A fixed-income manager is presented with the following key rate duration summary of his actively managed bond

Question:

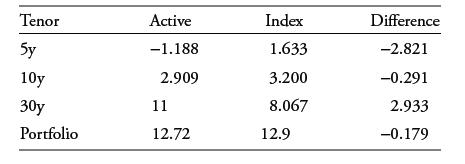

A fixed-income manager is presented with the following key rate duration summary of his actively managed bond portfolio versus an equally weighted index portfolio across 5-, 10-, and 30-year maturities:

Assume the active manager has invested in the index bond portfolio and used only derivatives to create the active portfolio. Which of the following most likely represents the manager’s synthetic positions?

a. Receive-fixed 5-year swap, short 10-year futures, and pay-fixed 30-year swap

b. Pay-fixed 5-year swap, short 10-year futures, and receive-fixed 30-year swap

c. Short 5-year futures, long 10-year futures, and receive-fixed 30-year swap

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

B is correct The key rate duration summary shows the investor to be net short 5 and 10year key ...View the full answer

Answered By

Gaurav Soni

Teaching was always an area where I can pursue my passion. I used to teach my friends and junior during my school and college life. After completing my professional qualification (chartered accountancy) and before joining my job, I also joined an organization for teaching and guidance to my juniors. I had also written some articles during my internship which later got published. apart from that, I have also given some presentations on certain amendments/complex issues in various forms.

Linkedin profile link:

https://www.linkedin.com/in/gaurav-soni-38067110a

7+ Reviews

13+ Question Solved

Related Book For

Question Posted: