Near the end of 2019, the management of Isle Corp., a merchandising company, prepared the following estimated

Question:

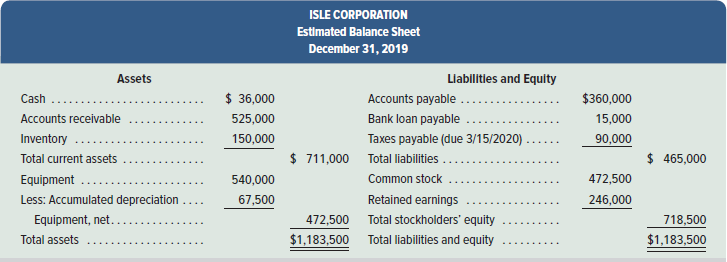

Near the end of 2019, the management of Isle Corp., a merchandising company, prepared the following estimated balance sheet for December 31, 2019.

To prepare a master budget for January, February, and March of 2020, management gathers the following information.

a. The company’s single product is purchased for $30 per unit and resold for $45 per unit. The expected inventory level of 5,000 units on December 31, 2019, is more than management’s desired level for 2020, which is 25% of the next month’s expected sales (in units). Expected sales are January, 6,000 units; February, 8,000 units; March, 10,000 units; and April, 9,000 units.

b. Cash sales and credit sales represent 25% and 75%, respectively, of total sales. Of the credit sales, 60% is collected in the first month after the month of sale and 40% in the second month after the month of sale. For the $525,000 accounts receivable balance at December 31, 2019, $315,000 is collected in January 2020 and the remaining $210,000 is collected in February 2020.

c. Merchandise purchases are paid for as follows: 20% in the first month after the month of purchase and 80% in the second month after the month of purchase. For the $360,000 accounts payable balance at December 31, 2019, $72,000 is paid in January 2020 and the remaining $288,000 is paid in February 2020.

d. Sales commissions equal to 20% of sales dollars are paid each month. Sales salaries (excluding commissions) are$90,000 per year.

e. General and administrative salaries are $144,000 per year. Maintenance expense equals $3,000 per month and is paid in cash.

f. Equipment reported in the December 31, 2019, balance sheet was purchased in January 2019. It is being depreciated over eight years under the straight-line method with no salvage value. The following amounts for new equipment purchases are planned in the coming quarter: January, $72,000; February, $96,000; and March, $28,800. This equipment will be depreciated using the straight-line method over eight years with no salvage value. A full month’s depreciation is taken for the month in which equipment is purchased.

g. The company plans to buy land at the end of March at a cost of $150,000, which will be paid with cash on the last day of the month.

h. The company has a contract with its bank to obtain additional loans as needed. The interest rate is 12% per year, and interest is paid at each month-end based on the beginning balance. Partial or full payments on these loans are made on the last day of the month. The company has agreed to maintain a minimum ending cash balance of $36,000 at the end of each month.

i. The income tax rate for the company is 40%. Income taxes on the first quarter’s income will not be paid until April 15.

Required

Prepare a master budget for each of the first three months of 2020; include the following component budgets (show supporting calculations as needed, and round amounts to the nearest dollar).

1. Monthly sales budgets (showing both budgeted unit sales and dollar sales).

2. Monthly merchandise purchases budgets.

3. Monthly selling expense budgets.

4. Monthly general and administrative expense budgets.

5. Monthly capital expenditures budgets.

6. Monthly cash budgets.

7. Budgeted income statement for the entire first quarter (not for each month).

8. Budgeted balance sheet as of March 31, 2020.

Salvage ValueSalvage value is the estimated book value of an asset after depreciation is complete, based on what a company expects to receive in exchange for the asset at the end of its useful life. As such, an asset’s estimated salvage value is an important...

Step by Step Answer:

Part 1 ISLE CORPORATION Sales Budgets January February and March 2020 Budgeted Units Budgeted Unit Price Budgeted Total Dollars January 2020 6000 45 270000 February 2020 8000 45 360000 March 2020 1000...View the full answer