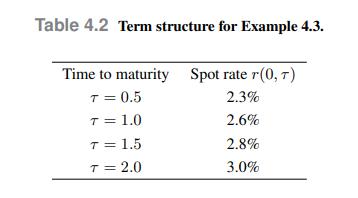

The current term structure of (continuously compounded) interest rates is given in Table 4.2. We want to

Question:

The current term structure of (continuously compounded) interest rates is given in Table 4.2. We want to find the swap rate for a contract maturing in two years with semiannual payments.

To find the swap rate, let us assume a nominal value of 1 (which is actually irrelevant) and solve the equation

which yields

Clearly, we may just apply Eq. (4.11) and find the same result. The swap rate \(K_{2}\) with semiannual compounding corresponds to \(K=\) 0.0299 with continuous compounding.

Data From Equation (4.11)

Data From Table 4.2

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Rohail Amjad

Experienced Finance Guru have a full grip on various sectors, i.e Media, Insurance, Automobile, Rice and other Financial Services.

Have also served in Business Development Department as a Data Anlayst

32+ Reviews

83+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: