In January 2017, Susan and Clark Shipley, co-owners of Island Foods, Inc. began discussing the possibility of

Question:

In January 2017, Susan and Clark Shipley, co-owners of Island Foods, Inc. began discussing the possibility of expanding their restaurant business from a single location in Glendale, Arizona, to two additional locations—one in Scottsdale and a second in Phoenix.

Although the Glendale restaurant had only been open for about two years, it had attracted a loyal customer base from neighborhood businesses and schools. Despite the success of the Glendale restaurant in its first two years of operations, the Shipleys would still need to borrow money to finance the two new restaurants. Susan and Clark knew that they would be expected to present a set of recent financial statements as part of any loan proposal. So, the co-owners spent an afternoon compiling data regarding the key transactions of the two preceding years.

Background

In early 2015, Clark and Susan Shipley moved from the damp, gray environment of Seattle, Washington, to the dry, sunny climate of Phoenix, Arizona. After some reflection on their life in Seattle, as well as an analysis of the local business environment in the Phoenix area, they concluded that they would like to own and manage a restaurant. Glendale was Arizona’s third largest city, but it was not noted for a plethora of eating establishments, and those that did exist were principally Italian, Mexican, or fast food. The Shipleys concluded that their restaurant would feature Japanese rice bowls and operate under the name “Island Teriyaki.”

With that decision made, Clark and Susan began the long and difficult process of setting up their restaurant.

In March 2015, they formed Island Foods, Inc. by contributing \($10,000\) in cash in exchange for all of the company’s 1,000 shares of stock. Clark convinced his parents to loan the new venture \($120,000\) in cash, with principal payable at the rate of \($12,000\) per year over ten years and interest payable at a rate of 7.5 percent on the outstanding balance as of the beginning of the loan’s year. The loan agreement was signed on March 31, 2015, and provided that both principal and interest would be paid only once a year on March 31.

During March, the Shipleys searched for a suitable location for the restaurant. Clark negotiated a lease for approximately 2,000 square feet of retail space at a rate of \($1,400\) per month. The lease agreement ran for five years, with an option to renew for five more years. The landlord agreed to give the Shipleys three months of free rent on the front end of the lease in order to help the new business survive the critical start-up period.

Also during the month of March, Clark arranged to buy a commercial refrigerator, range, and grill for \($26,000\) in cash, to be delivered and installed on March 31. Discussions with the seller indicated that the kitchen equipment should last for five years. Clark and Susan also purchased a computer system, with restaurant-specific software already installed, at a cost of \($12,000\) cash. While the system could last indefinitely, Susan suggested that it be depreciated over six years. Other purchases included food preparation equipment at a cost of \($1,200\) cash and various restaurant furniture and fixtures at a cost of \($2,700\) in cash; the equipment, furniture, and fixtures were expected to have a useful life of three years.

To enable the restaurant to be fully operational on April 1, the landlord allowed the Shipleys’ carpenter, electrician, painters, and plumbers to begin renovations to the leased store on March 30 and 31. Working round-the-clock, the workers completed all necessary improvements and renovations to the leased space at a cost of \($68,000\) in cash.

The improvements and renovations would be depreciated over five years.

On March 31, the purchased kitchen equipment was delivered and “Island Teriyaki” opened for business as planned on April 1, 2015.

First Two Years of Operations

Although Susan and Clark had prepared a timely U.S. income tax return in April of 2016 (for 2015 income taxes), they had not bothered to prepare a full set of financial statements using the accrual method of accounting.

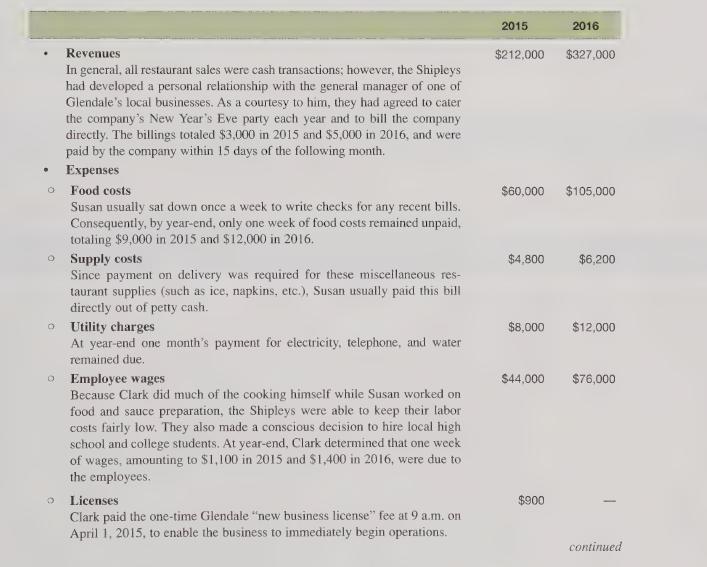

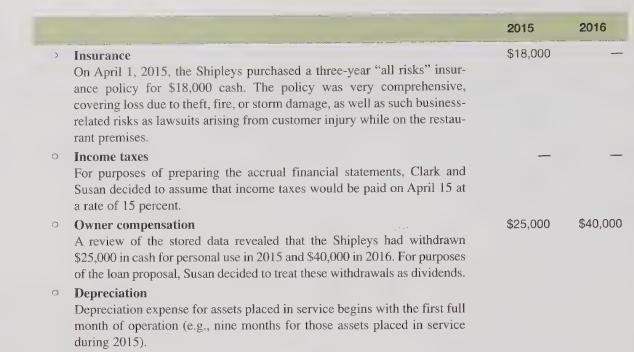

Since Clark had “backed up” the hard drive on their computer system on a weekly basis, he had a CD containing all of the 2015 and 2016 transactions. Working from the CD, Clark generated the necessary accounting information regarding the first two years of operations; he assembled the cash flow information in columnar form (see below) and relevant accrual information by each income statement account:

Required:

1. Prepare a balance sheet for Island Foods, Inc. as of March 31, 2015.

2. Prepare a balance sheet, income statement, and statement of cash flow as of December 31, 2015.

3. Prepare a balance sheet, income statement, and statement of cash flow as of December 31, 2016.

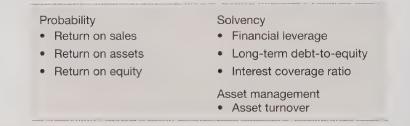

4. Calculate the following financial ratios for the restaurant for 2015 and 2016.

Step by Step Answer:

Financial Accounting For Executives And MBAs

ISBN: 9781618531988

4th Edition

Authors: Wallace, Simko, Ferris