New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management cost accounting

Management and Cost Accounting 10th edition Colin Drury - Solutions

Corcoran Ltd operate several manufacturing processes. In process G, joint products (P1 and P2) are created in the ratio 5:3 by volume from the raw materials input. In this process, a normal loss of 5 per cent of the raw material input is expected. Losses have a realizable value of £5 per litre.The

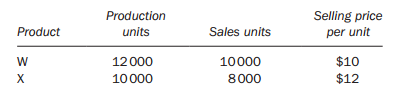

Two products (W and X) are created from a joint process. Both products can be sold immediately after split-off.There are no opening inventories or work in progress.The following information is available for last period:Total joint production costs $776 160 Using the sales value method of

In a process in which there are no work in progress stocks, two joint products (J and K) are created. Information (in units) relating to last month is as follows:Joint production costs last month were £110 000 and these were apportioned to the joint products based on the number of units produced.

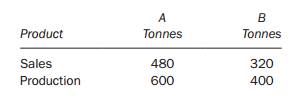

Two joint products A and B are produced in a process. Data for the process for the last period are as follows: Common production costs in the period were $12 000.There was no opening inventory. Both products had a gross profit margin of 40 per cent. Common production costs were apportioned on a

Why is budgeted activity the most widely used denominator measure?

Explain why the choice of an appropriate denominator level is important.

Identify and describe the four different denominator level measures that can be used to estimate fixed overhead rates.

Why is it necessary to select an appropriate denominator level measure only with absorption costing systems?

Explain how absorption costing can encourage managers to engage in behaviour that is harmful to the organization.

What arguments can be advanced in favour of absorption costing?

What arguments can be advanced in favour of variable costing?

Under what circumstances will variable costing report higher profits than absorption costing?

Under what circumstances will absorption costing report higher profits than variable costing?

Describe the circumstances when variable and absorption costing systems will report identical profits.

How are non-manufacturing fixed costs treated under absorption and variable costing systems?

Distinguish between variable costing and absorption costing.

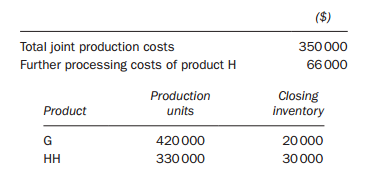

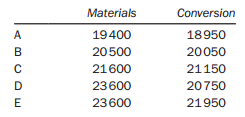

Two products G and H are created from a joint process. G can be sold immediately after split-off. H requires further processing into product HH before it is in a saleable condition.There are no opening inventories and no work in progress of products G, H or HH. The following data are available for

Describe the accounting treatment of by-products.

Explain the financial information that should be included in a decision as to whether a product should be sold at the split-off point or further processed.

Explain the factors that should influence the choice of method when allocating joint costs to products.

Why is the physical measure method considered to be an unsatisfactory joint cost allocation method?

Describe the four different methods of allocating joint costs to products.

Explain why it is necessary to allocate joint costs to products.

Provide examples of industries that produce both joint products and by-products.

Define joint costs, split-off point and further processing costs.

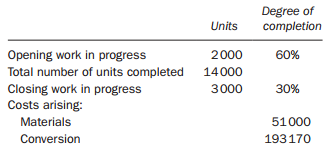

Yeoman Ltd uses process costing and the FIFO method of valuation. The following information for last month relates to Process G, where all the material is added at the beginning of the process:Opening work in progress: ........2000 litres (30 per cent complete in respect of in progress: conversion

CW Ltd makes one product in a single process.The details of the process for period 2 were as follows:There were 800 units of opening work in progress valued as follows:Material .......................................£98,000Labour .........................................£46,000Production

A company operates a process costing system using the first in, first out (FIFO) system of valuation. No losses occur in the process. The following data relate to last month:................................................................................UnitsOpening work in progress

Chemical Processors manufacture Wonderchem using two processes, mixing and distillation. The following details relate to the distillation process for a period:No opening work in progress (WIP) Closing WIP of 8000kg, which was 100 per cent complete for materials and 50 per cent complete for labour

‘No Friction’ is an industrial lubricant, which is formed by subjecting certain crude chemicals to two successive processes. The output of process 1 is passed to process 2, where it is blended with other chemicals. The process costs for period 3 were as follows:Process 1Material: 3000kg @

A company operates a process costing system using the first in, first out (FIFO) method of valuation. No losses occur in the process. All materials are input at the commencement of the process. Conversion costs are incurred evenly throughout the process.The following data relate to last

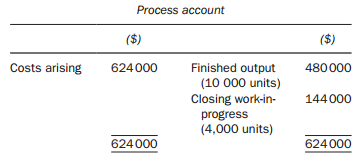

The following information is required for sub-questions (a) to (c).The incomplete process account relating to period 4 for a company which manufactures paper is shown below: There was no opening work in progress (WIP). Closing WIP, consisting of 700 units, was complete as shown:Material

The following details relate to the main process of W Limited, a chemical manufacturer:Opening work in progress ............2000 litres, fully complete as to materials and 40% complete as to conversionMaterial input ................................24 000 litresNormal losses are 10% of input (24 000

A company operates a process in which no losses are incurred. The process account for last month, when there was no opening work-in-progress, was as follows: The closing work in progress was complete to the same degree for all elements of cost.What was the percentage degree of completion of the

A company which operates a process costing system had work-in-progress at the start of last month of 300 units (valued at $1710) which were 60 percent complete in respect of all costs. Last month a total of 2000 units were completed and transferred to the finished goods warehouse. The cost per

A company uses process costing to value its output.The following was recorded for the period:Input materials ....................................2000 units at £4.50 per unitConversion costs ...............................£13,340Normal loss .........................................5% of input

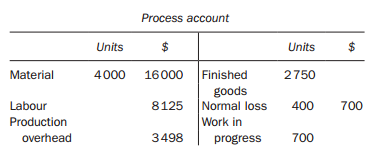

R makes one product, which passes through a single process. Details of the process account for period 1 were as follows:...........................................................$Material cost – 20 000kg ...........26,000Labour cost .................................12,000Production overhead cost

What are the implications for the accounting treatment of normal and abnormal losses if losses are assumed to be detected(a) At the end of the process, (b) Before the end of the process?

Explain the distinguishing features of a batch/operating costing system.

Why is it necessary to treat ‘previous process cost’ as a separate element of cost in a process costing.

Distinguish between normal and abnormal losses and explain how their accounting treatment differs.

(a) Explain the term ‘backflush accounting’ and the circumstances in which its use would be appropriate.(b) CSIX Ltd manufactures fuel pumps using a just-in-time manufacturing system which is supported by a backflush accounting system. The backflush accounting system has two trigger points for

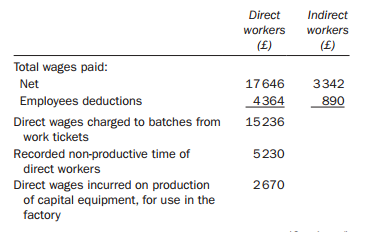

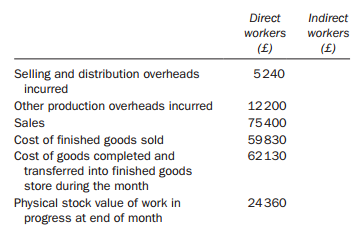

In the absence of the accountant you have been asked to prepare a month?s cost accounts for a company which operates a batch costing system fully integrated with the financial accounts. The cost clerk has provided you with the following information, which he thinks is

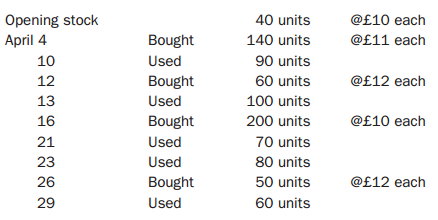

Z Ltd had the following transactions in one of its raw materials during April: You are required to:(a) Write up the stores ledger card using(i) FIFO and(ii) LIFOmethods of stock valuation.(b) State the cost of material used for each system during April.(c) Describe the weighted average method of

MN plc uses a JIT system and backflush accounting. It does not use a raw material stock control account.During April 1000 units were produced and sold. The standard cost per unit is £100: this includes materials of £45. During April £60 000 of conversion costs were incurred.The debit balance on

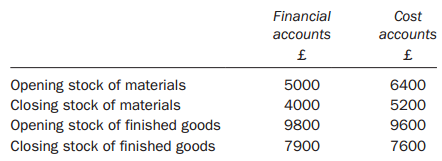

The following data have been taken from the books of CB plc, which uses a non-integrated accounting system: The effect of these stock valuation differences on the profit reported by the financial and cost accounting ledgers is that:(a) The financial accounting profit is ?300 greater than the cost

A company uses a blanket overhead absorption rate of $5 per direct labour hour. Actual overhead expenditure in a period was as budgeted.The under/over-absorbed overhead account for the period have the following entries: Which of the following statements is true?(a) Actual direct labour hours were

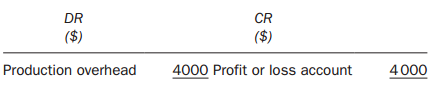

In an integrated bookkeeping system, when the actual production overheads exceed the absorbed production overheads, the accounting entries to close off the production overhead account at the end of the period would be:(a) Debit the production overhead account and credit the work in progress

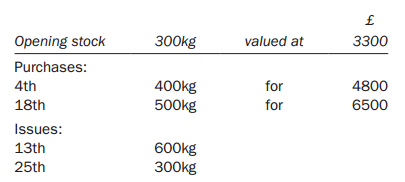

The following data relate to material J for last month: Using the LIFO valuation method, what was the value of the closing stock for last month?(a) ?3300(b) ?3500(c) ?3700(d) ?3900 £ Opening stock 300kg 3300 valued at Purchases: 400kg 500kg for 4800 4th 6500 18th for Issues: 13th 600kg 300kg 25th

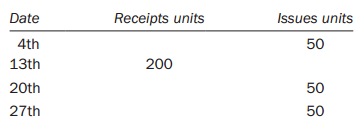

An organization?s records for last month show the following in respect of one store?s item: Last month?s opening stock was valued at a total of ?2900 and the receipts during the month were purchased at a cost of ?17.50 per unit.The organization uses the weighted average method of valuation and

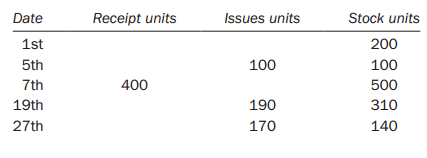

An organization?s stock records show the following transactions for a specific item during last month: The stock at the beginning of last month consisted of 100 units valued at ?6700.The receipts last month cost ?62 per unit.The value of the closing stock for last month has been calculated twice

Describe the major aims of backflush costing.

Explain the circumstances when backflush costing is used.

List the accounting entries for the payment and allocation of overheads.

List the accounting entries for the payment and the allocation of gross wages.

List the accounting entries for the purchase and issues of direct and indirect materials.

Explain the purpose of control accounts.

Explain the purpose of a stores ledger account.

Describe the first in, first out, last in, first out and average cost methods of stores pricing.

Distinguish between an integrated and interlocking accounting system.

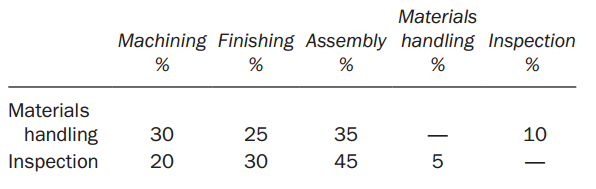

A company reapportions the costs incurred by two service cost centres, materials handling and inspection, to the three production cost centres of machining, finishing and assembly.The following are the overhead costs which have been allocated and apportioned to the five cost

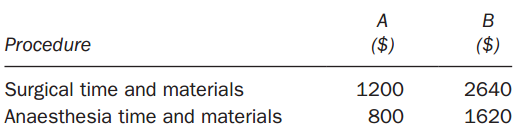

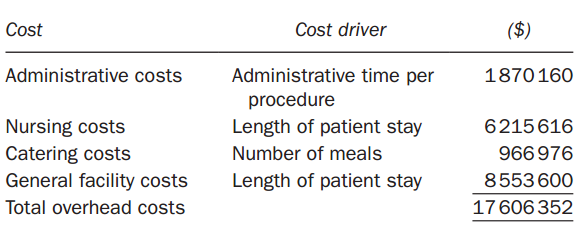

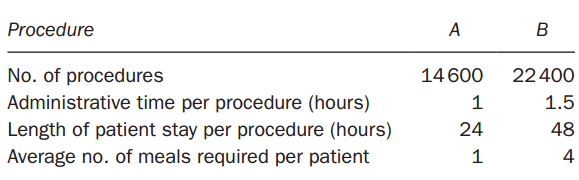

Beckley Hill (BH) is a private hospital carrying out two types of procedures on patients. Each type of procedure incurs the following direct costs: BH currently calculates the overhead cost per procedure by taking the total overhead cost and simply dividing it by the number of procedures, then

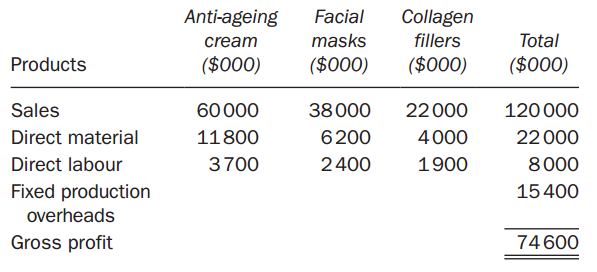

MS manufactures three types of skincare product for sale to retailers. MS currently operates a standard absorption costing system. Budgeted information for next year is given below: Fixed production overheads are absorbed using a direct material cost percentage rate.The management accountant of

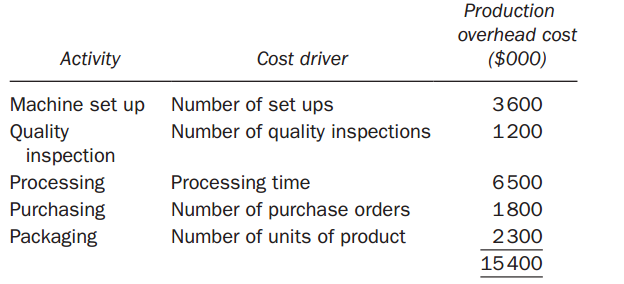

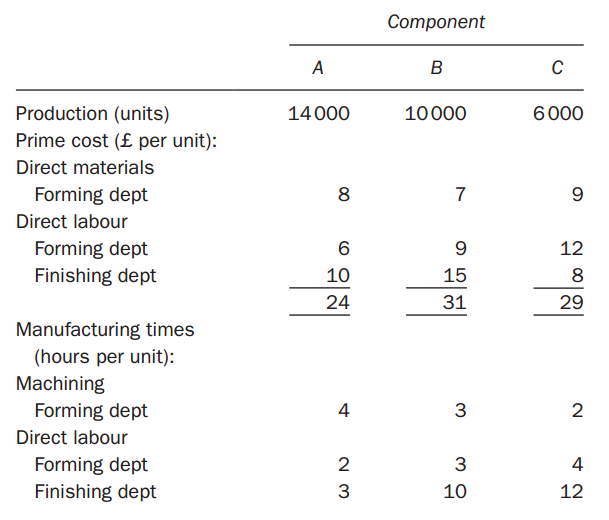

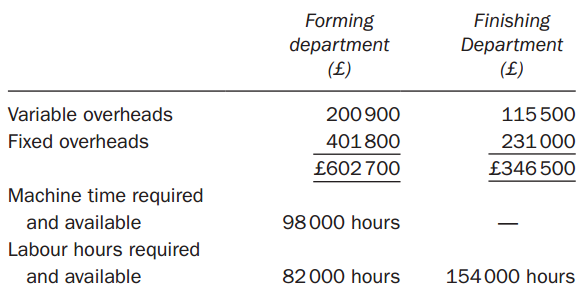

Shown below is next year?s budget for the forming and finishing departments of Tooton Ltd. The departments manufacture three different types of component, which are incorporated into the output of the firm?s finished products. The forming department is mechanized and employs only one grade of

A furniture making business manufactures quality furniture to customers? orders. It has three production departments and two service departments. Budgeted overhead costs for the coming year are as follows: ......................................................Total(?)Rent and rates

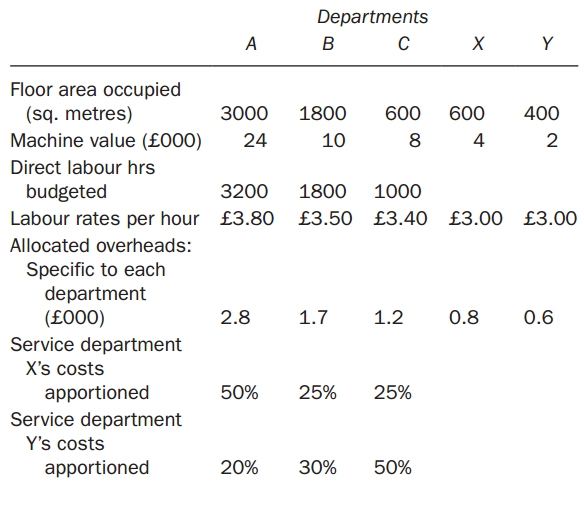

A factory consists of two production cost centres (P and Q) and two service cost centres (X and Y). The total allocated and apportioned overhead for each is as follows: It has been estimated that each service cost centre does work for other cost centres in the following proportions: The

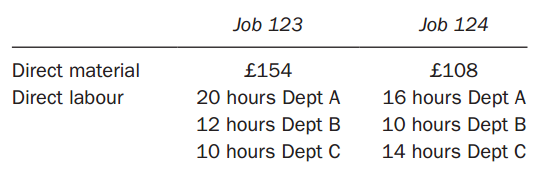

An engineering firm operates a job costing system.Production overhead is absorbed at the rate of $8.50 per machine hour. In order to allow for non-production overhead costs and profit, a mark-up of 60 per cent of prime cost is added to the production cost when preparing price estimates.The

Canberra has established the following information regarding fixed overheads for the coming month: Budgeted information:Fixed overheads..........................£180,000Labour hours.....................................3,000Machine hours.................................10,000Units of

A company absorbs overheads on machine hours. In a period, actual machine hours were 17,285, actual overheads were £496 500 and there was under-absorption of £12,520.What was the budgeted level of overheads?(a) £483,980(b) £496,500(c) £509,020(d) It cannot be calculated from the information

A company has over-absorbed fixed production overheads for the period by £6000. The fixed production overhead absorption rate was £8 per unit and is based on the normal level of activity of 5000 units. Actual production was 4,500 units.What was the actual fixed production overheads incurred for

A company uses an overhead absorption rate of $3.50 per machine hour, based on 32,000 budgeted machine hours for the period. During the same period the actual total overhead expenditure amounted to $108,875 and 30,000 machine hours were recorded on actual production.By how much was the total

A company uses a predetermined overhead recovery rate based on machine hours. Budgeted factory overhead for a year amounted to £720,000, but actual factory overhead incurred was £738,000. During the year, the company absorbed £714,000 of factory overhead on 119,000 actual machine hours.What was

Explain how the cost assignment approach described for manufacturing organizations can be extended to non-manufacturing organizations.

Give two reasons for the under-or over-recovery of overheads at the end of the accounting period.

Why are budgeted overhead rates preferred to actual overhead rates?

Why are some overhead costs sometimes not relevant for decision-making purposes?

Describe two important features that distinguish activity-based costing from traditional costing systems.

Define the term ‘activities’.

Describe the two-stage overhead allocation procedure.

Why are separate departmental or cost centre overhead rates preferred to a plant-wide (blanket) overhead rate?

Describe the process of assigning direct labour and direct materials to cost objects.

Explain why cost systems should differ in terms of their level of sophistication.

Explain how cost information differs for profit measurement/inventory valuation requirements compared with decision-making requirements.

Distinguish between arbitrary and cause-and-effect allocations.

Define cost tracing, cost allocation, allocation base and cost driver.

Why are indirect costs not directly traced to cost objects in the same way as direct costs?

Mrs Johnston has taken out a lease on a shop for a down payment of ?5000. Additionally, the rent under the lease amounts to ?5000 per annum. If the lease is cancelled, the initial payment of ?5000 is forfeit. Mrs Johnston plans to use the shop for the sale of clothing, and has estimated operations

(a) From the data below, you are required:(i) To prepare a schedule to be presented to management showing for the mileages of 5000, 10 000, 15 000 and 30 000 miles per annum:1. Total variable cost;2. Total fixed cost;3. Total cost;4. Variable cost per mile (in pence to nearest penny);5. Fixed cost

Distinguish between, and provide an illustration of:(i) ‘Avoidable’ and ‘unavoidable’ costs;(ii) ‘Cost centres’ and ‘cost units’.

Opportunity cost and sunk cost are among the concepts of cost commonly discussed. You are required:(i) To define these terms precisely;(ii) To suggest for each of them situations in which the concept might be applied;(iii) To assess briefly the significance of each of the concepts.

It is commonly suggested that a management accounting system should be capable of supplying different measures of cost for different purposes. You are required to set out the main types of purpose for which cost information may be required in a business organization and to discuss the alternative

‘Costs may be classified in a variety of ways according to their nature and the information needs of management.’ Explain and discuss this statement, illustrating with examples of the classifications required for different purposes.

(a) Describe the role of the cost accountant in a manufacturing organization.(b) Explain whether you agree with each of the following statements:(i) ‘All direct costs are variable.’(ii) ‘Variable costs are controllable and fixed costs are not.’(iii) ‘Sunk costs are irrelevant when

Cost classifications used in costing include:(i) Period costs;(ii) Product costs;(iii) Variable costs;(iv) Opportunity costs.Required:Explain each of these classifications, with examples of the types of cost that may be included.

Prepare a report for the managing director of your company explaining how costs may be classified by their behaviour, with particular reference to the effects both on total and on unit costs. Your report should:(i) Say why it is necessary to classify costs by their behaviour; and(ii) be illustrated

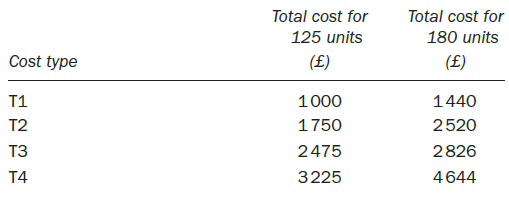

A manufacturing company has four types of cost (identified as T1, T2, T3 and T4). The total cost for each type at two different production levels is: Which cost types would be classified as being semi-variable? (a) T1(b) T2(c) T3(d) T4 Total cost for Total cost for 180 units 125 units (£) Cost

Fixed costs are conventionally deemed to be:(a) Constant per unit of output;(b) Constant in total when production volume changes;(c) Outside the control of management;(d) Those unaffected by inflation.

Which one of the following would be classified as indirect labour?(a) Assembly workers on a car production line;(b) Bricklayers in a house building company;(c) Machinists in a factory producing clothes;(d) Forklift truck drivers in the stores of an engineering company.

Which ONE of the following costs would NOT be classified as a production overhead cost in a food processing company?(a) The cost of renting the factory building;(b) The salary of the factory manager;(c) The depreciation of equipment located in the materials store;(d) The cost of ingredients.

The audit fee paid by a manufacturing company would be classified by that company as:(a) A production overhead cost;(b) A selling and distribution cost;(c) A research and development cost;(d) An administration cost.

Showing 2500 - 2600

of 2716

First

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Step by Step Answers