Using the implied volatility you calculated in Problem 14, and the information in that problem, use the

Question:

Using the implied volatility you calculated in Problem 14, and the information in that problem, use the Black-Scholes option pricing formula to calculate the value of the 800 January 2014 call option.

Problem 14

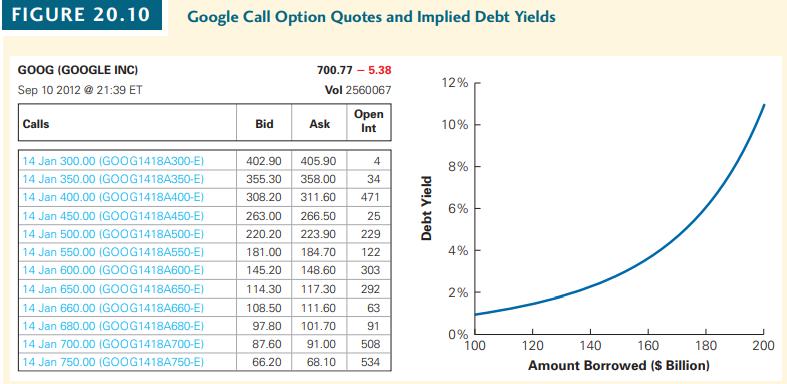

Using the market data in Figure 20.10 and a risk-free rate of 0.25% per annum, calculate the implied volatility of Google stock in September 2012, using the bid price of the 700 January 2014 call option.

Figure 20.10

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Aqib Parvej

I am teaching since my graduation time so I have teaching experience of about 5 years and in these years I learn to teach in the best and interesting way .

20+ Reviews

41+ Question Solved

Related Book For

Corporate Finance The Core

ISBN: 9781292158334

4th Global Edition

Authors: Jonathan Berk, Peter DeMarzo

Question Posted: