The current price of a stock share that pays no dividend is ( 50). The price follows

Question:

The current price of a stock share that pays no dividend is \(€ 50\). The price follows a GBM with drift \(12 \%\) and volatility \(35 \%\); the continuously compounded risk-free rate is \(5 \%\). Consider a call and a put options, both European-style, with strike \(€ 55\), maturing in nine months. Which option is more likely to be exercised?

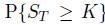

The probability of exercising the call is ), which is given by

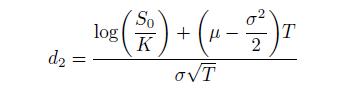

), which is given by  , provided that we use the true drift. Hence, we should compute

, provided that we use the true drift. Hence, we should compute  as

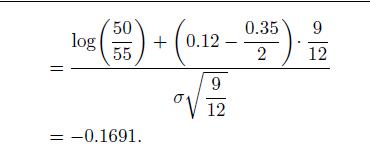

as

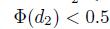

Since , there is no need for further calculations, as this implies

, there is no need for further calculations, as this implies  . Hence, the put is more likely to be exercised.

. Hence, the put is more likely to be exercised.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Pranav Makode

I am a bachelor students studying at professor ram meghe institute of technology and research. I have a great experience of being an expert. I have worked as an expert at helloexperts and solvelancer as a part time job. I have also worked as a doubt solver at ICAD SCHOOL OF LEARNING, which is in Amravati city. I have also worked as an Freelancer.

I have great experience of helping students, as described above. I can help any students in a most simple and understandable way. I will not give you have any chance for complaint. You will be greatfull to accept me as an expert.

1+ Reviews

10+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: