NovaCor Limited had the following shareholders' equity on 31 December 20X8: Earnings for (20 mathrm{X} 8) had

Question:

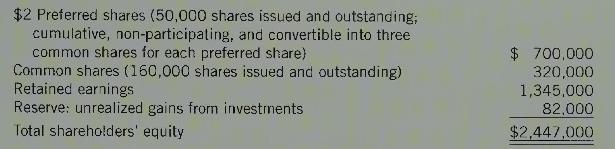

NovaCor Limited had the following shareholders' equity on 31 December 20X8:

Earnings for \(20 \mathrm{X} 8\) had been \(\$ 307,000\) and comprehensive income, which also included a \(\$ 12,000\) unrealized gain on an investment, was \(\$ 319,000\). Basic earnings per share was calculated as \(\$ 1.29\) :

During \(20 \times 8\), the company paid the \(\$ 2\) per share preferred dividends and also paid \(\$ 1.00\) per share dividend to common shareholders. Dividends are reported in total and per share in the financial statements.

On 1 April 20X9, NovaCor executed a 4-for-1 split of its common shares. On 15 July \(20 \mathrm{X} 9\), the company repurchased 22,000 common shares from one of the company's founders at \(\$ 12.00\) per share.

Required:

1. Prepare the journal entry to record the \(20 \mathrm{X} 9\) share repurchase.

2. Post-split, how many common shares would the holder of 5,000 preferred shares receive on conversion?

3. When the company prepares its comparative financial statements for \(20 \mathrm{X} 9\), what amount will be reported for \(20 \mathrm{X} 8\) earnings per share? What amount would be reported for \(20 \mathrm{X} 8\) cash dividends per common share?

4. Explain any other ways, in addition to the recalculation of earnings per share, that the 20X8 comparative amounts and disclosures would be changed, when presented in the \(20 \mathrm{X} 9\) financial statements.

Step by Step Answer: