Positively correlated residuals often occur when models are estimated using economic time series data. The residuals for

Question:

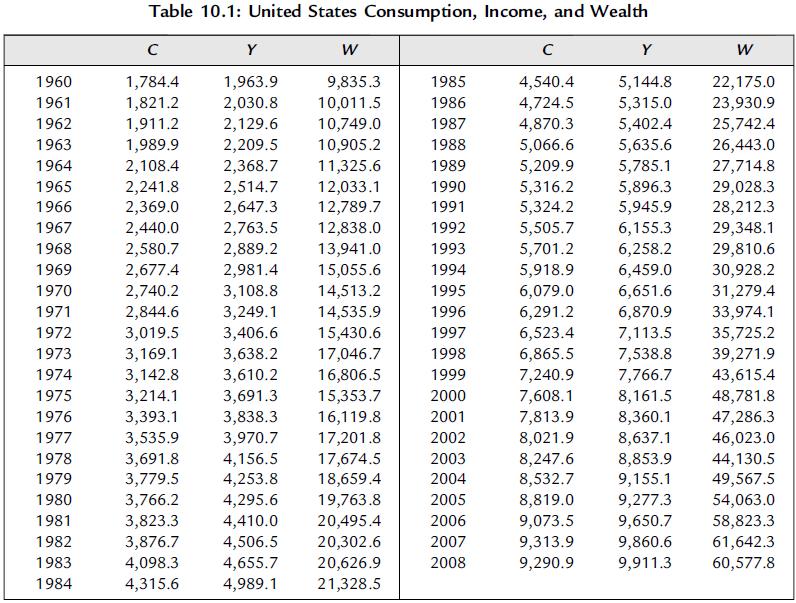

Positively correlated residuals often occur when models are estimated using economic time series data. The residuals for the consumption function estimated in this chapter turn out to be positively correlated, in that positive prediction errors tend to be followed by positive prediction errors and negative prediction errors tend to be followed by negative prediction errors. This problem can often be solved by working with changes in the values of the variables rather than the levels:![]()

Use the data in Table 10.1 to calculate the changes in C, Y, and W; for example, the value of C − C(−1) in 1961 is 1,821.2 − 1,784.4 = 36.8.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Antony Mutonga

I am a professional educator and writer with exceptional skills in assisting bloggers and other specializations that necessitate a fantastic writer. One of the most significant parts of being the best is that I have provided excellent service to a large number of clients. With my exceptional abilities, I have amassed a large number of references, allowing me to continue working as a respected and admired writer. As a skilled content writer, I am also a reputable IT writer with the necessary talents to turn papers into exceptional results.

2+ Reviews

10+ Question Solved

Related Book For

Essential Statistics Regression And Econometrics

ISBN: 9780123822215

1st Edition

Authors: Gary Smith

Question Posted: