Assume the Black-Scholes framework. For t 0, let S(t) be the time-t price of a nondividend-paying

Question:

Assume the Black-Scholes framework. For t ≥ 0, let S(t) be the time-t price of a nondividend-paying stock. You are given:

(i) S(0) = 180.

(ii) The stock’s volatility is 20%.

(iii) The continuously compounded expected rate of return on the stock is 8%.

(iv) The continuously compounded risk-free interest rate is 5%.

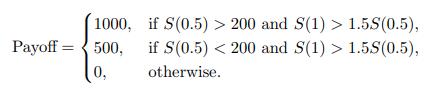

Consider a 1-year European partial cash-or-nothing option on the stock. The option’s payoff is

Calculate the time-0 price of this option.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

By riskneutral pricing the 6month price of the special 1year derivative ...View the full answer

Answered By

Shem Ongek

I am a professional who has the highest levels of self-motivation. Additionally, I am always angled at ensuring that my clients get the best of the quality work possible within the deadline. Additionally, I write high quality business papers, generate quality feedback with more focus being on the accounting analysis. I additionally have helped various students here in the past with their research papers which made them move from the C grade to an A-grade. You can trust me 100% with your work and for sure I will handle your papers as if it were my assignment. That is the kind of professionalism that I swore to operate within. I think when rating the quality of my work, 98% of the students I work for always come back with more work which therefore makes me to be just the right person to handle your paper.

174+ Reviews

426+ Question Solved

Related Book For

Question Posted: