New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate financial management

Financial Management Principles And Applications 14th Global Edition Sheridan Titman, Arthur Keown, John Martin - Solutions

In Finance in a Flat World: International Bonds on page 312, we learned about the bonds issued in financial markets outside of the United States. What are the potential benefits and costs of investing in foreign-issue bonds?

Explain why an increase in the inflation rate will cause the yield to maturity on a bond to increase.

Is the price of a long-term (longer-maturity) bond more or less sensitive to changes in interest rates than that of a short-term bond? Why?

Why does the market value of a bond differ from its par value when the coupon interest rate does not equal the market yield to maturity on a comparable-risk bond?

Distinguish between the following:a. Debentures and mortgage bondsb. Eurobonds, zero-coupon bonds, and junk bondsc. Premium and discount bonds

What does a bond rating reflect? Why is the rating important to the firm’s management?

Which elements determine what the yield to maturity will be for a bond?

Compare and contrast current yield and yield to maturity.

Why does a bond’s par or face value differ from its market value?

In Finance for Life: Buying a House in the United Kingdom on page 295, we learned about interest-only mortgage. When would you want to use an interest-only mortgage? Think about scenarios where people may expect a lump sum towards the end of their working life.

Describe the relationship between yield to maturity and the value of a bond.

What is the difference between a bond’s clean price and its dirty price, and what does the saying “buy clean, pay dirty” mean?

What is a floating-rate bond?

Distinguish between public and private corporate debt.

In Regardless of Your Major: Borrow Now, Pay Later on page 288, the suggestion is made that you may already be involved in the debt markets. List your current involvement in the debt markets. Do you have credit cards, a car loan, or a college tuition loan? How do you expect to be involved in the

What is the typical shape of the yield curve for U.S. Treasury securities?

What is the yield curve?

What are junk bonds, and why do they typically have a higher interest rate than other types of bonds?

How does an investor receive a return from a zero- or very-low-coupon bond?

What are the differences among debentures, subordinated debentures, and mortgage bonds?

As the maturity date of a bond approaches, what happens to the price of a discount bond? Is the result the same if the bond is a premium bond?

Why does a bond sell at a premium when the coupon rate is higher than the market’s yield to maturity on a similar bond, and vice versa?

As interest rates increase, why does the price of a long-term bond decrease more than the price of a short-term bond?

Explain the relationship between bond value and the bond’s yield to maturity.

How do semiannual interest payments affect the asset valuation equation?

Why might the expected return be different from the yield to maturity?

How do you estimate the appropriate discount rate?

How do you calculate the value of a bond?

What is the difference between an Aaa and a Ba bond in terms of risks to the bondholder? What are the principal bond rating agencies?

What are the key features of a bond? Which of these features determines the cash flows paid to the bondholder?

What is a bond indenture?

Explain the effects of inflation on interest rates and describe the term structure of interest rates.

Identify the major types of corporate bonds.

Describe the four key bond valuation relationships.

Calculate the value of a bond and relate it to the yield to maturity on the bond.

Identify the key features of bonds and describe the difference between private and public debt markets.

Based on your analysis, do you think the proposed fund offers a fair return given its risk?Explain.

In addition to this information provided, Jeremy has also gathered some additional data. He has observed that the risk-free rate of interest in the market for the coming year is 3 percent, the market risk premium is 5 percent, and the beta for the new investment is

What is the expected rate of return for the fund based on the CAPM?

What is the reward-to-risk ratio for the fund based on the fund’s standard deviation as a measure of risk?

What is the expected rate of return and standard deviation for the fund given the estimates of fund performance in different states of the economy?

(Using the CAPM to find expected returns) Grace Corporation is considering the following investments. The current rate on Treasury bills is 2.5 percent, and the expected return for the market portfolio is 9 percent.Stock Beta K 1.12 G 1.3 B 0.75 U 1.02a. Using the CAPM, what rate of return should

(Using the CAPM to find expected returns) Marsha is considering four different investments to include in his portfolio. The current rate on Treasury bills is 4 percent, and the expected return for the market portfolio is 10 percent. Using the CAPM, what rate of return should Marsha require for each

(Computing the portfolio beta and plotting the security market line) You own a portfolio consisting of the following stocks:Stock Percentage of Portfolio Beta Return Expected 1 10% 1.00 12%2 25 0.75 11 3 15 1.30 15 4 30 0.60 9 5 20 1.20 14 The risk-free rate is 4 percent. Also, the expected return

(Plotting the security market line) Assume the risk-free rate of return is 4 percent and the expected rate of return on the market portfolio is 10 percent.a. Graph the security market line. Also, calculate and label the market risk premium on the graph.b. Using your graph from parta, identify the

(Calculating the portfolio beta and expected return) You are putting together a portfolio made up of four different stocks. However, you are considering two possible weightings:Portfolio Weightings Asset Beta First Portfolio Second Portfolio A 2.5 10% 40%B 1.0 10% 40%C 0.5 40% 10%D –1.5 40% 10%a.

(Analyzing the security market line) You are considering the construction of a portfolio comprised of equal investments in each of four different stocks. The beta for each stock follows:Security Beta A 2.5 B 1.0 C 0.5 D –1.5a. What is the portfolio beta for your proposed investment portfolio?b.

(Analyzing the security market line) Your friend Kim has inherited an investment portfolio from his uncle. He has just been informed by the investment manager, responsible for managing this portfolio on his behalf, that this portfolio has a beta of 1.8. Kim has turned to you to explain to him what

(Computing the portfolio beta and plotting the security market line) You own a portfolio consisting of the following stocks:Stock Percentage of Portfolio Beta Expected Return 1 20% 1.00 16%2 30% 0.85 14%3 15% 1.20 20%4 25% 0.60 12%5 10% 1.60 24%The risk-free rate is 3 percent. Also, the expected

(Using the CAPM to find expected returns) The expected rate of return for the general market portfolio in Singapore is 8 percent, and the risk premium in the market is estimated at 6 percent. Wilmar, ST Engineering, and Jardine have betas of .678, 1.23, and .665, respectively. What are the

(Using the CAPM to find expected returns) Genetech GmbH is a Munich-based research firm that has a .685 beta. If the market portfolio return is 10 percent and the risk-free rate is 5 percent, what is the approximate expected rate of return for Genetech (using the CAPM)?

(Using the CAPM to find expected returns) Breckenridge, Inc., has a beta of .85. If the expected market portfolio return is 10.5 percent and the risk-free rate is 3.5 percent, what is the appropriate expected return of Breckenridge (using the CAPM)?

(Using the CAPM to find expected returns) Sante Capital operates two mutual funds headquartered in Houston, Texas. The firm is evaluating the stock of four different firms for possible inclusion in its fund holdings. As part of their analysis, Sante’s managers have asked their junior analyst to

(Using the CAPM to find expected returns) Kumar and Harold Investments Ltd. is considering a number of investments proposals, listed in the table below. Assume that the rate on Treasury bills is currently 5 percent, and the expected return for the market portfolio is 8 percent. What should be the

(Using the CAPM to find expected returns)a. Compute the expected rate of return for the shares of Choudhary and Choudhary Consultancy Limited (C&C), which has a beta of 1.62. The risk-free rate is 8 percent, and the market portfolio (composed of Bombay Stock Exchange listed shares) has an expected

(Using the CAPM to find expected returns)a. Compute the expected rate of return for the shares of Rumi Plc, which has a beta of 1.46. The risk-free rate is 4 percent, and the market portfolio (composed of London Stock Exchange listed shares) has an expected return of 10 percent.b. Why is the rate

(Plotting the security market line) Mark and Sheila from Problem 8–1 are trying to apply their understanding of the security market line concept to the analysis of their real estate investment strategy. They estimate that their portfolio will have an expected rate of return of 8.25%.a. If the

(Using the CAPM to find expected returns)a. Given the following holding-period returns, compute the average returns and the standard deviations for Coria Plc. and for the market portfolio.Quarter Coria Plc. Market 1 5% 3%2 3 1 3 –2 0 4 4 2 5 1 4b. If Coria’s beta is 1.8 and the risk-free rate

(Using the CAPM to find expected returns) (Related to Checkpoint 8.3 on page 272)a. Given the following holding-period returns, compute the average returns and the standard deviations for the Sugita Corporation and for the market portfolio.Month Sugita Corp. Market 1 1.8% 1.5%2 –0.5 1.0 3 2.0 0.0

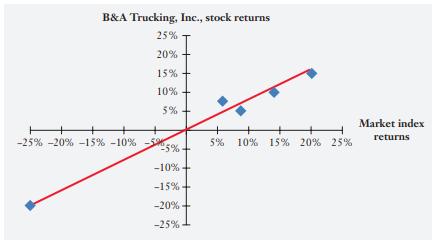

(Estimating betas) Consider the following stock returns for B&A Trucking, Inc., and the market index:Use the visual method described in Figure 8.3 to estimate the beta for B&A. Is the firm more or less risky than the market portfolio? Explain. B&A Trucking, Inc., stock returns 25% 20% 15%

(Analyzing systematic risk and expected rates of return) (Related to Checkpoint 8.3 on page 272) The following table contains beta coefficients for five firms, selected from the FTSE 100 index, from two different sources: FT.com and reuters.com. Calculate the change in the expected return from each

(Computing the expected rate of return and risk) After a tumultuous period in the stock market, Logan Morgan is considering an investment in one of two portfolios. Given the information that follows, which investment is better, based on risk (as measured by the standard deviation) and return as

(Computing the portfolio expected rate of return) Bronc Gerson is 60 years of age and is considering retirement. Bronc got his name from the fact that as a young man he spent several years in the rodeo circuit competing as a bareback rider. His retirement portfolio currently is valued at $950,000

(Computing the portfolio expected rate of return) (Related to Checkpoint 8.1 on page 257) Penny Francis inherited a $200,000 portfolio of investments from her grandparents when she turned 21 years of age. The portfolio is comprised of treasury bills and stock in Ford (F) and Harley Davidson

(Computing the standard deviation for a portfolio of two risky investments) Answer the following questions using the information provided in Problem 8–3:a. Answer part a of Problem 8–3 where Mary decides to invest 10 percent of her money in Firm A’s common stock and 90 percent in Firm B’s

(Computing the standard deviation for a portfolio of two risky investments) Mary Guilott recently graduated from Nichols State University and is anxious to begin investing her meager savings as a way of applying what she has learned in business school. Specifically, she is evaluating an investment

(Computing the standard deviation for an individual investment) (Related to Checkpoint 8.2 on page 263) Calculate the standard deviation in the anticipated returns found in Problem 8–1.

(Computing the expected rate of return) (Related to Checkpoint 8.1 on page 257) Two recent graduates from business school (Mark Van and Sheila Epps) decided to set up an investment company to acquire home mortgages that are in default but that they hope to restructure in ways that make it possible

If a company’s beta increased from 1.5 to 4.5, would its expected rate of return triple? Explain why or why not. (Hint: Assume the risk-free rate is 4 percent and the market risk premium is 5 percent.)

True or false: If the standard deviation of Company A’s stock returns is greater than the standard deviation of Company B’s stock returns, then the beta of Stock A must be greater than the beta of Stock B. Explain your answer.

Presently you own shares of stock in Company A and are considering adding some shares in either Company B or Company C. The standard deviations of all three firms are exactly the same, but the correlation between the common stock returns for Company A and Company B is .5, whereas it is –.5

Why would we expect the reward-to-risk ratio (slope of the security market line) to be the same across all risky investments? Assume that you are able to earn 5 percent per unit of risk for investing in the stock of Company A and 7 percent for investing in Company B. How would you expect investors

Describe what the Capital Asset Pricing Model tells you to your father, who has never had a course in finance. What is the key insight we gain from this model?

What is the security market line? What do the slope and intercept of this line represent?

Provide an intuitive discussion of beta and its importance in measuring risk.

Briefly discuss why there is no reason to believe that the market will reward investors with additional returns for assuming unsystematic risk.

True or false: Portfolio diversification is affected by the volatility of the returns of the individual investments in the portfolio as well as by the correlation among the returns. Explain.

While you are home for fall break, your grandfather tells you that he has purchased the stock of two firms in the automobile industry: Toyota and Ford. He goes on to discuss the merits of his decision, and one of the points he makes is that he has avoided the risk of purchasing only one company’s

Describe the relationship between the expected rate of return for an individual investment and the expected rate of return for a portfolio of several investments.

What did Depression-era humorist Will Rogers mean when he said, “People tell me about the great return I’m going to get on my investment, but I’m more concerned about the return of my investment”?

In Regardless of Your Major: Risk and Your Personal Investment Plan on page 256, what are the four guidelines suggested for analyzing your personal investment decisions?

What is the market risk premium, and how is it related to the Capital Asset Pricing Model?

Explain the concept of the security market line.

How is the portfolio beta related to the betas of the individual investments in the portfolio?

Who are Harry Markowitz and William Sharpe, and what did they do that was so important in finance?

How many different stocks are required to essentially diversify away unsystematic risk?

What are some factors that influence the returns of a company such as Home Depot that would constitute a source of systematic risk? Unsystematic risk?

When the returns of two risky investments are perfectly positively correlated, how does combining them in a portfolio affect the overall riskiness of the portfolio?

When the returns of two risky investments are perfectly negatively correlated, how does combining them in a portfolio affect the overall riskiness of the portfolio?

How is the expected rate of return on a portfolio related to the expected rates of return on the individual assets contained in the portfolio?

Estimate the investor’s expected rate of return using the Capital Asset Pricing Model.

Understand the concept of systematic risk for an individual investment and calculate portfolio systematic risk (beta).

Calculate the expected rate of return and volatility for a portfolio of investments and describe how diversification affects the returns to a portfolio of investments.

If you were given annual rate of return data for MTL’s or any other company’s stock and you were asked to estimate the average annual rate of return an investor would have earned over the sample period by holding the stock, would you use an arithmetic or a geometric average of the historical

Now calculate the compound annual rate of return using the geometric average monthly rate of return:Compound Annual Rate of Return = ¢1 +Geometric Average Monthly Rate of Return≤12- 1

Compute the annual rate of return for MTL using the beginning and ending stock prices for the period (i.e., 56.90 and 18.80).

Use the equation below:End@of@Year Stock Price = Beginning@of@Year Stock Price¢1 +Geometric Average Monthly Rate of Return≤12

Calculate the year-end price for MTL, computing the compound value of the beginning-of-year price of 56.90 per share for 12 months at the monthly geometric average rate of return calculated in Question

Calculate the average monthly rate of return for MTL using both the arithmetic and the geometric averages.

Compute MTL’s monthly realized rates of return for the entire year.

Showing 600 - 700

of 3729

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers