Question: Consider a random variable with a multivariate normal distribution, ~N(, ). The expected values and covariances of the discrete ap- proximation should match those of

Consider a random variable with a multivariate normal distribution,

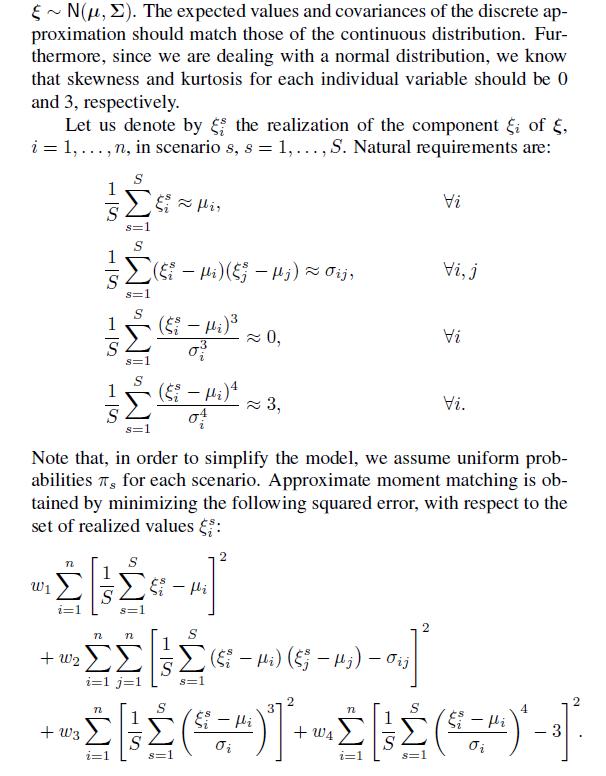

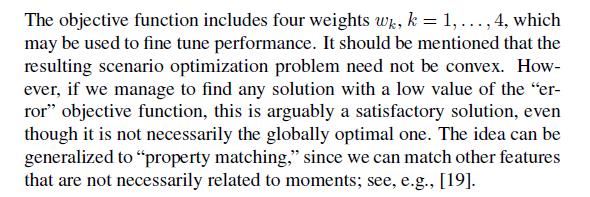

~N(, ). The expected values and covariances of the discrete ap- proximation should match those of the continuous distribution. Fur- thermore, since we are dealing with a normal distribution, we know that skewness and kurtosis for each individual variable should be 0 and 3, respectively. Let us denote by the realization of the component ; of, i = 1,..., n, in scenario s, s = 1,..., S. Natural requirements are: 51 11 51 51 S ~Hi ) ( - ;) ~ j, IM SIM SIM IM (Ei - Hi) 0, ( - Hi)4 3, Vi Vi, j Vi Vi. Note that, in order to simplify the model, we assume uniform prob- abilities T, for each scenario. Approximate moment matching is ob- tained by minimizing the following squared error, with respect to the set of realized values : [-313- n n +302 i=1 j=1 1 S S (i) (H) - ij s=1 {()}{} }+ [()}{3+

Step by Step Solution

3.41 Rating (148 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts