An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:

Question:

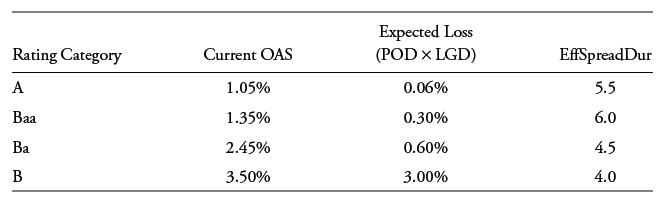

An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:

The investor anticipates an economic slowdown in the next year that will have a greater adverse impact on lower-rated issuers. Assume that an index portfolio is equally allocated across all four rating categories, while the investor chooses a tactical portfolio combining equal long positions in the investment-grade (A and Baa) bonds and short positions in the high-yield (Ba and B) bonds.

Calculate excess spread under an economic downturn scenario for the index and tactical portfolios where both OAS and expected loss rise 50% for investment grade bonds and double for high-yield bonds.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The following table summarizes expected excess returns E Exce...View the full answer

Answered By

Muhammad Umair

I have done job as Embedded System Engineer for just four months but after it i have decided to open my own lab and to work on projects that i can launch my own product in market. I work on different softwares like Proteus, Mikroc to program Embedded Systems. My basic work is on Embedded Systems. I have skills in Autocad, Proteus, C++, C programming and i love to share these skills to other to enhance my knowledge too.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: