New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting 11th

Intermediate Accounting IFRS International Adaptation 5th Edition Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield - Solutions

CA3.5 (LO 2, 3) (Identification of Income Statement Weaknesses) The following financial statement was prepared by employees of Walters plc.Walters plc Income Statement Year Ended December 31, 2025 Revenues Gross sales, including sales taxes £1,044,300 Less: Returns, allowances, and cash discounts

CA3.4 (LO 1) (Income Reporting Items) Simpson Group is an entertainment firm that derives approximately 30% of its income from the Casino Knights Division, which manages gambling facilities.As auditor for Simpson, you have recently overheard the following discussion between the controller and

CA3.3 (LO 1) Ethics (Earnings Management) Charlie Brown, controller for Kelly Corporation, is preparing the company’s income statement at year-end. He notes that the company lost a considerable sum on the sale of some equipment it had decided to replace. Brown does not want to highlight it as a

CA3.2 (LO 1) Groupwork (Earnings Management) Bobek Industries has recently reported steadily increasing income. The company reported income of €20,000 in 2022, €25,000 in 2023, and€30,000 in 2024. A number of market analysts have recommended that investors buy Bobek shares because the

CA3.1 (LO 1, 2, 3) (Identification of Income Statement Deficiencies) O’Malley plc requires a bank loan for additional working capital to finance expansion. The bank has requested an audited income statement for the year 2025. The accountant for O’Malley plc provides you with the following

*P3.8 (LO 2, 3, 6) Groupwork (Income Statement) Wade NV has 150,000 ordinary shares outstanding.In 2025, the company reports income before income tax of €1,210,000. Additional transactions not considered in the €1,210,000 are as follows.1. In 2025, Wade NV sold equipment for €40,000. The

*P3.7 (LO 4, 6) (Retained Earnings Statement, Prior Period Adjustment) The following is the retained earnings account for the year 2025 for Acadian Corp.Retained earnings, January 1, 2025 $257,600 Add:Gain on sale of investments $41,200 Net income 84,500 Refund on litigation with government 21,600

*P3.6 (LO 2, 3, 4, 6) (Statement Presentation) Presented below is a combined income and retained earnings statement for Sapporo Ltd. for 2025 (amounts in thousands).Net sales ¥640,000 Costs and expenses Cost of goods sold ¥500,000 Selling, general, and administrative expenses 66,000 Other, net

*P3.4 (LO 2, 3, 6) Groupwork (Income Statement Items) Maher AG reported income before income tax during 2025 of €790,000. Additional transactions occurring in 2025 but not considered in the€790,000 are as follows.1. The company experienced an uninsured flood loss in the amount of €90,000

P3.3 (LO 2, 3, 4) (Income Statement, Retained Earnings, Periodic Inventory) Presented below is the trial balance of Thompson Ltd. at December 31, 2025.Thompson Ltd.Trial Balance December 31, 2025 Debit Credit Purchase Discounts £ 10,000 Cash £ 189,700 Accounts Receivable 105,000 Rent Revenue

P3.2 (LO 2, 4) (Income Statement, Retained Earnings) Presented below is information related to Dickinson AG for 2025.Retained earnings balance, January 1, 2025 € 980,000 Sales revenue 25,000,000 Cost of goods sold 16,000,000 Interest expense 70,000 Selling and administrative expenses 4,700,000

P3.1 (LO 2, 3, 4) (Income Components) Presented below are financial statement classifications for the statement of comprehensive income and the retained earnings statement. For each transaction or account title, enter in the space provided a letter (or letters) to indicate the usual

*E3.22 (LO 6) (Change in Accounting Principle) Tim Mattke Company began operations in 2023 and, for simplicity reasons, adopted weighted-average pricing for inventory. In 2025, in accordance with other companies in its industry, Mattke changed its inventory pricing to FIFO. The pretax income data

E3.21 (LO 5) (Allocate Transaction Price) Shaw Company sells goods that cost $300,000 to Ricard Company for $410,000 on January 2, 2025. The sales price includes an installation fee, which has a standalone selling price of $40,000. The standalone selling price of the goods is $370,000. The

E3.20 (LO 5) (Determine Transaction Price) Jeff Heun, president of Concrete Always, agrees to construct a concrete cart path at Dakota Golf Club. Concrete Always enters into a contract with Dakota to construct the path for $200,000. In addition, as part of the contract, a performance bonus of

E3.19 (LO 5) (Fundamentals of Revenue Recognition) Consider the following.1. One of the main indicators of whether control has passed to the customer is whether revenue has been earned. Is this statement correct?2. One of the criteria that contracts must meet to apply the revenue standard is that

E3.18 (LO 4) (Changes in Equity) The equity section of Hasbro Inc. at January 1, 2025, was as follows.Share capital—ordinary $300,000 Accumulated other comprehensive income Unrealized holding gain on non-trading equity securities 50,000 Retained earnings 20,000 During the year, the company had

E3.17 (LO 3, 4) (Various Reporting Formats) The following information was taken from the records of Vega SA for the year 2025: income tax applicable to income from continuing operations R$119,000, income tax savings applicable to loss on discontinued operations R$25,500, and unrealized holding gain

E3.16 (LO 3, 4) (Comprehensive Income) Bryant plc reports the following information for 2025:sales revenue £750,000, cost of goods sold £500,000, operating expenses £80,000, and an unrealized holding loss on non-trading equity securities for 2025 of £50,000. It declared and paid a cash dividend

E3.15 (LO 3, 4) (Comprehensive Income) Gaertner AG reported the following for 2025: net sales€1,200,000, cost of goods sold €720,000, selling and administrative expenses €320,000, and an unrealized holding gain on non-trading equity securities.Instructions Prepare a statement of comprehensive

*E3.14 (LO 3, 6) (Change in Accounting Principle) Zehms Company began operations in 2023 and adopted weighted-average pricing for inventory. In 2025, in accordance with other companies in its industry, Zehms changed its inventory pricing to FIFO. The pretax income data is reported below.Year

E3.13 (LO 3) (Earnings per Share) At December 31, 2024, Schroeder SE had the following shares outstanding.8% cumulative preference shares, €100 par, 107,500 shares €10,750,000 Ordinary shares, €5 par, 4,000,000 shares 20,000,000 During 2025, Schroeder did not issue any additional shares. The

*E3.12 (LO 4, 6) (Retained Earnings Statement) McEntire Corporation began operations on January 1, 2022. During its first 3 years of operations, McEntire reported net income and declared dividends as follows.Net income Dividends declared 2022 $ 40,000 $ –0–2023 125,000 50,000 2024 160,000

E3.11 (LO 2, 3) (Condensed Income Statement—Periodic Inventory Method) Presented below are selected ledger accounts of Woods Corporation at December 31, 2025.Cash $ 185,000 Salaries and wages expense (sales) $284,000 Inventory (beginning) 535,000 Salaries and wages expense (office) 346,000 Sales

E3.9 (LO 2, 3, 4) (Income Statement with Retained Earnings) Presented below is information related to Tao Ltd. for the year 2025 (amounts in thousands).Net sales HK$1,200,000 Write-off of inventory due to obsolescence HK$ 80,000 Cost of goods sold 780,000 Depreciation expense omitted by accident in

*E3.8 (LO 2, 3, 6) (Income Statement, EPS) Presented below are selected ledger accounts of McGraw SA as of December 31, 2025.Cash € 50,000 Administrative expenses 100,000 Selling expenses 80,000 Net sales 540,000 Cost of goods sold 260,000 Cash dividends declared (2025) 20,000 Cash dividends paid

E3.7 (LO 2, 3, 4) (Income Statement) The accountant for Weatherspoon Shoe has compiled the following information from the company’s records as a basis for an income statement for the year ended December 31, 2025.Rent revenue £ 29,000 Interest expense 18,000 Unrealized gain on non-trading equity

E3.6 (LO 2, 3) (Income Statement Items) The following balances were taken from the books of Parnevik ASA on December 31, 2025.Interest revenue € 86,000 Accumulated depreciation—buildings € 28,000 Cash 51,000 Notes receivable 155,000 Sales revenue 1,280,000 Selling expenses 194,000 Accounts

E3.5 (LO 2, 3) (Income Statement) Presented below is information related to Webster plc(amounts in thousands).Administrative expenses Officers’ salaries £ 4,900 Depreciation of office furniture and equipment 3,960 Cost of goods sold 63,570 Rent revenue 17,230 Selling expenses Delivery expense

E3.4 (LO 2) (Income Statement Presentation) The financial records of Dunbar Inc. were destroyed by fire at the end of 2025. Fortunately, the controller had kept the following statistical data related to the income statement.1. The beginning merchandise inventory was $92,000, and it decreased 20%

E3.3 (LO 2) (Income Statement Items) Presented below are certain account balances of Wade Products Co.Rent revenue $ 6,500 Sales discounts $ 7,800 Interest expense 12,700 Selling expenses 99,400 Beginning retained earnings 114,400 Sales revenue 400,000 Ending retained earnings 134,000 Income tax

E3.2 (LO 2) (Computation of Net Income) The following are changes in all account balances of Jackson Furniture during the current year, except for retained earnings.Increase(Decrease)Increase(Decrease)Cash £ 69,000 Accounts Payable £ (51,000)Accounts Receivable (net) 45,000 Bonds Payable 82,000

E3.1 (LO 2, 4) (Compute Income Measures) Presented below is information related to Viel AG at December 31, 2025, the end of its first year of operations.Sales revenue €310,000 Cost of goods sold 140,000 Selling and administrative expenses 50,000 Gain on sale of plant assets 30,000 Unrealized gain

*BE3.21 (LO 6) Vandross Company has recorded bad debt expense in the past at a rate of 1½% of accounts receivable, based on an aging analysis. In 2025, Vandross decides to increase its estimate to 2%.If the new rate had been used in prior years, cumulative bad debt expense would have been $380,000

*BE3.20 (LO 6) During 2025, Williamson Company changed from FIFO to weighted-average inventory pricing. Pretax income in 2024 and 2023 (Williamson’s first year of operations) under FIFO was$160,000 and $180,000, respectively. Pretax income using weighted-average pricing in the prior years would

BE3.19 (LO 5) On May 1, 2025, Mount Company enters into a contract to transfer a product to Eric Company on September 30, 2025. It is agreed that Eric will pay the full price of $25,000 in advance on June 15, 2025. Eric pays on June 15, 2025, and Mount delivers the product on September 30, 2025.

BE3.18 (LO 5) Nair Corp. enters into a contract with a customer to build an apartment building for$1,000,000. The customer hopes to rent apartments at the beginning of the school year and provides a performance bonus of $150,000 to be paid if the building is ready for rental beginning August 1,

BE3.17 (LO 5) Ismail Construction enters into a contract to design and build a hospital. Ismail is responsible for the overall management of the project and identifies various goods and services to be provided, including engineering, site clearance, foundation, procurement, construction of the

BE3.16 (LO 5) Destin Company signs a contract to manufacture a new 3D printer for $80,000. The contract includes installation which costs $4,000 and a maintenance agreement over the life of the printer at a cost of $10,000. The printer cannot be operated without the installation. Destin Company as

BE3.15 (LO 5) Hillside Company enters into a contract with Sanchez Inc. to provide a software license and 3 years of customer support. The customer-support services require specialized knowledge that only Hillside Company’s employees can perform. How many performance obligations are in the

BE3.14 (LO 5) Leno Computers manufactures tablet computers for sale to retailers such as Fallon Electronics. Recently, Leno sold and delivered 200 tablet computers to Fallon for $20,000 on January 5, 2025. Fallon has agreed to pay for the 200 tablet computers within 30 days. Fallon has a good

BE3.13 (LO 4) On January 1, 2025, Otano Ltd. had cash and share capital of ¥60,000,000. At that date, the company had no other asset, liability, or equity balances. On January 2, 2025, it purchased for cash¥20,000,000 of non-trading equity securities. It received cash dividends of ¥3,000,000

*BE3.12 (LO 4, 6) Using the information from BE3.11, prepare a retained earnings statement for the year ended December 31, 2025. Assume an error was discovered: Land costing NT$80,000 (net of tax) was charged to repairs expense in 2024.

BE3.11 (LO 4) Tsui Ltd. has retained earnings of NT$675,000 at January 1, 2025. Net income during 2025 was NT$1,400,000, and cash dividends declared and paid during 2025 totaled NT$75,000. Prepare a retained earnings statement for the year ended December 31, 2025.

BE3.10 (LO 3) In 2025, Hollis Corporation reported net income of $1,000,000. It declared and paid preference dividends of $250,000. During 2025, Hollis had a weighted average of 190,000 ordinary shares outstanding. Compute Hollis’s 2025 earnings per share.

*BE3.9 (LO 3, 6) Vandross NV has recorded bad debt expense in the past at a rate of 1½% of receivables.In 2025, Vandross decides to increase its estimate to 2%. If the new rate had been used in prior years, cumulative bad debt expense would have been €380,000 instead of €285,000. In 2025, bad

*BE3.8 (LO 3, 6) During 2025, Williamson Company changed from FIFO to weighted-average inventory pricing. Pretax income in 2024 and 2023 (Williamson’s first year of operations) under FIFO was$160,000 and $180,000, respectively. Pretax income using weighted-average pricing in the prior years would

BE3.7 (LO 2, 3) Finley plc had income from continuing operations of £10,600,000 in 2025. During 2025, it disposed of its restaurant division at an after-tax loss of £189,000. Prior to disposal, the division operated at a loss of £315,000 (net of tax) in 2025. Finley had 10,000,000 shares

BE3.6 (LO 2, 3) Indicate in which section (gross profit, income from operations, or income before income tax) the following items are reported: (a) interest revenue, (b) interest expense, (c) loss on impairment of goodwill, (d) sales revenue, and (e) administrative expenses.

BE3.5 (LO 2, 3) The following information is provided about Caltex Company: income from operations$430,000, loss on inventory write-downs $12,000, selling expenses $62,000, and interest expense$20,000. The tax rate is 30%. Determine net income.

BE3.4 (LO 2, 3) The following information is provided.Sales revenue HK$100,000 Gain on sale of plant assets 30,000 Selling and administrative expenses 10,000 Cost of goods sold 55,000 Interest expense 5,000 Income tax rate 20%Determine (a) income from operations, (b) income before income tax, and

BE3.3 (LO 2, 3) The following financial information is related to Volaire Group, a service company.Revenues €800,000 Income from continuing operations 100,000 Comprehensive income 120,000 Net income 90,000 Income from operations 220,000 Selling and administrative expenses 500,000 Income before

BE3.2 (LO 2) Brisky Corporation had net sales of $2,400,000 and interest revenue of $31,000 during 2025. Expenses for 2025 were cost of goods sold $1,450,000, administrative expenses $212,000, selling expenses$280,000, and interest expense $45,000. Brisky’s tax rate is 30%. The company had

BE3.1 (LO 2) Starr Ltd. had sales revenue of £540,000 in 2025. Other items recorded during the year were:Cost of goods sold £330,000 Selling expenses 120,000 Income tax 25,000 Increase in value of employees 15,000 Administrative expenses 10,000 Prepare an income statement for Starr for 2025.

40. Describe the revenue recognition principle.

39. What is the transaction price? What additional factors related to the transaction price must be considered in determining the transaction price?

38. When must multiple performance obligations in a revenue arrangement be accounted for separately?

37. Describe the critical factor in evaluating whether a performance obligation is satisfied.

36. Explain the importance of a contract in the revenue recognition process.

35. Identify the five steps in the revenue recognition process.

34. Gribble AG reported the following amounts in 2025: Net income,€150,000; Unrealized gain related to revaluation of buildings,€10,000, net of tax; Unrealized loss related to non-trading equity securities,€(35,000), net of tax. Determine Gribble’s total comprehensive income for 2025.

33. What are two ways that other comprehensive income may be displayed(reported)?

32. IFRS usually requires the use of accrual accounting to “fairly present” income. If the cash receipts and disbursements method of accounting will “clearly reflect” taxable income, why does this method also not usually “fairly present” income?

31. What major types of items are reported in the retained earnings statement?

30. Explain how a change in accounting principle affects the current year’s net income.

29. How should corrections of errors be reported in the financial statements?

28. Linus Paper Company decided to close two small pulp mills in Conway, New Hampshire, and Corvallis, Oregon. Would these closings be reported in a separate section entitled “Discontinued operations after income from continuing operations”? Discuss.

27. When does tax allocation within a period become necessary?How should this allocation be handled?

26. What is meant by “tax allocation within a period”? What is the justification for such a practice?

25. Qualls SE reported 2024 earnings per share of €7.21. In 2025, Qualls reported earnings per share as follows.On income from continuing operations €8.00 On loss on discontinued operations .88 On net income €7.12 Is the decrease in earnings per share from €7.21 to €7.12 a negative trend?

24. How should a loss on the disposal of a discontinued business be disclosed in the income statement?

23. Neumann Company computed earnings per share as follows._ S h_a_r_e_s _o_uN_tes_tt_a i_nn_dc_oinmg_e _a _t _ye_a_r_-e_n_d_ Neumann has a simple capital structure. What possible errors might the company have made in the computation? Explain.

22. What effect does intraperiod tax allocation have on reported net income?

21. Cooper Investments reported an unusual gain from the sale of certain assets in its 2025 income statement. How does intraperiod tax allocation affect the reporting of this unusual gain?

20. Santo SA has eight expense accounts in its general ledger which could be classified as selling expenses. Should Santo report these eight expenses separately in its income statement or simply report one total amount for selling expenses? Explain.

19. Indicate the section of an income statement in which each of the following is shown.a. Loss on inventory write-down.b. Loss from strike.c. Bad debt expense.d. Loss on disposal of a discontinued business.e. Gain on sale of machinery.f. Interest expense.g. Depreciation expense.h. Interest revenue.

18. Indicate where the following items would ordinarily appear on the financial statements of Boleyn, plc for the year 2025.a. The service life of certain equipment was changed from 8 to 5 years. If a 5-year life had been used previously, additional depreciation of £425,000 would have been

17. Discuss the appropriate treatment in the financial statements of each of the following.a. Write-down of plant assets due to impairment.b. A delivery expense on goods sold.c. Additional depreciation on factory machinery because of an error in computing depreciation for the previous year.d. Rent

16. Discuss the appropriate treatment in the income statement for the following items.a. Loss on discontinued operations.b. Non-controlling interest allocation.c. Earnings per share.d. Gain on sale of equipment.

15. Explain the difference between the “nature-of-expense” and“function-of-expense” classifications.

14. Explain where the following items are reported on the income statement: (1) interest expense and (2) income tax.

13. Ahold Delhaize (NLD/BEL), in its consolidated income statement, reported a “settlement of securities class action” €803 million loss. In what section of the income statement is this amount reported?

12. What are the sections of the income statement that comprise(1) gross profit and (2) income from operations?

11. Do the elements of financial statements, income and expense, include gains and losses? Explain.

10. What is the major distinction between income and expenses under IFRS?

9. An article in the financial press noted that MicroStrategy (USA)reported higher income than its competitors by using a more aggressive policy for recognizing revenue on future upgrades to its products.Some contend that MicroStrategy’s quality of earnings is low. What does the term “quality

8. Why should caution be exercised in the use of the net income figure derived in an income statement? What are the objectives of IFRS in its application to the income statement?

7. How can earnings management affect the quality of earnings?

6. What is earnings management?

5. Explain the transaction approach to measuring income. Why is the transaction approach to income measurement preferable to other ways of measuring income?

4. Identify at least two situations in which application of different accounting methods or accounting estimates results in difficulties in comparing companies.

3. Identify at least two situations in which important changes in value are not reported in the income statement.

2. How can information based on past transactions be used to predict future cash flows?

1. What kinds of questions about future cash flows do investors and creditors attempt to answer with information in the income statement?

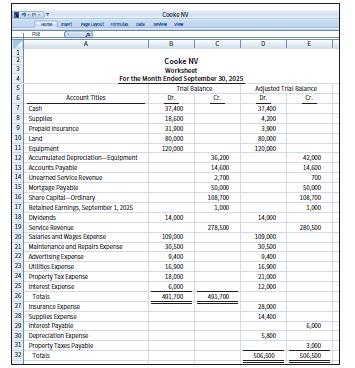

*P2.11 (LO 3, 4, 8) (Worksheet, Statement of Financial Position, Adjusting and Closing Entries) Cooke NV has a fiscal year ending on September 30. Selected data from the September 30 worksheet are presented below.Instructionsa. Prepare a complete worksheet.b. Prepare a classified statement of

*P2.10 (LO 6) (Cash and Accrual Basis) On January 1, 2025, Norma Smith and Grant Wood formed a computer sales and service company in Manchester, UK, by investing £90,000 cash. The new company, Lakeland Sales and Service, has the following transactions during January.1. Pays £6,000 in advance for

P2.9 (LO 3, 4) (Adjusting and Closing) The following is the December 31 trial balance of New York Boutique.New York Boutique Trial Balance December 31 Debit Credit Cash € 18,500 Accounts Receivable 32,000 Allowance for Doubtful Accounts € 700 Inventory, December 31 80,000 Prepaid Insurance

P2.8 (LO 3, 4) (Adjusting and Closing) Presented below is the trial balance of the Ko Golf Club, as of December 31. The books are closed annually on December 31.Ko Golf Club Trial Balance December 31 Debit Credit Cash £ 15,000 Accounts Receivable 13,000 Allowance for Doubtful Accounts £ 1,100

P2.7 (LO 3, 4) (Adjusting Entries and Financial Statements) Sorenstam Advertising AG was founded in January 2021. The following are the adjusted and unadjusted trial balances as of December 31, 2025.Sorenstam Advertising AG Trial Balance December 31, 2025 Unadjusted Adjusted Dr. Cr. Dr. Cr.Cash €

P2.6 (LO 3, 4) (Adjusting Entries and Financial Statements) The following are the trial balance and other information related to Yorkis Perez, a consulting engineer.Yorkis Perez, Consulting Engineer Trial Balance December 31, 2025 Debit Credit Cash R$ 29,500 Accounts Receivable 49,600 Allowance for

Showing 1700 - 1800

of 3960

First

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Last

Step by Step Answers