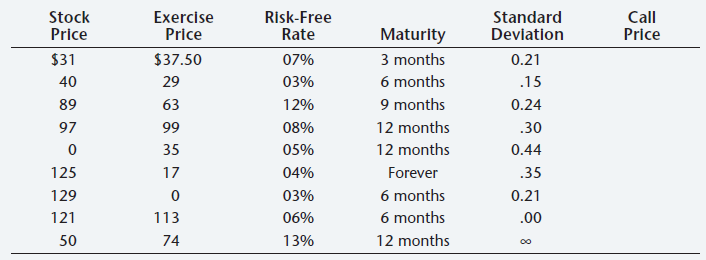

Calculate the BlackScholes option price in each of the cases that follow. The risk-free rate and standard

Question:

Calculate the Black–Scholes option price in each of the cases that follow. The risk-free rate and standard deviation are quoted in annual terms. The last three cases may require some thought.

Round computed values for d1 and d2 to the nearest values in Table 25A.1 for determining N(d1) and N(d2), respectively.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Accurate values for the standard normal distribution are used here based on Excels NO...View the full answer

Answered By

Collins Omondi

I have been an academic and content writer for at least 6 years, working on different academic fields including accounting, political science, technology, law, and nursing in addition to those earlier listed under my education background.

I have a Bachelor’s degree in Commerce (Accounting option), and vast knowledge in various academic fields Finance, Economics, Marketing, Management, Social Science, Women and Gender, Business law, and Statistics among others.

4+ Reviews

16+ Question Solved

Related Book For

Fundamentals of Corporate Finance

ISBN: 978-0071051606

8th Canadian Edition

Authors: Stephen A. Ross, Randolph W. Westerfield

Question Posted: