New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

introduces quantitative finance

Introduces Quantitative Finance 2nd edition Paul Wilmott - Solutions

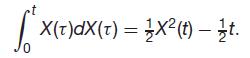

By considering X2(t), show that X(t)dX(t) = }X (t) – Įt.

Compare interest rate data with your share price data. Are there any major differences? Is the asset price modeldS = μS dt + σS dXalso suitable for modeling interest rates?

Using daily share price data, find and plot returns for the asset. What are the mean and standard deviation for the sample you have chosen?

What is the distribution of the price increase for the share movement described in Question 1?Question 1A share has an expected return of 12% per annum (with continuous compounding) and a volatility of 20% per annum. Changes in the share price satisfy dS = μS dt + σS dX. Simulate the movement of

A share has an expected return of 12% per annum (with continuous compounding) and a volatility of 20% per annum. Changes in the share price satisfy dS = μS dt + σS dX. Simulate the movement of the share price, currently $100, over a year, using a time interval of one week.

A share price is currently $75. At the end of three months, it will be either $59 or $92. What is the risk-neutral probability that the share price increases? The risk-free interest rate is 4% p.a. with continuous compounding.

A share price is currently $180. At the end of one year, it will be either $203 or $152. The risk-free interest rate is 3% p.a. with continuous compounding. Consider an American put on this underlying. Find the exercise price for which holding the option for the year is equivalent to exercising

A share price is currently $15. At the end of three months, it will be either $13 or $17. Ignoring interest rates, calculate the value of a three-month European option with payoff max(S2 − 159, 0), where S is the share price at the end of three months. You must use both the methods of setting up

A share price is currently $63. At the end of each three month period, it will change by going up $3 or going down $3. Calculate the value of a six month American put option with exercise price $61. The risk-free interest rate is 4% p.a. with continuous compounding. You must use both the methods of

A share price is currently $45. At the end of each of the next two months, it will change by going up $2 or going down $2. Calculate the value of a two month European call option with exercise price $44. The risk-free interest rate is 6% p.a. with continuous compounding. You must use both the

A share price is currently $92. At the end of one year, it will be either $86 or $98. Calculate the value of a one-year European call option with exercise price $90 using a single-step binomial tree. The risk-free interest rate is 2% p.a. with continuous compounding. You must use both the methods

A share price is currently $80. At the end of three months, it will be either $84 or $76. Ignoring interest rates, calculate the value of a three-month European call option with exercise price $79. You must use both the methods of setting up the delta-hedged portfolio, and the risk-neutral

Starting from the approximations for u and v, check that in the limit δt →0 we recover the Black–Scholes equation.

Solve the three equations for u, v and p using the alternative condition p = 1/2 instead of the condition that the tree returns to where it started, i.e. uv = 1.

Using the notation V(E) to mean the value of a European call option with strike E, what can you say about ∂V/∂E and ∂2V/∂E2 for options having the same expiration? Consider call and butterfly spreads and the absence of arbitrage.

A three-month, 80 strike, European call option is worth $11.91. The 90 call is $4.52 and the 100 call is $1.03. How much is the butterfly spread?

A share currently trades at $60. A European call with exercise price $58 and expiry in three months trades at $3. The three month default-free discount rate is 5%. A put is offered on the market, with exercise price $58 and expiry in three months, for $1.50. Do any arbitrage opportunities now

What is the difference between a payoff diagram and a profit diagram? Illustrate with a portfolio of short one share, long two calls with exercise price E.

Find the value of the following portfolios of options at expiry, as a function of the share price:(a) Long one share, long one put with exercise price E,(b) Long one call and one put, both with exercise price E,(c) Long one call, exercise price E1, short one call, exercise price E2, where E1 <

A particular forward contract costs nothing to enter into at time t and obliges the holder to buy the asset for an amount F at expiry T. The asset pays a dividend DS at time td, where 0 ≤ D ≤ 1 and t ≤ td ≤ T. Use an arbitrage argument to find the forward price F(t).Consider the point of

A spot exchange rate is currently 2.350. The one-month forward is 2.362. What is the one-month interest rate assuming there is no arbitrage?

You put $1000 in the bank at a continuously compounded rate of 5% for one year. At the end of this first year rates rise to 6%. You keep your money in the bank for another eighteen months. How much money do you now have in the bank including the accumulated, continuously compounded, interest?

The dollar sterling exchange rate (colloquially known as ‘cable’) is 1.83, £1 = $1.83. The sterling euro exchange rate is 1.41, £1 = € 1.41. The dollar euro exchange rate is 0.77, $1 = €0.77. Is there an arbitrage, and if so, how does it work?

A company whose stock price is currently S pays out a dividend DS, where 0 ≤ D ≤ 1. What is the price of the stock just after the dividend date?

A company makes a three-for-one stock split. What effect does this have on the share price?

Showing 600 - 700

of 625

1

2

3

4

5

6

7

Step by Step Answers