When talking about the group financial statements the consolidated financial statements include Consolidated Income Statement that a parent must prepare among other sets of consolidated financial statements. Consolidated Income statement that is also called consolidated statement of comprehensive income or CSOCI.

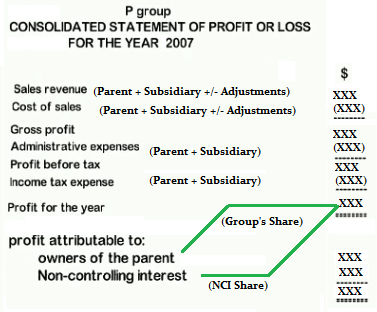

Format of Consolidated Income Statement

Both parent's and subsidiary's income statement items are added together on the face of the consolidated income statement as follows.

Important Terms

The consolidated income statement questions will include some important and new terms unlike a simple income statement.

Intra-group transactions

When a parent or subsidiary buy or sell goods or exchange assets within the group, such transactions are called intra-group transactions. Since the group is considered as a single reporting entity that is why the intra-group transactions occurring at profit are required to be adjusted for any unrealized profits.

Excess Depreciation and Amortization

When a non current tangible or intangible asset is transferred from parent or subsidiary at a price above the cost of the asset gives rise to unrealized profit to the seller. This Unrealized profit needs to be adjusted on the face of the income statement.

Incomes from Subsidiaries

Since the parent controls the subsidiary's shares and hence receives dividends from the subsidiary that is separately shown in parent's other income section. This part is not included in the consolidated income statement because the Parent and subsidiary both are a single entity.

Impairment of Goodwill

As the parent acquires control over subsidiary normally goodwill arises. The Income statement must incorporate any impairment on goodwill at the end of the accounting period.

Distribution of profits to NCI and Group

The profits of subsidiaries are distributed to NCI at the end of the consolidated income statement as per the percentage of subsidiary's shares owned by NCI. For this reason the subsidiary's profits are adjusted for effects of intragroup transactions and then the share of NCI is given out of this adjusted profit. The remaining amount of consolidated profits belongs to the Parent company or group owners.

Learn more about consolidated income statement with a solved example.

Consolidated Income Statement | Accounting | SolutionInn Premium Tutors

Still want to learn more about Consolidated Income Statement

Checkout other online study materials on SolutionInn

Related solved question answer on Consolidated Income Statement

Base your answers to the following questions on the financial statements for Dollarama Inc. in...... consolidatedstatement of net earnings and comprehensive income and explain where the additional revenue went.

Ada Vidal established Exotic Bean Bags Inc. (EBBI) in 20X2 to distribute exotic bean bags...... consolidated... value. – No dividends were declared by ER during the year. Required Draft a report for the AE partner that includes the...

RONA Inc. is a major Canadian retailer of hardware, building supplies, and home renovation...... consolidated... it improved? c. Does RONA present its expenses by function or by nature? Does this approach require a higher level of management...

The Project Data file provided for you contains information that you may use to help you complete...... consolidated... 142 Total assets Accounts payable Notes payable Long-term debt Bonds payable 2$ 52 2$ 37 50 300 400 250 250 262 6 years Common...

The Zetar plc's complete annual report, including the notes to its financial statements, is available in the Investors section at www.zetarplc.com. Describe in which statement each of the following items is reported, and the position in the...

The Zetar plc's complete annual report, including the notes to its financial statements, is available in the Investors section at www.zetarplc.com. Describe in which statement each of the following items is reported, and the position in the...

Samsung’s statement of cash flows in Appendix A reports the change in cash and equivalents for the year ended December 31, 2017. Identify the cash generated (or used) by operating activities, by investing activities,and by financing...

Refer to the statement of cash flows for Samsung in Appendix A. For the year ended December 31, 2017, what was the amount for repayment of long-term borrowings and debentures? Data from Samsung

Refer to Samsung’s 2017 statement of cash flows in Appendix A. List its cash flows from operating activities,investing activities, and financing activities. Data from Samsung

Learn the step-by-step answers to your textbook problems, just enter our Solution Library containing more than 3 Million+ textbooks solutions and help guides from over 1300 courses.

24/7 Online Tutors

Tune up your concepts by asking our tutors any time around the clock and get prompt responses.