Question: Let us consider how we may represent a semicontinuous variable within an LP framework. As we have mentioned, a common requirement on the level of

Let us consider how we may represent a semicontinuous variable within an LP framework. As we have mentioned, a common requirement on the level of an activity is that, if it is undertaken, its level should be in the interval [m,M]. Note that this is not equivalent to requiring that![]() . Rather, we want something like

. Rather, we want something like ![]()

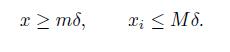

which is a non-convex set (recall that the union of convex sets need not be convex). Using the same big-M trick as above, we may introduce a binary variable ![]() and write

and write

Semicontinuous variables may be used when the amount of an asset in a portfolio must be above a minimum threshold, if the asset is included in the portfolio.

mxM

Step by Step Solution

3.42 Rating (158 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts