Question: Heres a simplified version of exercise 10. Consider an alternative parameterization of the binomial: Construct binomial European call and put option pricing functions in VBA

Here’s a simplified version of exercise 10.

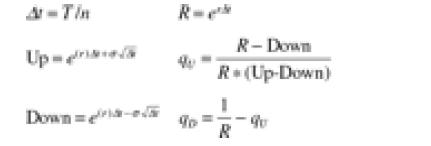

Consider an alternative parameterization of the binomial:

Construct binomial European call and put option pricing functions in VBA for this parameterization and show that they also converge to the Black-Scholes formula. (The message here is that the parameterization of the binomial Up and Down is not unique.)

Up -Tin R- R-Down R(Up-Down) Down=- To R

Step by Step Solution

★★★★★

3.45 Rating (142 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock