Zoltar Moving Co. has been in operation for over 30 years providing moving services for local households

Question:

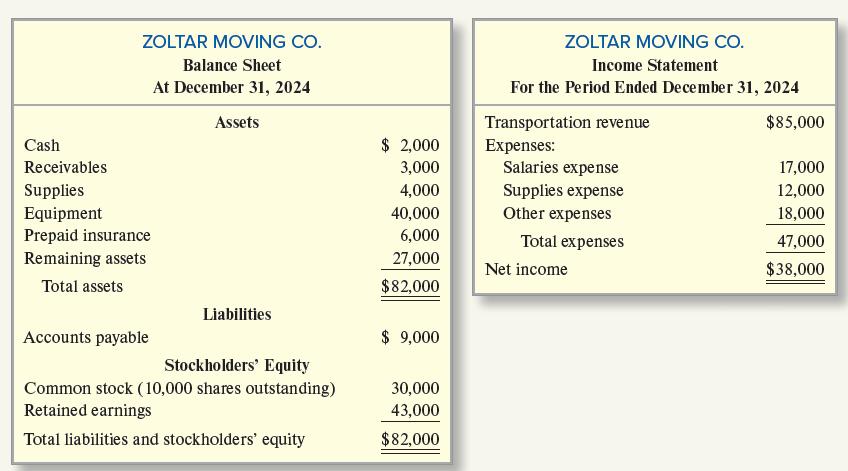

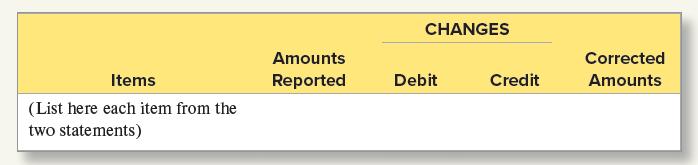

Zoltar Moving Co. has been in operation for over 30 years providing moving services for local households and businesses. It is now December 31, 2024, the end of the annual accounting period. Assume that the company has not done well financially during the year, although revenue has been fairly good. The two stockholders manage the company, but they have not given much attention to recordkeeping. In view of a serious cash shortage, they have applied to your bank for a $30,000 loan. You requested a complete set of financial statements. The following 2024 annual financial statements were prepared by a clerk and then were given to your bank.

After briefly reviewing the statements and “looking into the situation,” you requested that the statements be redone (with some expert help) to “incorporate depreciation, accruals, inventory counts, income taxes, and so on.” As a result of a review of the records and supporting documents, the following additional information was developed:

a. The Supplies of $4,000 shown on the balance sheet has not been adjusted for supplies used during 2024. A count of the supplies on hand on December 31, 2024, showed $1,800 worth of supplies remaining.

b. The insurance premium paid in 2024 was for years 2024 and 2025. The total insurance premium was debited in full to Prepaid Insurance when paid in 2024 and no adjustment has been made.

c. The equipment cost $40,000 when purchased January 1, 2024. It has an estimated annual depreciation of $8,000. No depreciation has been recorded for 2024.

d. Unpaid (and unrecorded) salaries at December 31, 2024, amounted to $3,200.

e. At December 31, 2024, transportation revenue collected in advance amounted to $7,000. This amount was credited in full to Transportation Revenue when the cash was collected earlier during 2024.

f. The income tax rate is 25 percent.

Required:

1. Record the six adjusting entries required on December 31, 2024, based on the preceding additional information.

2. Recast the preceding statements after taking into account the adjusting entries. You do not need to use classifications on the statements. Suggested form for the solution:

3. Omission of the adjusting entries caused:

a. Net income to be overstated or understated (select one) by $ .

b. Total assets on the balance sheet to be overstated or understated (select one) by $ .

c. Total liabilities on the balance sheet to be overstated or understated (select one) by $ .

4. For both the unadjusted and adjusted balances, calculate these ratios for the company: (a) earnings per share (rounded to two decimal places) and (b) total asset turnover (rounded to three decimal places), assuming the correct amount of total assets at the beginning of the year was $46,400. There were 10,000 shares outstanding all year. Explain the causes of the differences and the impact of the changes on financial analysis.

5. Write a letter to the company explaining the results of the adjustments, your analysis, and your decision regarding the loan.

Step by Step Answer:

Req 1 Req 2 Req 3 Omission of the adjusting entries caused Net income to be overstated by 27050 Total assets to be overstated by 13200 Total liabilities to be understated by 13850 Req 4 aEarnings per ...View the full answer

Financial Accounting

ISBN: 9781264229734

11th Edition

Authors: Robert Libby, Patricia Libby, Frank Hodge