Two depository institutions have composite CAMELS ratings of 1 or 2 and are well capitalized. Thus, each

Question:

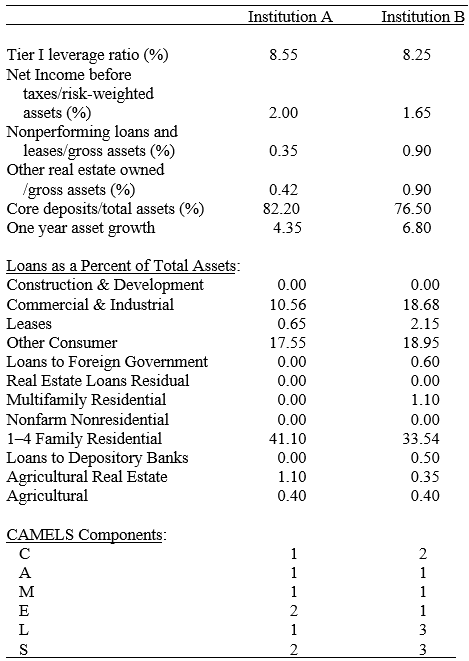

Two depository institutions have composite CAMELS ratings of 1 or 2 and are “well capitalized.” Thus, each institution falls into the FDIC Risk Category I deposit insurance assessment scheme. Institution A has average total assets of $750 million and average Tier I equity of $75 million. Institution B has average total assets of $1 billion and average Tier I equity of $110 million. Institution A has no unsecured debt or brokered deposits. Institution B has no unsecured debt and an asset growth rate over the last four years of 8 percent. Further, the institutions have the following financial ratios and CAMELS ratings:

The DIF reserve ratio is currently 1.30 percent. Calculate the deposit insurance assessment and the dollar value of the deposit insurance premium for each institution.

Financial RatiosThe term is enough to curl one's hair, conjuring up those complex problems we encountered in high school math that left many of us babbling and frustrated. But when it comes to investing, that need not be the case. In fact, there are ratios that,...

Step by Step Answer:

To determine the deposit insurance assessment for each in...View the full answer

Financial Institutions Management A Risk Management Approach

ISBN: 978-1259717772

9th edition

Authors: Anthony Saunders, Marcia Millon Cornett