New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

principles corporate finance

Fundamentals Of Futures And Options Markets 4th Edition John C. Hull - Solutions

5.8. Suppose that 6-month, 12-month, 18-month, 24-month, and 30-month zero rates are 4%, 4.2%, 4.4%, 4.6%, and 4.8% per annum with continuous compounding respectively. Estimate the cash price of a bond with a face value of 100 that will mature in 30 months pays a coupon of 4% per annum semiannually.

5.9. A three-year bond provides a coupon of 8% semiannually and has a cash price of 104. What is the bond yield?

5.10. Suppose that the 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 6%, 6.5%, and 7% respectively. What is the two-year par yield?

5.11. Explain carefully why liquidity preference theory is consistent with the observation that the term structure tends to be upward sloping more often than it is downward sloping.

5.12. Suppose that zero interest rates with continuous compounding are as follows:Calculate forward interest rates for the second, third, fourth, and fifth years. Maturity (years) 1 2 3 Rate (% per annum) 12.0 13.0 13.7 4 14.2 5 14.5

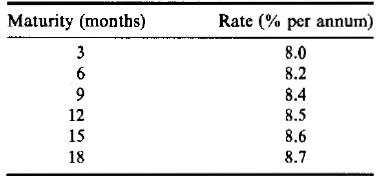

5.13. Suppose that zero interest rates with continuous compounding are as follows:Calculate forward interest rates for the second, third, fourth, fifth, and sixth quarters. Maturity (months) 3 6 Rate (% per annum) 8.0 8.2 12 15 9258 8.4 8.5 8.6 18 8.7

5.16. It is May 5, 2003. The quoted price of a government bond with a 12% coupon that matures on July 27, 2011, is 110-17. What is the cash price?

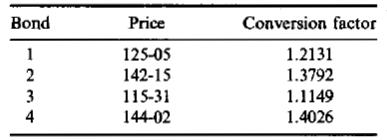

5.17. Suppose that the Treasury bond futures price is 101-12. Which of the following four bonds is cheapest to deliver? Bond Price Conversion factor 1234 125-05 1.2131 2 142-15 1.3792 3 115-31 1.1149 4 144-02 1.4026

5.18. It is July 30, 2001. The cheapest-to-deliver bond in a September 2001 Treasury bond futures contract is a 13% coupon bond, and delivery is expected to be made on September 30, 2001. Coupon payments on the bond are made on February 4 and August 4 each year. The term structure is flat, and the

5.20. Assuming that zero rates are as in Problem 5.13, what is the value of an FRA that enables the holder to earn 9.5% for a three-month period starting in one year on a principal of $1,000,000? The interest rate is expressed with quarterly compounding.

5.21. Suppose that the nine-month LIBOR interest rate is 8% per annum and the six-month LIBOR interest rate is 7.5% per annum (both with continuous compounding). Estimate the three-month Eurodollar futures price quote for a contract maturing in six months.

5.26. How can the portfolio manager change the duration of the portfolio to 3.0 years in Problem 5.25?

5.27. Between February 28, 2002, and March 1, 2002, you have a choice between owning a government bond paying a 10% coupon and a corporate bond paying a 10% coupon. Consider carefully the day count conventions discussed in this chapter and decide which of the two bonds you would prefer to own.

5.31. Assume that a bank can borrow or lend money at the same interest rate in the LIBOR market. The 91-day rate is 10% per annum, and the 182-day rate is 10.2% per annum. both expressed with continuous compounding. The Eurodollar futures price for a contract maturing in 91 days is quoted as 89.5.

5.32. A Canadian company wishes to create a Canadian LIBOR futures contract from a U.S. shes to create a Canadi Eurodollar futures contract and forward contracts on foreign exchange. Using an example, explain how the company should proceed. For the purposes of this problem, assume that a futures

5.33. Portfolio A consists of a one-year zero-coupon bond with a face value of $2,000 and a 10-year zero-coupon bond with a face value of $6,000. Portfolio B consists of a 5.95-year discount bond with a face value of $5,000. The current yield on all bonds is 10% per annum.a. Show that both

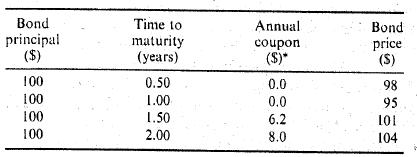

5.34. The following table gives the prices of bonds:a. Calculate zero rates for maturities of 6 months, 12 months, 18 months, and 24 months.b. What are the forward rates for the periods: 6 months to 12 months, 12 months to 18 months, 18 months to 24 months?c. What are the 6-month, 12-month,

5.35. It is June 25, 2001. The futures price for the June 2001 CBOT bond futures contract is 118-23.a. Calculate the conversion factor for a bond maturing on January 1, 2017, paying a coupon of 10%.b. Calculate the conversion factor for a bond maturing on October 1, 2022, paying a coupon of 7%.c.

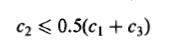

8.22. Suppose that c1, c2, and c3 are the prices of European call options with strike prices X1, X2, and X3, respectively, where X3 > X2 > X1 and X3 - X2 = X2 - X. All options have the same maturity. Show that(Hint: Consider a portfolio that is long one option with strike price X1, long one

11.10. Prove that, with the notation in the chapter, a 95% confidence interval for Sr is between Soe-2/2)T-1.960T and Soe (-02/2)T+1.960T

11.12. Assume that a non-dividend-paying stock has an expected return of and a volatility of . An innovative financial institution has just announced that it will trade a derivative that pays off a dollar amount equal toat time T. The variables So and Sr denote the values of the stock price at time

11.19. A stock price is currently $50 and the risk-free interest rate is 5%. Use the DerivaGem software to translate the following table of European call options on the stock into a table of implied volatilities, assuming no dividends. Are the option prices consistent with Black-Scholes? Maturity

12.1. A portfolio is currently worth $10 million and has a beta of 1.0. The S&P 100 is currently standing at 800. Explain how a put option on the S&P 100 with a strike price of 700 can be used to provide portfolio insurance.

12.5. Explain how corporations can use currency options to hedge their foreign exchange risk.

12.8. Suppose that an exchange constructs a stock index that tracks the return, including dividends, on a certain portfolio. Explain how you would value (a) futures contracts and (b) European options on the index.

12.9. A foreign currency is currently worth $1.50. The domestic and foreign risk-free interest rates are 5% and 9%, respectively. Calculate a lower bound for the value of a six-month call option on the currency with a strike price of $1.40 if it is (a) European and (b) American.

2.12. Show that if C is the price of an American call with exercise price X and maturity T on a stock paying a dividend yield of q, and P is the price of an American put on the same stock with the same strike price and exercise date,where So is the stock price, r is the risk-free rate, and r >

12.13. Show that a call option on a currency has the same price as the corresponding put option on the currency when the forward price equals the strike price.

12.18. Use the DerivaGem software to calculate implied volatilities for the June 100 call and the June 100 put on the Dow Jones Industrial Average in Table 12.1. The value of the DJX on March 15, 2001, was 100.31. Assume the risk-free rate was 4.5%, the dividend yield was 2%. The options expire on

12.19. A stock index currently stands at 300. It is expected to increase or decrease by 10% over each of the next two time periods of three months. The risk-free interest rate is 8% and the dividend yield on the index is 3%. What is the value of a six-month put option on the index with a strike

12.20. Suppose that the spot price of the Canadian dollar is U.S. $0.75 and that the Canadian dollar/U.S. dollar exchange rate has a volatility of 4% per annum. The risk-free rates of interest in Canada and the United States are 9% and 7% per annum, respectively. Calculate the value of a European

12.21. A mutual fund announces that the salaries of its fund managers will depend on the performance of the fund. If the fund loses money, the salaries will be zero. If the fund makes a profit, the salaries will be proportional to the profit. Describe the salary of a fund manager as an option. How

11.26. Assume that the stock in Problem 11.25 is due to go ex-dividend in 1.5 months. The expected dividend is 50 cents.a. What is the price of the option if it is a European call?b. What is the price of the option if it is a European put?c. Use the results in the Appendix to this chapter to

1.24. A financial institution plans to offer a derivative that pays off a dollar amount equal to Sat time T where Sr is the stock price at time T. Assume no dividends. Defining other variables as necessary use risk-neutral valuation to calculate the price of the derivative at time zero. (Hint: The

11.22. A stock price is currently $50. Assume that the expected return from the stock is 18% per annum and its volatility is 30% per annum. What is the probability distribution for the stock price in two years? Calculate the mean and standard deviation of the distribution. Determine 95% confidence

11.21. Show that the probability that a European call option will be exercised in a risk-neutral world is, with the notation introduced in this chapter, N(d2). What is an expression for the value of a derivative that pays off $100 if the price of a stock at time T is greater than X?

11.20. Show that the Black-Scholes formulas for call and put options satisfy put-call parity.

11.16. Show that the Black-Scholes formula for a call option gives a price that tends to max (So - X, 0) as T→ 0.

11.15. A call option on a non-dividend-paying stock has a market price of $2.50. The stock price is $15, the exercise price is $13, the time to maturity is three months, and the risk- free interest rate is 5% per annum. What is the implied volatility?

11.14. What is the price of a European put option on a non-dividend-paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum, and the time to maturity is six months?

11.13. What is the price of a European call option on a non-dividend-paying stock when the stock price is $52, the strike price is $50, the risk-free interest rate is 12% per annum, the volatility is 30% per annum, and the time to maturity is three months?

11.11. A portfolio manager announces that the average of the returns realized in each of the last 10 years is 20% per annum. In what respect is this statement misleading?

11.7. What is Black's approximation for valuing an American call option on a dividend- paying stock?

11.6. What is meant by implied volatility? How would you calculate the volatility implied by a European put option price?

11.5. What difference does it make to your calculations in the previous question if a dividend of $1.50 is expected in two months?

11.3. Explain how risk-neutral valuation could be used to derive the Black-Scholes formulas.

11.2. The volatility of a stock price is 30% per annum. What is the standard deviation of the percentage price change in one trading day?

11.1. What does the Black-Scholes stock option pricing model assume about the probability distribution of the stock price in one year? What does it assume about the continuously compounded rate of return on the stock during the year?

10.16. Using a "trial-and-error" approach, estimate how high the strike price has to be in Problem 10.16 for it to be optimal to exercise the option immediately.

10.13. A stock price is currently $25. It is known that at the end of two months it will be either $23 or $27. The risk-free interest rate is 10% per annum with continuous compounding. Suppose S7 is the stock price at the end of two months. What is the value of a derivative that pays off at this

10.12. For the situation considered in Problem 10.11, what is the value of a six-month European put option with a strike price of $51? Verify that the European call and European put prices satisfy put-call parity. If the put option were American, would it ever be optimal to exercise it early at any

10.6. For the situation considered in Question 10.5, what is the value of a one-year European put option with a strike price of $100? Verify that the European call and European put prices satisfy put-call parity.

10.4. A stock price is currently $50. It is known that at the end of six months it will be either $45 or $55. The risk-free interest rate is 10% per annum with continuous compound- ing. What is the the value of a six-month European put option with a strike price of $50?

10.3. What is meant by the delta of a stock option?

9.20. A diagonal spread is created by buying a call with strike price X2 and exercise date 72 and selling a call with strike price X and exercise date T (T2 > T). Draw a diagram showing the profit when (a) X2 > X and (b) X2 < X1.

9.17. What is the result if the strike price of the put is higher than the strike price of the call in a strangle?

9.16. A box spread is a combination of a bull call spread with strike prices X and X2 and a bear put spread with the same strike prices. The expiration dates of all options are the same. What are the characteristics of a box spread?

9.15. How can a forward contract on a stock with a particular delivery price and delivery date be created from options?

9.13. Construct a table showing the payoff from a bull spread when puts with strike prices X and X2 are used (X2 > X1).

9.11. Use put-call parity to show that the cost of a butterfly spread created from European puts is identical to the cost of a butterfly spread created from European calls.

9.9. Explain how an aggressive bear spread can be created using put options.

9.6. What is the difference between a strangle and a straddle?

9.5. What trading strategy creates a reverse calendar spread?

9.3. When is it appropriate for an investor to purchase a butterfly spread?

9.2. Explain two ways in which a bear spread can be created.

9.1. What is meant by a protective put? What position in call options is equivalent to a protective put?

8.23. What is the result corresponding to that in Problem 8.22 for European put options?

8.20. Use the software DerivaGem to verify that Figures 8.1 and 8.2 are correct.

8.19. Even when the company pays no dividends, there is a tendency for executive stock options to be exercised early. (See Section 7.12 for a discussion of executive stock options.) Give a possible reason for this.

8.18. Prove the result in equation (8.8). (Hint: For the first part of the relationship consider (a) a portfolio consisting of a European call plus an amount of cash equal to D+ X and (b) a portfolio consisting of an American put option plus one share.)

8.17. Prove the result in equation (8.4). (Hint: For the first part of the relationship consider (a) a portfolio consisting of a European call plus an amount of cash equal to X and (b) a portfolio consisting of an American put option plus one share.)

8.16. Explain carefully the arbitrage opportunities in Problem 8.15 if the American put price is greater than the calculated upper bound.

8.14. Explain carefully the arbitrage opportunities in Problem 8.13 if the European put price is $3.

8.12. Give an intuitive explanation of why the early exercise of an American put becomes more attractive as the risk-free rate increases and volatility decreases.

8.6. Explain why an American call option is always worth at least as much as its intrinsic value. Is the same true of a European call option? Explain your answer.

8.1. List the six factors affecting stock option prices.

7.23. A United States investor buys 500 shares of a stock and sells five call option contracts on the stock. The strike price is $30. The price of the option is $3. What is the investor's minimum cash investment (a) if the stock price is $28 and (b) if it is $32?

7.21. Explain why the market maker's bid-offer spread represents a real cost to options investors.

7.20. Options on General Motors stock are on a March, June, September, and December cycle. What options trade on (a) March 1, (b) June 30, and (c) August 5?

7.19. What is the effect of an unexpected cash dividend on (a) a call option price and (b) a put option price?

7.18. "If most of the call options on a stock are in the money, it is likely that the stock price has risen rapidly in the last few months." Discuss this statement.

7.16. Suppose that sterling-U.S. dollar spot and forward exchange rates are as follows: Spot 90-day forward 180-day forward 1.8470 1.8381 1.8291 What opportunities are open to an investor in the following situations?a. A 180-day European call option to buy 1 for $1.80 costs $0.0250.b. A 90-day

7.14. Explain carefully the difference between writing a call option and buying a put option.

7.13. Explain why an American option is always worth at least as much as its intrinsic value.

7.12. Explain why an American option is always worth at least as much as a European option on the same asset with the same strike price and exercise date.

7.7. A corporate treasurer is designing a hedging program involving foreign currency options. What are the pros and cons of using (a) the Philadelphia Stock Exchange and (b) the over-the-counter market for trading?

7.6. A company declares a 3-for-1 stock split. Explain how the terms change for a call option with a strike price of $60.

7.5. A stock option is on a February, May, August, and November cycle. What options trade on (a) April 1 and (b) May 30?

7.4. Explain why brokers require margins when clients write options but not when they buy options.

7.3. An investor buys a call with strike price of X and writes a put with the same strike price. Describe the investor's position.

6.21. Suppose that the term structure of interest rates is flat in the United States and Australia. The USD interest rate is 7% per annum and the AUD rate is 9% per annum. The current value of the AUD is 0.62 USD. Under the terms of a swap agreement, a financial institution pays 8% per annum in AUD

6.20. Under the terms of an interest rate swap, a financial institution has agreed to pay 10% per annum and to receive three-month LIBOR in return on a notional principal of $100 million with payments being exchanged every three months. The swap has a remaining life of 14 months. The average of the

6.18. The one-year LIBOR rate is 10%. A bank trades swaps where a fixed rate of interest is exchanged for 12-month LIBOR with payments being exchanged annually. Two- and three-year swap rates (expressed with annual compounding) are 11% and 12% per annum. Estimate the two- and three-year LIBOR zero

6.17. The LIBOR zero curve is flat at 5% (continuously compounded) out to 1.5 years. Swap rates for 2- and 3-year semiannual pay swaps are 5.4% and 5.6%, respectively. Estimate the LIBOR zero rates for maturities of 2.0, 2.5, and 3.0 years. (Assume that the 2.5-year swap rate is the average of the

6.16. Explain how you would value a swap that is the exchange of a floating rate in one currency for a fixed rate in another currency.

6.15. A bank finds that its assets are not matched with its liabilities. It is taking floating-rate deposits and making fixed-rate loans. How can swaps be used to offset the risk?

6.14. Why is the expected loss from a default on a swap less than the expected loss from the default on a loan with the same principal?

6.12. After it hedges its foreign exchange risk using forward contracts, is the financial institution's average spread in Figure 6.10 likely to be greater than or less than 20 basis points? Explain your answer.

6.10. A financial institution has entered into a 10-year currency swap with company Y. Under the terms of the swap, it receives interest at 3% per annum in Swiss francs and pays interest at 8% per annum in U.S. dollars. Interest payments are exchanged once a year. The principal amounts are 7

6.9. A financial institution has entered into an interest rate swap with company X. Under the terms of the swap, it receives 10% per annum and pays six-month LIBOR on a principal of $10 million for five years. Payments are made every six months. Suppose that company X defaults on the sixth payment

Showing 700 - 800

of 5445

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers