Rusty Spears, CEO of Rustys Renovations, a custom building and repair company, is preparing documentation for a

Question:

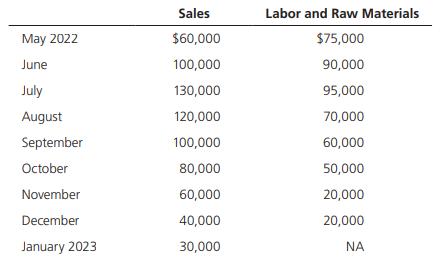

Rusty Spears, CEO of Rusty’s Renovations, a custom building and repair company, is preparing documentation for a line of credit request from his commercial banker. Among the required documents is a detailed sales forecast for parts of 2022 and 2023:

Estimates obtained from the credit and collection department are as follows: collections within the month of sale, 15%; collections during the month following the sale, 65%; collections the second month following the sale, 20%. Payments for labor and raw materials are typically made during the month following the one in which these costs were incurred. Total costs for labor and raw materials are estimated for each month as shown in the table. General and administrative salaries will amount to approximately $15,000 a month; lease payments under long-term lease contracts will be $5,000 a month; depreciation charges will be $7,500 a month; miscellaneous expenses will be $2,000 a month; income tax payments of $25,000 will be due in both September and December; and a progress payment of $80,000 on a new office suite must be paid in October. Cash on hand on July 1 will amount to $60,000, and a minimum cash balance of $40,000 will be maintained throughout the cash budget period.

a. Prepare a monthly cash budget for the last 6 months of 2022.

b. Prepare an estimate of the required financing (or excess funds)—that is, the amount of money Rusty’s Renovations will need to borrow (or will have available to invest)—for each month during that period.

c. Assume that receipts from sales come in uniformly during the month (i.e., cash receipts come in at the rate of 1/30 each day) but that all outflows are paid on the 5th of the month. Will this have an effect on the cash budget—in other words, would the cash budget you have prepared be valid under these assumptions? If not, what can be done to make a valid estimate of peak financing requirements? No calculations are required, although calculations can be used to illustrate the effects.

d. Rusty’s Renovations produces on a seasonal basis, just ahead of sales. Without making any calculations, discuss how the company’s current ratio and debt ratio would vary during the year assuming all financial requirements were met by short-term bank loans. Could changes in these ratios affect the firm’s ability to obtain bank credit? Why or why not?

e. If its customers began to pay late, this would slow down collections and thus increase the required loan amount. Also, if sales dropped off, this would have an effect on the required loan amount. Perform a sensitivity analysis that shows the effects of these two factors on the maximum loan requirement.

Step by Step Answer:

a Monthly Cash Budget for the Last 6 Months of 2022 Month July August September October November December Receipts 19500 87750 12000 80000 12000 8000 Disbursements Labor and Raw Materials 70000 50000 ...View the full answer

Intermediate Financial Management

ISBN: 9780357516669

14th Edition

Authors: Eugene F Brigham, Phillip R Daves