Youve just taken a job at the central bank and are given the job of calculating the

Question:

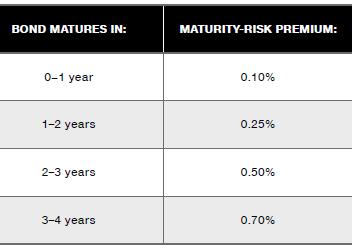

You’ve just taken a job at the central bank and are given the job of calculating the appropriate nominal interest rate for a number of different Treasury bonds with different maturity dates. You have been told to use the real riskfree interest rate of 3.5 percent, and this is expected to continue on into the future without any change. Inflation is expected to be constant over the future at a rate of 2.5 percent. Since the Treasury bonds are issued by the government, they do not have any default risk or any liquidity risk (that is, there is no liquidity risk premium). The maturity-risk premiums, dependent upon how many years the bond has to maturity, are as follows:

Given this information, what should the nominal rate of interest on Treasury bonds maturing in 0–1 year, 1–2 years, 2–3 years, and 3–4 years be?

Step by Step Answer:

Foundations Of Finance

ISBN: 9781292318738

10th Global Edition

Authors: Arthur Keown, John Martin, J. Petty