The Dunley Corp. plans to issue 5-year bonds. It believes the bonds will have a BBB rating.

Question:

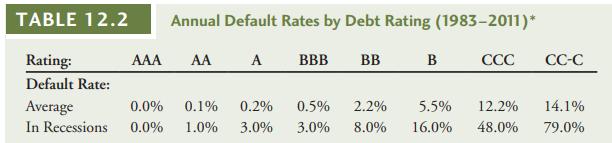

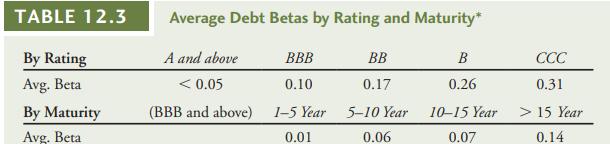

The Dunley Corp. plans to issue 5-year bonds. It believes the bonds will have a BBB rating. Suppose AAA bonds with the same maturity have a 4% yield. Assume the market risk premium is 5% and use the data in Table 12.2 and Table 12.3.

a. Estimate the yield Dunley will have to pay, assuming an expected 50% loss rate in the event of default during average economic times. What spread over AAA bonds will it have to pay?

b. Estimate the yield Dunley would have to pay if it were a recession, assuming the expected loss rate is 71% at that time, but the beta of debt and market risk premium are the same as in average economic times. What is Dunley’s spread over AAA now?

c. In fact, one might expect risk premia and betas to increase in recessions. Redo part (b)

assuming that the market risk premium and the beta of debt both increase by 20%; that is, they equal 1.2 times their value in recessions.

Table 12.2

Table 12.3

Step by Step Answer:

Corporate Finance The Core

ISBN: 9781292158334

4th Global Edition

Authors: Jonathan Berk, Peter DeMarzo