It is 19 December, and a UK company is expecting to receive $1m in three months time

Question:

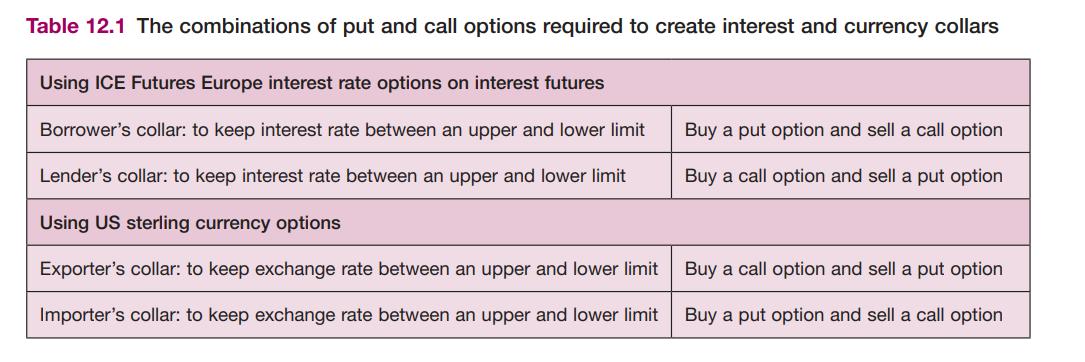

It is 19 December, and a UK company is expecting to receive $1m in three months’ time in payment for exports. The company wants to guard against the pound appreciating against the dollar, which currently stands at $1.65/£. As sterling currency options are not available on ICE Futures Europe, the company will have to use US currency options. It decides to use CME sterling currency options, which have futures contracts as the underlying asset. These come in contract sizes of £62,500 and require physical delivery of the currency. From the US perspective, sterling is the foreign currency and so the company will buy call options. By buying sterling currency call options, the company obtains the right, but not the obligation, to sell dollars and buy sterling at an exchange rate of $1.65 to the pound. To find how many contracts are needed, the future dollar receipt is converted to pounds at the option strike price, giving £606,061 (i.e. $1m/$1.65), and then divided by the standard contract size, giving the number of contracts needed as 9.7 (i.e. £606,061/£62,500). It is impossible to get a perfect hedge here owing to the standard size of the contracts. The company must either under-hedge by buying nine contracts or over-hedge by buying ten contracts. Any shortfalls or excess amounts of dollars can be dealt with via forward exchange contracts or currency market transactions when the options are exercised. Assume that the company decides to buy 10 contracts. If March sterling currency call options with a $1.65 strike price are currently trading at a premium of 7 cents (per pound of contract), the total cost of 10 contracts will be:

![]()

By buying March sterling currency call options with a $1.65 strike price the company will, in the worst case, exchange its dollars at a rate of $1.72 to the pound (i.e. $1.65 plus the 7 cents premium). If, in three months’ time, the spot rate is below $1.65/£, the company will allow the option to expire and exchange its dollars in the spot market. Conversely, if the company had imported goods and therefore needed to buy dollars in three months’ time, it would buy US sterling currency put options, giving it the option to sell sterling and receive dollars at a predetermined rate.

Step by Step Answer:

Based on the information you provided heres how to calcula...View the full answer

Corporate Finance Principles And Practice

ISBN: 9781292450940

9th Edition

Authors: Denzil Watson, Antony Head