Question: Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants

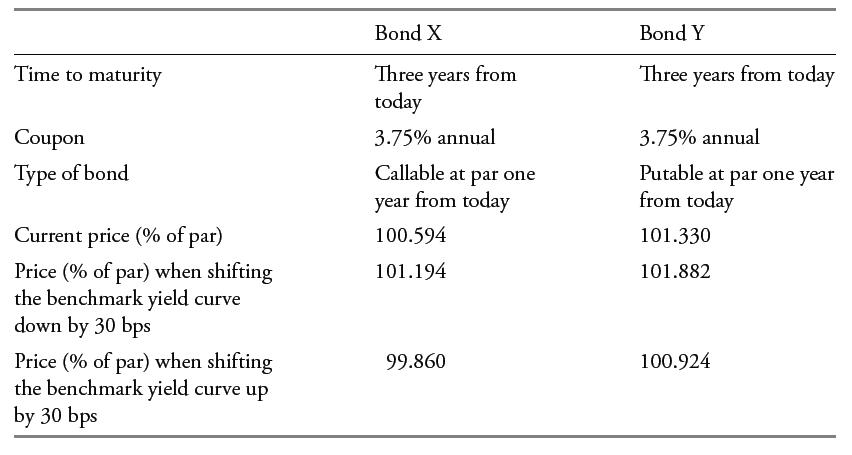

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her valuation software shows how the prices of these bonds change for 30 bps shifts up or down: The effective convexity of Bond X:

The effective convexity of Bond X:

A. Cannot be negative.

B. Turns negative when the embedded option is near the money.

C. Turns negative when the embedded option moves out of the money.

Time to maturity Coupon Type of bond Current price (% of par) Price (% of par) when shifting the benchmark yield curve down by 30 bps Price (% of par) when shifting the benchmark yield curve up by 30 bps Bond X Three years today 3.75% annual from Callable at par one year from today 100.594 101.194 99.860 Bond Y Three years from today 3.75% annual Putable at par one year from today 101.330 101.882 100.924

Step by Step Solution

3.28 Rating (163 Votes )

There are 3 Steps involved in it

B is correct The effective convexity of a callable bond turns negative w... View full answer

Get step-by-step solutions from verified subject matter experts