Assume the Black-Scholes framework. Consider a 3-month European contingent claim on a stock. You are given: (i)

Question:

Assume the Black-Scholes framework. Consider a 3-month European contingent claim on a stock.

You are given:

(i) The stock is currently selling for 50.

(ii) The stock will pay a single dividend of 1.5 in two months.

(iii) Var[ln FPt,0.25(S)] = 0.09t, for 0 ≤ t ≤ 0.25.

(iv) The continuously compounded risk-free interest rate is 10%.

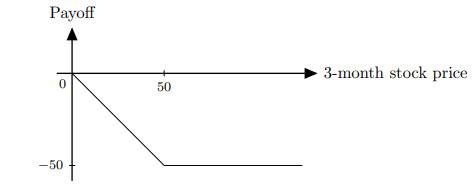

(v) The 3-month payoff of the contingent claim is as follows:

Calculate the profit on the contingent claim if the 3-month stock price is 45.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Observe that the 3month payoff of the contingent claim w...View the full answer

Answered By

GERALD KAMAU

non-plagiarism work, timely work and A++ work

6+ Reviews

11+ Question Solved

Related Book For

Question Posted: