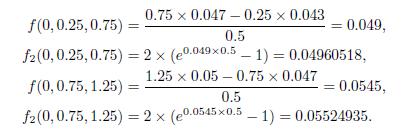

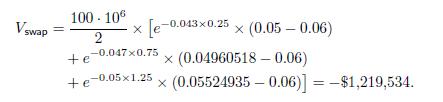

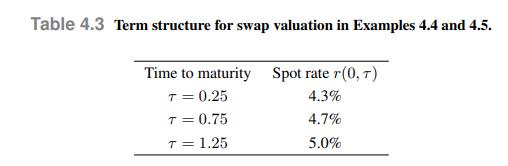

We use the data in Table 4.3 once more, but now we need the forward rates for

Question:

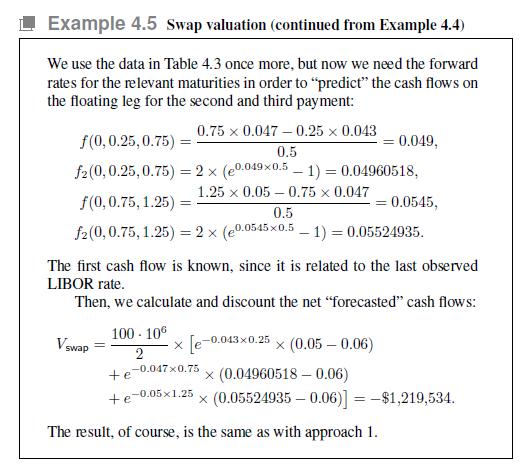

We use the data in Table 4.3 once more, but now we need the forward rates for the relevant maturities in order to "predict" the cash flows on the floating leg for the second and third payment:

The first cash flow is known, since it is related to the last observed LIBOR rate.

Then, we calculate and discount the net "forecasted" cash flows:

The result, of course, is the same as with approach 1 .

Data From Table 4.3

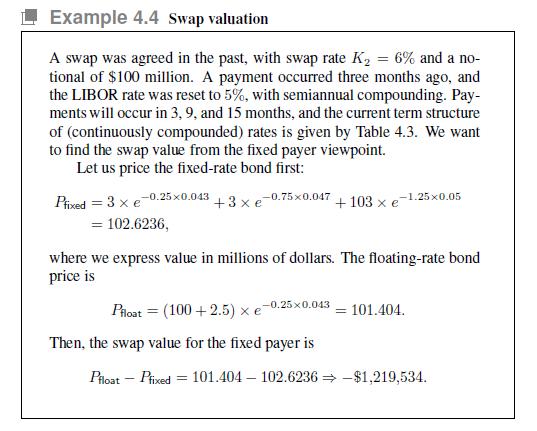

Data From Example 4.4

Data From Example 4.5

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

GERALD KAMAU

non-plagiarism work, timely work and A++ work

6+ Reviews

11+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: