Question: Start with the partial model in the file Ch02 P15 Build a Model.xlsx on the textbooks Web site. The file contains data for this problem.

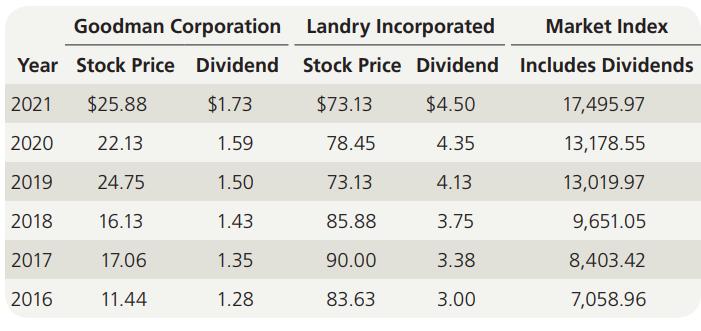

Start with the partial model in the file Ch02 P15 Build a Model.xlsx on the textbook’s Web site. The file contains data for this problem. Goodman Corporation’s and Landry Incorporated’s stock prices and dividends, along with the Market Index, are shown here. Stock prices are reported for December 31 of each year, and dividends reflect those paid during the year. The market data are adjusted to include dividends.

a. Use the data given to calculate annual returns for Goodman, Landry, and the Market Index, and then calculate average annual returns for the two stocks and the index. Remember, returns are calculated by subtracting the beginning price from the ending price to get the capital gain or loss, adding the dividend to the capital gain or loss, and then dividing the result by the beginning price. Assume that dividends are already included in the index. Also, you cannot calculate the rate of return for 2016 because you do not have 2015 data.

b. Calculate the standard deviations of the returns for Goodman, Landry, and the Market Index. (Hint: Use the sample standard deviation formula given in the chapter, which corresponds to the STDEV function in Excel.)

c. Construct a scatter diagram graph that shows Goodman’s returns on the vertical axis and the Market Index’s returns on the horizontal axis. Construct a similar graph showing Landry’s stock returns on the vertical axis.

d. Estimate Goodman’s and Landry’s betas as the slopes of regression lines with stock return on the vertical axis (y-axis) and market return on the horizontal axis (x-axis). Use Excel’s SLOPE function. Are these betas consistent with your graph?

e. The risk-free rate on long-term Treasury bonds is 6.04%. Assume that the market risk premium is 5%. What is the required return on the market? Now use the SML equation to calculate the two companies’ required returns.

f. If you formed a portfolio that consisted of 50% Goodman stock and 50% Landry stock, what would be its beta and its required return?

g. Suppose an investor wants to include some Goodman Industries stock in his portfolio. Stocks A, B, and C are currently in the portfolio, and their betas are 0.769, 0.985, and 1.423, respectively. Calculate the new portfolio’s required return if it consists of 25% Goodman, 15% Stock A, 40% Stock B, and 20% Stock C.

Goodman Corporation Landry Incorporated Year Stock Price Dividend Stock Price Dividend 2021 $25.88 $1.73 $73.13 $4.50 2020 22.13 1.59 78.45 4.35 2019 24.75 1.50 73.13 4.13 2018 16.13 1.43 85.88 3.75 2017 17.06 1.35 90.00 3.38 2016 11.44 1.28 83.63 3.00 Market Index Includes Dividends 17,495.97 13,178.55 13,019.97 9,651.05 8,403.42 7,058.96

Step by Step Solution

3.47 Rating (183 Votes )

There are 3 Steps involved in it

a To calculate the annual returns for Goodman Landry and the Market Index we use the formula Annual Return ... View full answer

Get step-by-step solutions from verified subject matter experts