New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting

Accounting 9th edition Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett - Solutions

Broken Hill Ltd’s equity at 30 June 2016 was as follows:200000 ordinary shares, issued at $3.20, fully paid500000 ordinary shares, issued at $3.40, called to $2.40180000 redeemable preference shares, issued at $1, fully paidCalls in advance (10 000 ordinary shares)Share issue costsGeneral

Equity of Toronto Ltd at 14 February 2016 consisted of:Share capital:800000 shares (fully paid for $1)600000 shares (paid to 50c, issued at $1)$800000 300000$1100000General reservePlant replacement reserveRetained earnings10000050000125000The following events occurred during

The following information relating to the year ending 30 June 2016 for Penrith Ltd has been obtained from the company’s records.Profit for year before further adjustments and taxRetained earnings (1 July 2015)General reserveRevaluation surplusInterim dividend paidDevelopment

The following is the equity of Bowral Ltd at 30 June 2016: Share capital (200000 fully paid ordinary shares) $400000 General reserve

Picton Ltd was registered on 1 July 2016. On 4 August a prospectus was issued inviting publicsubscriptions for an issue of 200 000 12% preference shares payable $2 in full on application, and600 000 ordinary shares at a price of $1.60 per share, payable $1 on application, 20c on allotmentand the

On 1 January 2016, Shoalhaven Ltd was registered and, on the same day, the company purchased the net assets (excluding cash) of a partnership for a consideration of 240 000 ordinary shares (fully paid) at a price of $2.40 per share. 1 000 000 ordinary shares were offered to the public at$2.40 per

Newcastle Ltd was incorporated on 1 July 2016. On 1 August, it was decided to issue 300 000ordinary shares on the following terms:ApplicationAllotmentCall as required$2 per share$1 per share$1 per shareTo the end of August, applications for 350 000 shares had been received together with the

On 1 July 2016, Grafton Ltd was incorporated, and on 4 July a prospectus was issued inviting applications for 80 000 shares payable $4.50 on application, $2.50 on allotment and $2.50 on each of two calls to be made at intervals of 3 months after the date of allotment.By 31 July, applications were

A. Show the journal entries to record the following transactions for Murrurundi Ltd.1. Profit for the year was $1 750 000. Ignore income tax.2. Directors resolved to transfer the amounts specified below from retained earnings to:(a) contingencies reserve,

During the year ended 30 June 2016, the directors of Jindabyne Ltd declared and paid an interim dividend of $18 000 out of retained earnings. At the end of the year the financial statements showed a profit (before tax) of $460 000 out of which the directors made the following reserve transfers and

The following information relates to Nevertire Ltd. Profit before income tax for the year ended 30 June 2016 was $220 000. The following items were used in determining that profit:SalesCost of salesSelling, administrative and finance expensesLoss from floodInterest revenueBad debtsDevelopment costs

Penshurst Ltd’s balance sheet, before a share dividend, is as follows:Peru ltdBalance Sheetas at 30 June 2016ASSETSCash at bankNon-current assets$ 20000150000EQUITYShare capitalGeneral reserveRetained earnings$10000040000 30000$170000$170000The company immediately declared a

During the year ended 30 June 2016, the directors of Cooma Ltd paid a final dividend out of retained earnings of $60 000, which had been recommended at the end of the previous financial year. They also declared and paid an interim dividend of $150 000 on 1 February 2017. The balance of the Retained

Bega Ltd was registered as a new company on 2 January 2017. On that day a prospectus was issued inviting applications for 300 000 ordinary shares at $10, payable $2.50 on application, $2.50 on allotment and the balance due in one call on 15 June 2017. The issue was underwritten for a fee of $7000.

Maitland Ltd has issued 2 000 000 ordinary shares for $4 and 200 000 8% preference shares for $4, all shares being fully paid. On 30 September 2016 at the annual general meeting of the company, a dividend was declared for a total cash payout of $320 000. Preference shares are entitled to

The following is an actual case:Fortescue raises $504mIron ore hopeful Fortescue Metals Group has raised $504 million to fund expansions to its emerging project in the Pilbara region of Western Australia. Fortescue said it had set a minimum raising target of US$300 million (A$344 million) for the

The following events occurred in the newly formed company, Armidale Ltd, which was registered on 31 January 2016:2016Feb. 1Mar. 1Sept. 20Oct. 20Nov. 1Dec. 15Armidale Ltd issued a prospectus calling for applications for 600000 ordinary shares to be

Scone Ltd was registered on 1 February 2016. The following events occurred in that year:Feb. 1Mar. 15Mar. 1825000 ordinary shares were allotted to the original members. The shares were paid for in full at a price of $1 each.A prospectus was issued for 100000 10% preference shares

On 1 July 2016, Denman Ltd issued a prospectus offering 160 000 of its ordinary shares, payable $1on application, $1 on allotment and $2 to be called as and when required. When applications closed on 23 July, applications had been received for 240 000 shares, including one applicant for 20 000

On 30 April, Tamworth Ltd issued 40 000 shares for $6 each, payable $2 on application, $2 on allotment and the remainder due by two equal calls on 30 June and 31 August. Share issue costs of $3500 were paid on 31 May.RequiredPrepare journal entries (in general journal format) to record the share

Warren Ltd was organised on 2 January 2016, and proceeded to issue 100000 9% cumulative preference shares and 200000 ordinary shares. The preference shares were issued privately at a value of $2 each and the ordinary shares were issued to the public at $5 each, payable in two instalments of $2.50

The directors of Dunedoo Ltd decided to issue 100 000 ordinary shares.RequiredA. Prepare journal entries (in general journal form) to record the issue of shares as a private placement to Good Times Ltd for $15 per share payable in full.B. Prepare journal entries (in general journal form) to record

‘A company must have made sufficient profits before it can pay dividends to its shareholders.’ Discuss.

A well-established company, which wanted to raise finance for expansion, decided to issue some preference shares. The terms of the issue were that the shareholders did not have the right to vote at meetings, but were entitled to dividends of 12 cents per share each year, on a cumulative basis.

‘Preference shares can offer security of dividends and other advantages over ordinary shares, and are therefore the best equity to have in a company.’ Do you agree? Explain.

How should a company account for its start-up costs, and its share issue costs? How should a company account for the fees paid to an underwriter?

Distinguish between a private placement, a public share issue and a rights issue. Distinguish also between a renounceable rights issue and a non-renounceable rights issue.

Explain the purpose of each of the following accounts used in a public share issue: Share Capital, Application, Cash Trust, Allotment, Call, Calls in Advance.

‘It is better for a company to have a constitution rather than rely on the replaceable rules in the Act.’ Discuss.

What are the contents of an application form to register a company?

What is the difference between a small proprietary company, a large proprietary company and a public company?

Two partners in a business are discussing the possibility of incorporating their business as a proprietary company. Discuss the advantages and disadvantages that this move would potentially bring to them. Briefly discuss the impact that the Corporations Act would have on their decision.

Refer to the latest financial report of Country Road Limited on its website, www.countryroad.com.au, and answer the following questions using the consolidated income statement and balance sheet/ statement of financial position and notes to the consolidated financial statements.1. The Country Road

Craig Fraser and Michelle Mason set up a partnership to run a small retail business. Craig contributed $60 000 to begin the business and Michelle’s contribution was $50 000. Craig is confident with numbers and accounting whereas Michelle prefers to deal with people and to ignore anything

Divide into groups of three or four according to students’ major areas of interest — for example, a group of commerce students, a group of management students, a group of marketing students. Discuss the following and report back to the whole class.1. If your group formed a partnership to carry

A. Calculate the amount of profit distribution to each partner under each scenario. Which scenario is most favourable to O’Malley and to O’Reilly?B. Given the capital commitments and expertise of each partner, which scenario is the most appropriate for the partnership agreement?C. What

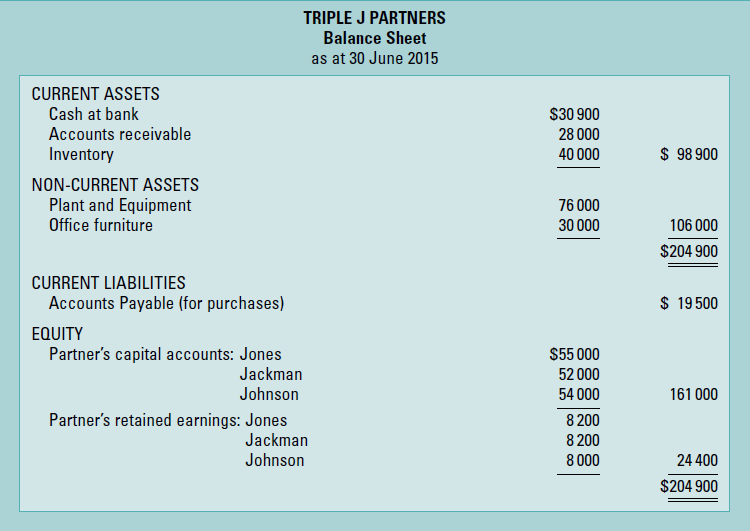

Jones, Jackman and Johnson are partners in the consulting firm of Triple J Partners. The balance sheet of the partnership as at 30 June 2015 is set out below.It was agreed that all profits be divided equally between the partners. Business transactions for the year were as follows (ignore

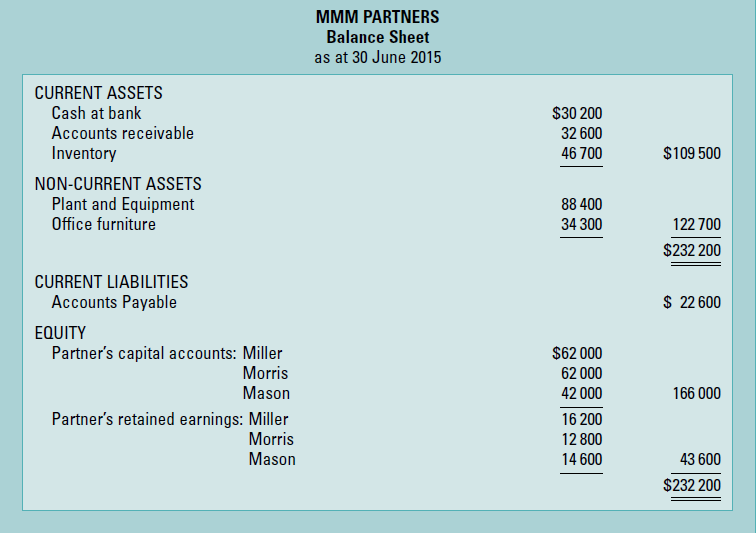

Miller, Morris and Mason are partners in the consulting firm of MMM Partners. The balance sheet of the partnership as at 30 June 2015 is set out below.It was agreed that all profits should be divided equally between the partners. Business transactions for the year ending 30 June 2016

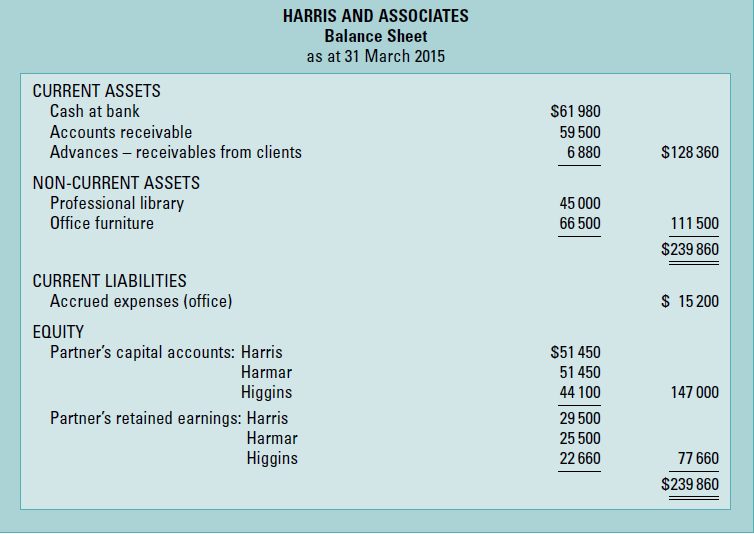

Harris, Harmar and Higgins are partners in the consulting firm of Harris and Associates. The balance sheet of the partnership as at 31 March 2015 is shown below. It was agreed that all profits would be divided equally between the partners. Business transactions for the year ending 31

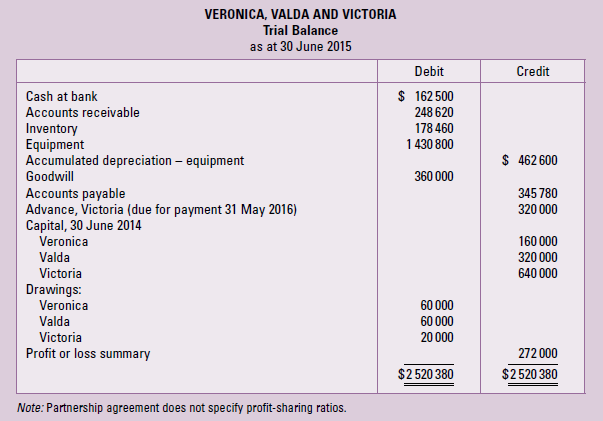

At the end of the financial year ended 30 June 2015, the trial balance of Veronica, Valda and Victoria is as shown below.Victoria made her advance before 1 July 2014. Veronica and Valda each withdrew $12 000 on 30 September 2014, $8000 on 31 December 2014, $5000 on 31 March 2015, and the remainder

Gregory and Simpson share profits in a proportion of 60:40. Gregory is entitled to a salary allow¬ance of $60 000 p.a., and Simpson is entitled to $50 000 p.a. Capitals are fixed at Gregory $72 000 and Simpson $48 000. Interest is to be calculated on partners’ capital, advances, and drawings in

On 1 July 2015, McGregor and Roberts decided to amalgamate their businesses and to share profits equally. Financial information at that date was:McGregorRobertsCapitalAccounts payableBank overdraft$101 38041 470 18 430$119 80055 300$161 280$175 100Cash at

Selected accounts from the trial balance as at 30 June 2016 of the partnership of Amber, Ruby and Gemma are as follows:DebitCreditAmber, CapitalAmber, Retained earningsRuby, CapitalRuby, Retained earningsGemma, CapitalGemma, Retained earningsLoan — ABC Bank LtdGemma, SalaryAdvance, Amber

Richards, David and Andrews decided to enter into a partnership agreement as from 1 July 2015, some of the provisions of which were as follows.1. Richards to contribute $20 000 cash, inventory the fair value of which was $42 500, plant and machinery $78 600, accounts receivable totalling $12

Francine Steele and Shaun Dunn formed a partnership on 1 July 2015. Some of Steele’s business assets and liabilities were assumed by the partnership, and these are listed below at both carrying amounts and fair value.Carrying amountFair valueCash at bankAccounts

On 1 October 2015, Dallas Lucas and Suzanne Foreman formed a partnership. Some business assets and the liabilities of Lucas were assumed by the partnership, and these are listed below at both carrying amounts and fair value.Carrying amountFair valueCash at bankMarketable securitiesAccounts

The partnership deed of Dustin, Daniel and Dylan, partners trading as Triple D Traders, includes the following provisions. 1. Salaries are to be allowed: Dustin, $35 000; Daniel, $30 000; Dylan, $25 000. 2. Dylan is to receive a bonus of 20% of the profits after allowing for partners’

A partnership is formed by Robert investing $150 000 and Linda investing $100 000. The partners are considering the following plans for dividing profits and losses:(a) According to the ratio of their original investment(b) Paying Robert a salary of $60 000 and Linda a salary of $50 000 and the

Philip and Lance have decided to form a partnership by investing $100000 and $80000 respectively. The following plans for dividing profits and losses are under consideration: (a) Sharing profits equally (b) A $20 000 salary to Philip, a $30 000 salary to Lance, and the remainder in the

Anthony Chu and Adrian Tan formed a partnership on 1 January 2015, agreeing to share profits and losses equally. Anthony contributed $80 000 in cash and plant and equipment with a fair value of $120 000. Assets contributed to and liabilities assumed by the partnership from Adrian’s business at

John Landis and Raymond Oliver formed a partnership on 1 July 2015, agreeing to share profits and losses in the ratio of 2:1. John contributed $30 000 in cash and land with a fair value of $180 000. Assets contributed to and liabilities assumed by the partnership from Raymond’s business at both

Bonnie and Clyde have a partnership to run their human resource management services firm. Account balances related to their equity for the year ended 30 June 2016 are as follows:Capital Balance 1 July 2015, BonnieCapital Balance 1 July 2015, ClydeAdditional investment, BonnieWithdrawal of capital,

Paul and Justin began their partnership on 1 July 2015 by contributing $320000 and $280000 respectively. During the first year of business, Justin contributed another $40000 and Paul with¬drew $20000 of his capital investment. The profit for the year ended 30 June 2016 of $160000 was divided

Wendy, William and Wanda are independent website developers who had been trading in active opposition to one another for some years. They decide to form a partnership, WWW Web Devel¬opers, as from 1 January 2015. The agreement set out the following basic arrangements:Wendy to contribute $8000 in

Greg, Graham and Gordon are partners. The partnership agreement provides that partners will receive interest of 8% of their average capital balance and a salary allowance as follows:GregGrahamGordon$50 00040 00040 000Greg, who manages the business, will receive a bonus of 25% of the

Martin and Brett share profits on a 60:40 basis respectively. On 1 July 2016 the equity accounts were as follows:MartinBrettCapitalRetained earnings$540 000160 000$460 000130 000The partners were entitled to 12% interest on capital. Brett ran the business and received a salary

Terry and Craig share profits in the proportion of one-third and two-thirds respectively. On 1 July 2015, the equity accounts stood as follows:TerryCraigCapitalRetained earnings$80 00025 000$120 00032 000Partners were entitled to 8% interest on capital, and Terry, as manager,

Meagan and Jenny are in partnership, sharing profits equally. Provision exists in the partner¬ship agreement for charging interest on capital at the rate of 8% p.a. and interest on drawings at 10% p.a. Capital and Drawings account balances are:Meagan, CapitalJenny, CapitalMeagan, DrawingsJenny,

Barrett and Pickering run a market stall together as a partnership. On 30 November 2016, Barrett withdrew $12 000 cash. Pickering withdrew $8000 on 20 December 2016. On 31 March 2017 Pickering withdrew $15 000 of her capital investment in cash to meet unexpected medical expenses for her

Thomson and Turner formed a partnership by investing $110 000 and $90 000 respectively. The partnership had a final profit of $72 000 in the first year.RequiredA. Prepare the journal entries to record the allocation of profit under each of the following assumptions, using method 1

Warren and Winston’s partnership had a final profit for the year of $40 500. When the partnership was formed at the beginning of the year Warren invested $150 000 and Winston invested $100 000.RequiredA. Prepare the journal entries to record the allocation of profit under each of the

Penny and Lane formed a partnership on 1 July 2015 with initial capital balances of $200 000 and $220 000 respectively. For the year ended 30 June 2016, the Profit or Loss Summary account dis¬closed a final credit balance of $180 000.RequiredA. Prepare the closing entry to transfer the profit

Godfrey and Taylor formed a partnership on 1 July 2015 with initial capital balances of $90 000 and $60 000 respectively. For the year ended 30 June 2016, the Profit or Loss Summary account disclosed a final credit balance of $96 000.RequiredA. Prepare the closing entry to transfer the profit

Refer to the data presented in exercise 15.2. Assume further that Pike and Smith agree that their opening capital balances in the new partnership should be the same and set the amount at $90 000.RequiredPrepare separate journal entries to record the initial investment of each partner, assuming

Tammie Pike and Gail Smith agree to combine their businesses and form a partnership. The fair value and the carrying amount of the assets contributed by each partner and the liabilities assumed by the partnership are shown below:Tammie PikeGail SmithCarrying amountFair valueCarrying amountFair

Thomas and James, who were operating separate competing businesses, decided on 1 July 2015 to form a partnership by contributing cash, assets and liabilities of their respective businesses. At that date the fair values of the assets and liabilities were as set out below:ThomasJamesCash at

Ethan and Amy, who have been friends for a long time, decide to go into partnership selling a range of pet accessories. They seek advice from an accountant regarding the best system, the generally accepted accounting principles to be used in the accounting records, and the format and contents of

Eduardo and Evanthia run a craft shop as a partnership. During the year Eduardo incurred an unusual amount of personal expenses in relation to his family and felt that his share of the partnership profit for the year would not cover these costs. Eduardo approached Evanthia to see if he can get any

Hannah and Jeremy set up a partnership to run a café. At the time of establishing the business, Hannah was in a better financial position than Jeremy and so contributed 60% of the capital required. Jeremy believes that he contributes as much effort to running the café as Hannah and therefore

‘Partners’ advances and capital both represent money contributed to the partnership by the partners. Therefore the accounting treatment for interest paid on advances and capital should be the same.’ Discuss.

A student of accounting was heard to remark: ‘You really do not need a Profit Distribution account when accounting for profit distribution in a partnership. Everything can be done through the Profit or Loss Summary account.’ Discuss.

‘The accounting treatment of a partner’s drawings differs when separate Retained Earnings accounts are kept for each partner as opposed to not having Retained Earnings accounts. Choice of method is immaterial.’ Discuss.

Liam sold his partnership interest to Jason even though his other partners were unaware that Liam intended to do so. Does Jason have the right to be a partner? Does Jason have the right to take over Liam’s position as manager of the business? Would Jason be entitled to share in the partnership

Which is likely to last longer and why: a partnership or a company?

‘There is really no need for a partnership agreement since all issues likely to arise among partners are adequately covered in the appropriate Partnership Act.’ Discuss.

‘The big disadvantage of a sole trader business is that the personal liability of the owner is unlimited — the owner could lose everything. I think I will take on a partner and convert my business to a partnership. That way I will certainly reduce the chances of losing my personal assets if the

Refer to the latest financial report of JB Hi-Fi Limited on its website, www.jbhifi.com.au, and answer the following questions:A perusal of the report clearly indicates that JB Hi-Fi Ltd does make capital budgeting decisions of some magnitude. What evidence is there of these activities?What method

Creekside Cement Ltd is considering purchasing a new cement-mixing truck. The supplier of trucks, Sea Meant Trucks Ltd, sells its trucks for $350000 cash or customers can purchase them by paying annual instalments of $60000 per year over 10 years at a discount rate of 10%.Di Shonest is the chief

The Hyupp Group runs five-star hotels in most major cities. The group is looking to build a six-star luxury resort in South-East Asia on a remote island. The chief financial officer prefers to use the payback method to evaluate the new investment. The senior accountant believes the return on

A. Assuming that Fonus Ltd will continue to produce 300 000 phones each year, should the plastic casings be made by Fonus or bought?B. If Fonus Ltd produces 500 000 phones each year, would your decision be different? If so, why?C. If the space

Ben’s Big BBQs Pty Ltd makes large barbecues and sells them through specialist barbecue stores and outdoor furniture stores. Ben’s Big BBQs Pty Ltd has been approached by a national department store, DMart, to produce 2000 barbecues per year for the next 3 years on their behalf.Ben’s Big BBQs

Flasher Freight Ltd is considering three investments for the new year. The company has a cost of capital of 12%. Summary information concerning the net cash inflows of the investments and their initial costs is shown below:YearInvestmentABC123456789101112Initial

Evans Engineering is an engineering consulting firm specialising in the installation of electronic communications systems. The company is considering the purchase of testing equipment that will be used on jobs. The equipment will cost $1 740 000 and will have no residual value at the end of its

Medrano Ltd is a furniture manufacturer. The company is looking at three alternative specialised machines to replace its existing production line. Data for each of the machines are as follows:MachineExpected annual profit increaseEstimated annual net cash inflows increaseEstimated lifeInitial

Wilde Marketing Partnership, marketing consultants, is considering a project requiring considerable expansion of its current operations. This will require the purchase of equipment at a cost of $600 000. The new equipment will have a 10-year life and then have no resale value. The new project would

Pierre Ltd is a catering business owned by well-known chef Pierre Boudin. It is organised as two divisions, each with its own manager. There is the Shop Division, managed by Louise Lane, that runs retail outlets in a number of shopping centres throughout the city, and the Catering Division, managed

Truong Trucking Co. Ltd operates a freight service and is planning the next year’s operation. The company’s assets are estimated to be $30 400 000 at the beginning of the financial year and $30 700 000 at the 30 June end of financial year. The company expects that it will deliver 25 000 000

Green Gnome Ltd produces garden fertilisers. The fertilisers are made into pellets which are sold in 5-kilogram packets. The fertilisers are based on a basic mix of minerals and nutrients that make up 80% of each packet. To this basic mix are added special nutrients and minerals for special purpose

Retelsdorf Ltd manufactures tablet screens. Recently, the company has been producing slightly below 75% of capacity and management is considering how to use currently unused plant capacity. One proposal is to produce a component used in several of the company’s products that is currently being

SpeedBurn Ltd manufactures DVD burners and is considering expanding production. A distributor has asked the company to produce a special order of 3000 DVD burners. The burners will be sold using a different brand name and will not influence SpeedBurn Ltd’s current sales. The plant is currently

Abeer Kalaba is the owner of a Champion Chips Pty Ltd, which produces communication chips for mobile phones. The company has two production lines, one for a standard communication chip that is also produced by several competitors and one for custom communication chips built to customer

Kellaway Ltd is considering installing a computer controlled production line to significantly reduce its manufacturing costs. The annual after-tax cost savings are expected to be $460000, and the production line will cost $1 800000. Its useful life will be 5 years and its resale value at that time

Hentschke Ltd produces two products, X and Y, at a joint cost of $480 000. The company can sell 620 000 units of product X for $30 per unit, or the units can be processed further at a cost of $160 000 to produce 16 000 units of product A, 20 000 units of product B, and 25 000 units of product C.

Butterworth Boats Ltd produces boats for water skiing. The motors for the boats are currently purchased from an outside supplier at a cost of $4000 each. Some factory space that Butterworth Boats Ltd currently rents to another company for storage purposes could be used to produce the motors. The

The screens for mobile phones are currently purchased from an outside supplier at a cost of $40 each by Futuristic Phones Ltd. The company is concerned about the quality of the screens it is buying as one in a 500 is found to be faulty within a year of using them to make mobile phones.If the

Bradshaw Bakeries Ltd is evaluating investment alternatives for three machines and has compiled the following relevant information:InvestmentMachine M1Machine M2Machine M3Initial investment$600000$860 000$560000Net cash inflows:Year 1

Fizulic Filters is considering the purchase of equipment that will produce net after-tax cash savings over the useful life of the equipment of 5 years as follows:YearAfter-tax savings12345$14 30013 80013 30012 80012 400RequiredWhat is the maximum price the business should

Home whitegoods manufacturer, Mozzi Ltd, is evaluating the purchase of a new machine that will cost $580 000 and be paid for in cash. The machine will be depreciated over 10 years with a resale value at the end of $60 000. Annual before-tax cash savings from better productivity are expected to be

Qin Ltd wants to determine its cost of capital to use in future capital budgeting decisions. The company’s capital structure is as follows:Source of capitalAmountAfter-tax costBorrowingsPreference sharesOrdinary sharesRetained earnings$60000020000010000007000009%7%10%10%RequiredCalculate the

Chocolate Daydreams Ltd produces chocolates and is evaluating the purchase of a new machine that will cost $1060000 and have no residual value. Annual net cash inflows (including tax payments) for each of the next 10 years are expected to be $190000. The average annual profit is expected to be

Showing 5800 - 5900

of 6751

First

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Last

Step by Step Answers