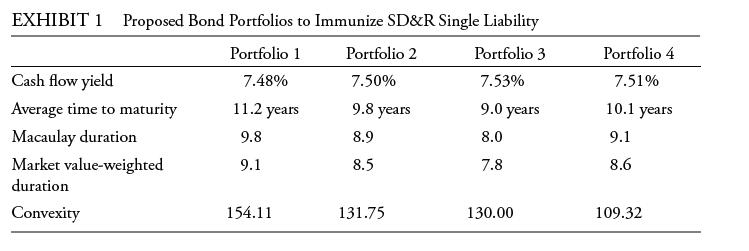

Which of the portfolios in Exhibit 1 best minimizes the structural risk to a single-liability immunization strategy?

Question:

Which of the portfolios in Exhibit 1 best minimizes the structural risk to a single-liability immunization strategy?

A. Portfolio 1

B. Portfolio 3

C. Portfolio 4

SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is meeting with a prospective client, Leah of DePuy Financial Company (DFC).

Leah informs Molly that DFC’s previous fixed-income manager focused on the interest rate sensitivities of assets and liabilities when making asset allocation decisions. Molly explains that, in contrast, SD&R’s investment process first analyzes the size and timing of client liabilities, and then it builds an asset portfolio based on the interest rate sensitivity of those liabilities.

Molly notes that SD&R generally uses actively managed portfolios designed to earn a return in excess of the benchmark portfolio. For clients interested in passive exposure to fixed-income instruments, SD&R offers two additional approaches.

• Approach 1: Seeks to fully replicate a small range of benchmarks consisting of government bonds.

• Approach 2: Follows an enhanced indexing process for a subset of the bonds included in the Bloomberg Barclays US Aggregate Bond Index. Approach 2 may also be customized to reflect client preferences.

To illustrate SD&R’s immunization approach for controlling portfolio interest rate risk, Molly discusses a hypothetical portfolio composed of two non-callable, investment-grade bonds. The portfolio has a weighted average yield-to-maturity of 9.55%, a weighted average coupon rate of 10.25%, and a cash flow yield of 9.85%.

Leah informs Molly that DFC has a single $500 million liability due in nine years, and she wants SD&R to construct a bond portfolio that earns a rate of return sufficient to pay off the obligation. Leah expresses concern about the risks associated with an immunization strategy for this obligation. In response, Molly makes the following statements about liability-driven investing:

• Statement 1: Although the amount and date of SD&R’s liability is known with certainty, measurement errors associated with key parameters relative to interest rate changes may adversely affect the bond portfolios.

• Statement 2: A cash flow matching strategy will mitigate the risk from non-parallel shifts in the yield curve.

Molly provides the four US dollar−denominated bond portfolios in Exhibit 1 for consideration. Molly explains that the portfolios consist of non-callable, investment-grade corporate and government bonds of various maturities because zero-coupon bonds are unavailable.

The discussion turns to benchmark selection. DFC’s previous fixed-income manager used a custom benchmark with the following characteristics:

• Characteristic 1: The benchmark portfolio invests only in investment-grade bonds of US corporations with a minimum issuance size of $250 million.

• Characteristic 2: Valuation occurs on a weekly basis, because many of the bonds in the index are valued weekly.

• Characteristic 3: Historical prices and portfolio turnover are available for review.

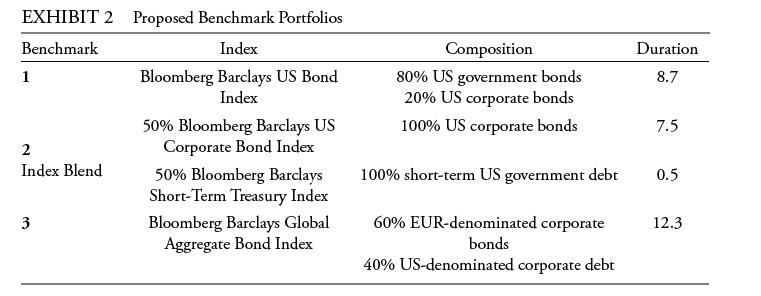

Molly explains that, in order to evaluate the asset allocation process, fixed-income portfolios should have an appropriate benchmark. Leah asks for benchmark advice regarding DFC’s portfolio of short-term and intermediate-term bonds, all denominated in US dollars. Molly presents three possible benchmarks in Exhibit 2.

Step by Step Answer: