Marston Marble Corporation is considering a merger with the Conroy Concrete Company. Conroy is a publicly traded

Question:

Marston Marble Corporation is considering a merger with the Conroy Concrete Company. Conroy is a publicly traded company, and its beta is 1.30.

Conroy has been barely profitable, so it has paid an average of only 20% in taxes during the last several years. In addition, it uses little debt; its target ratio is just 25%, with the cost of debt 9%.

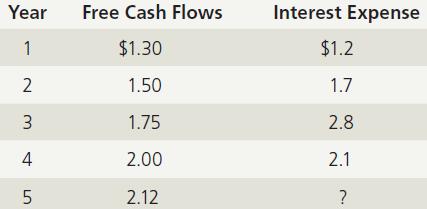

If the acquisition were made, Marston would operate Conroy as a separate, wholly owned subsidiary. Marston would pay taxes on a consolidated basis, and the tax rate would therefore increase to 35%. Marston also would increase the debt capitalization in the Conroy subsidiary to wd 5 40%, for a total of $22.27 million in debt by the end of Year 4, and pay 9.5% on the debt. Marston’s acquisition department estimates that Conroy, if acquired, would generate the following free cash flows and interest expenses (in millions of dollars) in Years 1–5:

In Year 5, Conroy’s interest expense would be based on its beginning-ofyear (that is, the end-of-Year-4) debt, and in subsequent years both interest expense and free cash flows are projected to grow at a rate of 6%. These cash flows include all acquisition effects. Marston’s cost of equity is 10.5%, its beta is 1.0, and its cost of debt is 9.5%. The risk-free rate is 6%, and the market risk premium is 4.5%. Use the compressed APV model to answer the following questions.

a. What is the value of Conroy’s unlevered operations, and what is the value of Conroy’s tax shields under the proposed merger and financing arrangements?

b. What is the dollar value of Conroy’s operations? If Conroy has $10 million in debt outstanding, how much would Marston be willing to pay for Conroy?

Problems 26-1

Hasting Corporation is interested in acquiring Vandell Corporation. Vandell has 1 million shares outstanding and a target capital structure consisting of 30% debt; its beta is 1.4 (given its target capital structure). Vandell has $10.82 million in debt that trades at par and pays an 8% interest rate. Vandell’s free cash flow (FCF0) is $2 million per year and is expected to grow at a constant rate of 5% a year. Vandell pays a 40% combined federal and state tax rate. The risk-free rate of interest is 5%, and the market risk premium is 6%. Hasting’s first step is to estimate the current intrinsic value of Vandell.

Problems 26-2

Hasting Corporation estimates that if it acquires Vandell Corporation, synergies will cause Vanell’s free cash flows to be $2.5 million, $2.9 million, $3.4 million, and $3.57 million at Years 1 through 4, respectively, after which the free cash flows will grow at a constant 5% rate. Hasting plans to assume Vandell’s $10.82 million in debt (which has an 8% interest rate) and raise additional debt financing at the time of the acquisition. Hasting estimates that interest payments will be $1.5 million each year for Years 1, 2, and 3.

After Year 3, a target capital structure of 30% debt will be maintained. Interest at Year 4 will be $1.472 million, after which the interest and the tax shield will grow at 5%. As described in Problem 26-1, Vandell currently has 1 million shares outstanding and a target capital structure consisting of 30% debt; its current beta is 1.4 (i.e., based on its target capital structure).

Step by Step Answer:

Intermediate Financial Management

ISBN: 9781337395083

13th Edition

Authors: Eugene F. Brigham, Phillip R. Daves