ed Bradley Co.xls Home Insart Page Layout

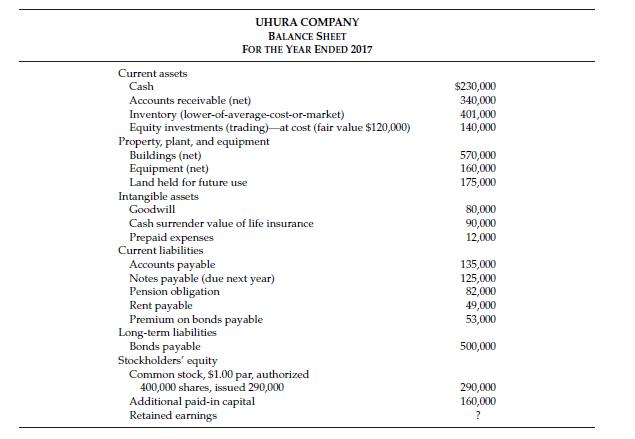

E5-5 (L03) (Preparation of a Corrected Balance Sheet) Uhura Company has decided to expand its operations. The bookkeeper recently completed the balance sheet presented below in order to obtain additional funds for expansion.Instructions Prepare a revised balance sheet given the available

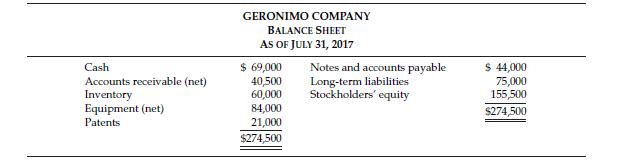

E5-6 (L02,3) (Corrections of a Balance Sheet) The bookkeeper for Geronimo Company has prepared the following balance sheet as of July 31, 2017.The following additional information is provided.1. Cash includes $1,200 in a petty cash fund and $15,000 in a bond sinking fund.2. The net accounts

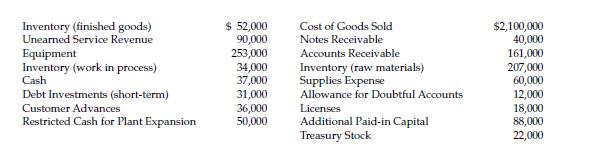

E5-7 (L03) EXCEL (Current Assets Section of the Balance Sheet) Presented below are selected accounts of Yasunari Kawabata Company at December 31, 2017.The following additional information is available.1. Inventories are valued at lower-of-cost-or-market using LIFO.2. Equipment is recorded at cost.

E5-9 (L02,3) (Current Assets and Current Liabilities) The current assets and current liabilities sections of the balance sheet of Allessandro Scarlatti Company appear as follows.The following errors in the corporation’s accounting have been discovered:1. January 2018 cash disbursements entered as

E5-11 (L03) EXCEL (Balance Sheet Preparation) Presented below is the adjusted trial balance of Kelly Corporation at December 31, 2017.Additional information:1. Net loss for the year was $2,500.2. No dividends were declared during 2017.Instructions Prepare a classified balance sheet as of December

E5-12 (L03) (Preparation of a Balance Sheet) Presented below is the trial balance of Scott Butler Corporation at December 31, 2017.Instructions Prepare a balance sheet at December 31, 2017, for Scott Butler Corporation. (Ignore income taxes.) Debit Credit Cash Sales Revenue Debt Investments

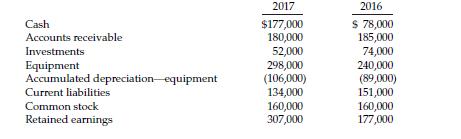

E5-14 (L05) (Preparation of a Statement of Cash Flows) The comparative balance sheets of Constantine Cavamanlis Inc. at the beginning and the end of the year 2017 are as follows.Net income of $44,000 was reported, and dividends of $23,000 were paid in 2017. New equipment was purchased and none was

E5-15 (L05,6) (Preparation of a Statement of Cash Flows) Presented below is a condensed version of the comparative balance sheets for Zubin Mehta Corporation for the last two years at December 31.Additional information:Investments were sold at a loss of $10,000; no equipment was sold; cash

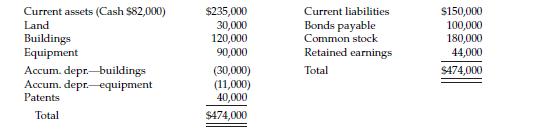

E5-16 (L05,6) (Preparation of a Statement of Cash Flows) A comparative balance sheet for Shabbona Corporation is presented below.Additional information:1. Net income for 2017 was $125,000. No gains or losses were recorded in 2017.2. Cash dividends of $60,000 were declared and paid.3. Bonds payable

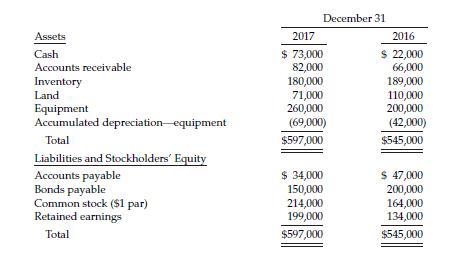

E5-17 (L03,5) (Preparation of a Statement of Cash Flows and a Balance Sheet) Grant Wood Corporation’s balance sheet at the end of 2016 included the following items.The following information is available for 2017.1. Net income was $55,000.2. Equipment (cost $20,000 and accumulated depreciation

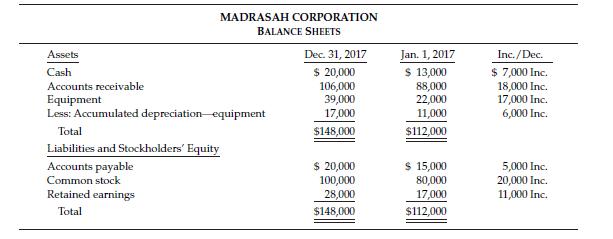

E5-18 (L05,6) (Preparation of a Statement of Cash Flows, Analysis) The comparative balance sheets of Madrasah Corporation at the beginning and end of the year 2017 appear below.Net income of $44,000 was reported, and dividends of $33,000 were paid in 2017. New equipment was purchased and none was

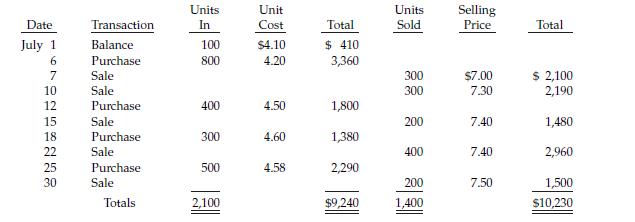

E8-13 (L03) (Compute FIFO, LIFO, Average-Cost—Periodic) Presented below is information related to Blowfish radios for the Hootie Company for the month of July.Instructions (a) Assuming that the periodic inventory method is used, compute the inventory cost at July 31 under each of the following

E8-14 (L03) (FIFO and LIFO—Periodic and Perpetual) The following is a record of Pervis Ellison Company’s transactions for Boston Teapots for the month of May 2017.Instructions (a) Assuming that perpetual inventories are not maintained and that a physical count at the end of the month shows 560

E8-15 (L03) (FIFO and LIFO; Income Statement Presentation) The board of directors of Ichiro Corporation is considering whether or not it should instruct the accounting department to shift from a first-in, first-out (FIFO) basis of pricing inventories to a last-in, first-out (LIFO) basis. The

E8-16 (L03) (FIFO and LIFO Effects) You are the vice president of finance of Sandy Alomar Corporation, a retail company that prepared two different schedules of gross margin for the first quarter ended March 31, 2017. These schedules appear below.The computation of cost of goods sold in each

E8-17 (L03) (FIFO and LIFO—Periodic) Johnny Football Shop began operations on January 2, 2017. The following stock record card for footballs was taken from the records at the end of the year.A physical inventory on December 31, 2017, reveals that 100 footballs were in stock. The bookkeeper

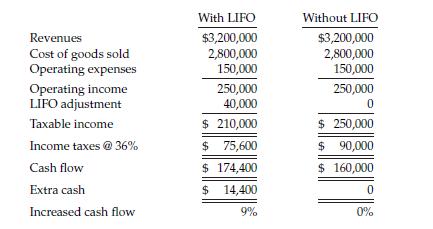

E8-18 (L04) (LIFO Effect) The following example was provided to encourage the use of the LIFO method. In a nutshell, LIFO subtracts inflation from inventory costs, deducts it from taxable income, and records it in a LIFO reserve account on the books. The LIFO benefit grows as inflation widens the

E8-19 (L03,4) (Alternative Inventory Methods—Comprehensive) Tori Amos Corporation began operations on December 1, 2016. The only inventory transaction in 2016 was the purchase of inventory on December 10, 2016, at a cost of $20 per unit.None of this inventory was sold in 2016. Relevant

E8-20 (L04) (Dollar-Value LIFO) Oasis Company has used the dollar-value LIFO method for inventory cost determination for many years. The following data were extracted from Oasis’ records.Instructions Calculate the index used for 2018 that yielded the above results. Price Date Index at Base Prices

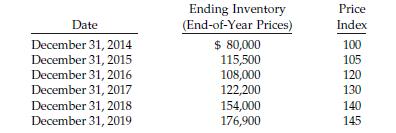

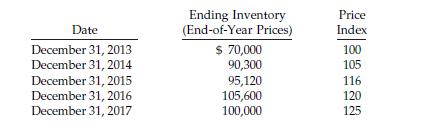

E8-22 (L04) (Dollar-Value LIFO) Presented below is information related to Dino Radja Company.Instructions Compute the ending inventory for Dino Radja Company for 2014 through 2019 using the dollar-value LIFO method.E8-23 (L04) (Dollar-Value LIFO) The following information relates to the Jimmy

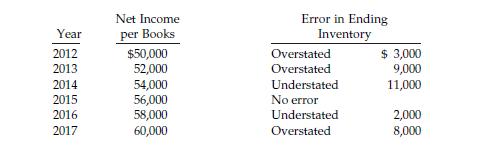

E8-26 (L05) (Inventory Errors) The net income per books of Linda Patrick Company was determined without knowledge of the errors indicated.Instructions Prepare a worksheet to show the adjusted net income figure for each of the 6 years after taking into account the inventory errors. Net Income Year

E8-25 (L05) (Inventory Errors) At December 31, 2016, Stacy McGill Corporation reported current assets of $370,000 and current liabilities of $200,000. The following items may have been recorded incorrectly.1. Goods purchased costing $22,000 were shipped f.o.b. shipping point by a supplier on

E8-24 (L05) (Inventory Errors—Periodic) Ann M. Martin Company makes the following errors during the current year.(Evaluate each case independently and assume ending inventory in the following year is correctly stated.)1. Ending inventory is overstated, but purchases and related accounts payable

E8-21 (L04) (Dollar-Value LIFO) The dollar-value LIFO method was adopted by Enya Corp. on January 1, 2017. Its inventory on that date was $160,000. On December 31, 2017, the inventory at prices existing on that date amounted to $140,000. The price level at January 1, 2017, was 100, and the price

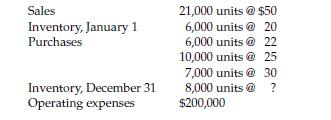

E8-12 (L03) (FIFO, LIFO, Average-Cost Inventory) Shania Twain Company was formed on December 1, 2016. The following information is available from Twain’s inventory records for Product BAP.Purchases Sales April 1 (balance on hand) 600 @ $ 6.00 April 3 500 @ $10.00 4 1,500 @ 6.08 9 1,400 @ 10.00 8

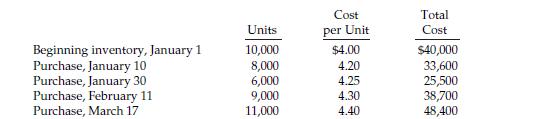

E8-11 (L03) (FIFO, LIFO and Average-Cost Determination) John Adams Company’s record of transactions for the month of April was as follows.Instructions (a) Assuming that periodic inventory records are kept in units only, compute the inventory at April 30 using (1) LIFO and (2) average-cost.(b)

E8-10 (L03) (FIFO and LIFO—Periodic and Perpetual) Inventory information for Part 311 of Monique Aaron Corp. discloses the following information for the month of June.June 1 Balance 300 units @ $10 June 10 Sold 200 units @ $24 11 Purchased 800 units @ $12 15 Sold 500 units @ $25 20 Purchased 500

E8-9 (L03) EXCEL (Periodic versus Perpetual Entries) Fong Sai-Yuk Company sells one product. Presented below is information for January for Fong Sai-Yuk Company.Jan. 1 Inventory 100 units at $5 each 4 Sale 80 units at $8 each 11 Purchase 150 units at $6 each 13 Sale 120 units at $8.75 each 20

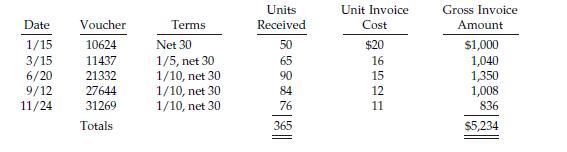

E8-8 (L02) (Purchases Recorded, Gross Method) Cruise Industries purchased $10,800 of merchandise on February 1, 2017, subject to a trade discount of 10% and with credit terms of 3/15, n/60. It returned $2,500 (gross price before trade or cash discount)on February 4. The invoice was paid on February

E8-7 (L02) (Purchases Recorded Net) Presented below are transactions related to Tom Brokaw, Inc.May 10 Purchased goods billed at $15,000 subject to cash discount terms of 2/10, n/60.11 Purchased goods billed at $13,200 subject to terms of 1/15, n/30.19 Paid invoice of May 10.24 Purchased goods

E8-6 (L02) (Determining Merchandise Amounts—Periodic) Two or more items are omitted in each of the following tabulations of income statement data. Fill in the amounts that are missing.2016 2017 2018 Sales revenue $290,000 $ ? $410,000 Sales returns and allowances 11,000 13,000 ?Net sales ?

E8-5 (L02) (Inventoriable Goods and Costs—Error Adjustments) Craig Company asks you to r eview its December 31, 2017, inventory values and prepare the necessary adjustments to the books. The following information is given to you.1. Craig uses the periodic method of recording inventory. A physical

E8-4 (L02) (Inventoriable Goods and Costs—Perpetual) Colin Davis Machine Company maintains a general ledger account for each class of inventory, debiting such accounts for increases during the period and crediting them for decreases. The transactions below relate to the Raw Materials inventory

E8-3 (L02) (Inventoriable Goods and Costs) Assume that in an annual audit of Harlowe Inc. at December 31, 2017, you find the following transactions near the closing date.1. A special machine, fabricated to order for a customer, was finished and specifically segregated in the back part of the

E8-2 (L02) EXCEL (Inventoriable Goods and Costs) In your audit of Jose Oliva Company, you find that a physical inventory on December 31, 2017, showed merchandise with a cost of $441,000 was on hand at that date. You also discover the following items were all excluded from the $441,000.1.

E8-1 (L02) (Inventoriable Goods and Costs) Presented below is a list of items that may or may not be reported as inventory in a company’s December 31 balance sheet.1. Goods out on consignment at another company’s store.2. Goods sold on an installment basis (bad debts can be reasonably

E7-27 (L09) (Expected Cash Flows) On December 31, 2017, Conchita Martinez Company signed a $1,000,000 note to Sauk City Bank. The market interest rate at that time was 12%. The stated interest rate on the note was 10%, payable annually. The note matures in 5 years. Unfortunately, because of lower

E7-26 (L09) (Expected Cash Flows) On December 31, 2017, Iva Majoli Company borrowed $62,092 from Paris Bank, signing a 5-year, $100,000 zero-interest-bearing note. The note was issued to yield 10% interest. Unfortunately, during 2019, Majoli began to experience financial difficulty. As a result, at

E7-25 (L08) (Bank Reconciliation and Adjusting Entries) Logan Bruno Company has just received the August 31, 2017, bank statement, which is summarized below.County National Bank Disbursements Receipts Balance Balance, August 1 $ 9,369 Deposits during August $32,200 41,569 Note collected for

E7-24 (L08) (Bank Reconciliation and Adjusting Entries) Angela Lansbury Company deposits all receipts and makes all payments by check. The following information is available from the cash records.June 30 Bank Reconciliation Balance per bank $ 7,000 Add: Deposits in transit 1,540 Deduct: Outstanding

E7-23 (L08) (Petty Cash) The petty cash fund of Fonzarelli’s Auto Repair Service, a sole proprietorship, contains the following.1. Coins and currency $ 15.20 2. Postage stamps 2.90 3. An I.O.U. from Richie Cunningham, an employee, for cash advance 40.00 4. Check payable to Fonzarelli’s Auto

E7-22 (L08) (Petty Cash) Carolyn Keene, Inc. decided to establish a petty cash fund to help ensure internal control over its small cash expenditures. The following information is available for the month of April.1. On April 1, it established a petty cash fund in the amount of $200.2. A summary of

E7-21 (L06,7) (Transfer of Receivables) Use the information for Jones Company as presented in E7-20. Jones is planning to factor some accounts receivable at the end of the year. Accounts totaling $25,000 will be transferred to Credit Factors, Inc. with recourse. Credit Factors will retain 5% of the

E7-20 (L07) (Analysis of Receivables) Presented below is information for Jones Company.1. Beginning-of-the-year Accounts Receivable balance was $15,000.2. Net sales (all on account) for the year were $100,000. Jones does not offer cash discounts.3. Collections on accounts receivable during the year

E7-19 (L06) (Transfer of Receivables without Recourse) JFK Corp. factors $300,000 of accounts receivable with LBJ Finance Corporation on a without recourse basis on July 1, 2017. The receivables records are transferred to LBJ Finance, which will receive the collections. LBJ Finance assesses a

E7-18 (L06) (Transfer of Receivables with Recourse) Beyoncé Corporation factors $175,000 of accounts receivable with Kathleen Battle Financing, Inc. on a with recourse basis. Kathleen Battle Financing will collect the receivables. The receivables records are transferred to Kathleen Battle

Showing 1100 - 1200

of 3974

First

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Last

Step by Step Answers