Question: Take the linear model Y X0e with E[Ze] 0. Consider the GMM estimator b of . Let J n g n( b)0b

Take the linear model Y Æ X0¯Åe with E[Ze] Æ 0. Consider the GMM estimator b¯ of ¯.

Let J Æ n g n( b¯)0b

¡1g n( b¯) denote the test of overidentifying restrictions. Show that J ¡!

d

Â2

`¡k as n !1 by demonstrating each of the following.

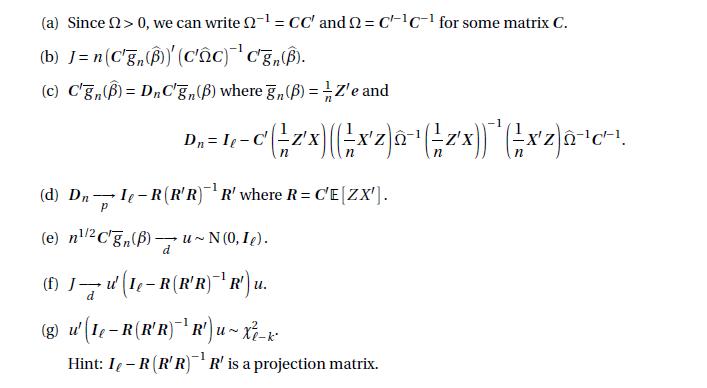

(a) Since > 0, we can write 2-1 = CC' and Q = CC-1 for some matrix C. (b) J= n(C'gn(B))' (C'c)C'gn(B). (c) C'gn(B) = DnC'gn() where (B)=Z'e and (d) Dn - P n D= 1-czxxz0zx))(x) Z'X -X'Z - I - R (R'R) R' where R = C'E[ZX']. (e) ncgn() -U~ (0,1). (f) Ju' (Le-R (R'R) R') u. - d (g) u' (le-R (RR) R') u ~ X-k -1 Hint: I-R (RR) R' is a projection matrix.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock