Question: Prediction in the serially correlated error component model. For the BLU predictor of (y_{i, T+1}) given in (5.25), show that when (v_{i t}) follows (a)

Prediction in the serially correlated error component model. For the BLU predictor of \(y_{i, T+1}\) given in (5.25), show that when \(v_{i t}\) follows

(a) the AR(1) process, the GLS predictor is corrected by the term in (5.26);

(b) the AR(2) process, the GLS predictor is corrected by the term given in (5.27);

(c) the specialized AR(4) process, the GLS predictor is corrected by the term given in (5.28);

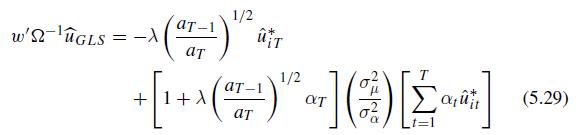

(d) the MA(1) process, the GLS predictor is corrected by the term given in (5.29).

![]()

i.T+1 = ZT+18GLS + w'uGLS (5.25)

Step by Step Solution

★★★★★

3.28 Rating (154 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock