Rogers Communications Inc. is a diversified Canadian communications and media company engaged in three primary lines of

Question:

Rogers Communications Inc. is a diversified Canadian communications and media company engaged in three primary lines of business: Wireless, Cable, and Media. The following is part of Rogers’ revenue recognition policy note in its 2019 financial statements:

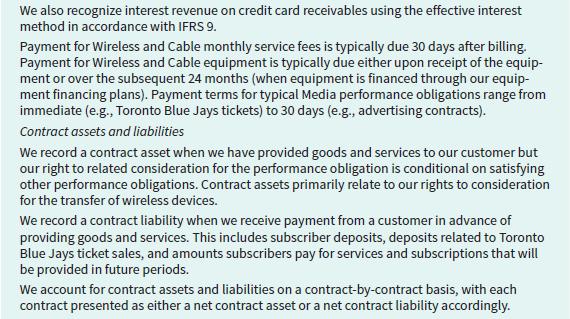

Rogers’ balance sheet included a current liability of $224 million at December 31, 2019, called Contract Liabilities. Contract liabilities represent payment in advance of services and include subscriber deposits, deposits related to Toronto Blue Jays ticket sales, and amounts received from subscribers related to services and subscriptions to be provided in future periods.

Instructions

a. When does Rogers recognize its revenue from installation services for Cable subscribers?

b. When should Rogers record unearned revenue from its subscription services? When should it record unearned revenue for its Blue Jays home game admission revenue?

c. If Rogers (inappropriately) recorded these unearned revenues as revenue when the cash was received in advance, what would be the effect on the company’s financial position? (Use the basic accounting equation and explain what elements would be overstated or understated.)

Step by Step Answer:

a Revenue from installation services for Cable subscr...View the full answer

Accounting Principles Volume 1

ISBN: 9781119786818

9th Canadian Edition

Authors: Jerry J. Weygandt, Donald E. Kieso, Paul D. Kimmel, Barbara Trenholm, Valerie Warren, Lori Novak