New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

principles of external auditing

Auditing Concepts For A Changing Environment 5th Edition Larry E. Rittenberg, Bradley J. Schwieger - Solutions

Which of the following is true of capitalized leases as compared to operating leases?a. Only rent expense is reflected in the income statement.b. The leased asset does not appear on the balance sheet.c. Liabilities include the lease obligation.d. Future minimum lease obligations are not required to

An audit client will often use a specialist to assist in the valuation of selected as- sets and liabilities. Which of the following is an accurate description of the audi- tor's responsibilities for evaluating the work of a specialist? a. The auditor must gather evidence that pertains to both the

In accounting for an acquisition, the auditor must determine that there are sepa- rate valuations for all of the following except: a. All the specifically identifiable intangible assets, including an estimate of re- maining useful life. b. Goodwill associated with the reporting unit. c. Warranty

In determining the potential impairment of goodwill, which of the following would not be an appropriate methodology to estimate the fair value of a report- ing entity? Assume the reporting entity is not the company as a whole.a. Determine the fair market value of the entity based on current stock

If a company overpays for the purchase of another company, as took place when the merger of AOL and Time-Warner took place, what steps should the auditor take to be sure the results are fairly portrayed in the financial statements?a. Review financial analysts' reports; write the excess payment off

Which of the following is not considered a related entity transaction for account- ing purposes? A transaction between:a. A company and a separate entity controlled by the sister-in-law of the com- pany's president.b. A parent company and a subsidiary company. C. A company and its major customer

Which of the following statements is correct regarding transactions between a company and a major customer that accounts for more than 10 percent of the company's sales? a. The profit from such transactions should be shown as a separate line item on the financial statements. b. There is no

Which of the following is not a procedure that an auditor would use in perform- ing an audit designed to identify and account for related entity transactions?a. Send confirmations to all customers inquiring whether they are related par- ties.b. Obtain a list of all related parties from the

An auditor accepted an engagement to audit the 2006 financial statements of EFG Corporation and began the fieldwork on September 30, 2006. EFG gave the auditor the 2006 financial statements on January 17, 2007. The auditor completed the fieldwork on February 10, 2004, and delivered the report on

Identify the alternative methods an auditor can use to test the effectiveness of controls.

An auditor should gain an understanding of: a. Internal controls related to revenue recognition. b. Computer applications for recording sales. c. Key revenue related documents. d. All of the above

To test the completeness of sales, the auditor would select a sample of transactions from the population represented by the:a. Customer order file. b. Open invoice file. c. Bill of lading file. d. Sales invoice file.

A customer confirmed its balance by fax. Which of the following would not reduce the risk associated with the response?a. Consider the fax response to be an exception.b. Examine subsequent collections of the account.c. Request the customer to mail the original confirmation to the auditor.d.

The auditor's analytical procedures are facilitated if the client:a. Uses a standard cost system that produces variance reports.b. Segregates obsolete inventory before the physical inventory count.c. Corrects reportable conditions in internal control before the beginning of the audit.d. Reduces

One of the firm's largest clients, Ropper Company, makes gas grills, gas stoves, and gas dryers. Its financial position has deteriorated, but its management is confident that the worst has passed. Management points to new home starts associated with the current drop in interest rates and notes that

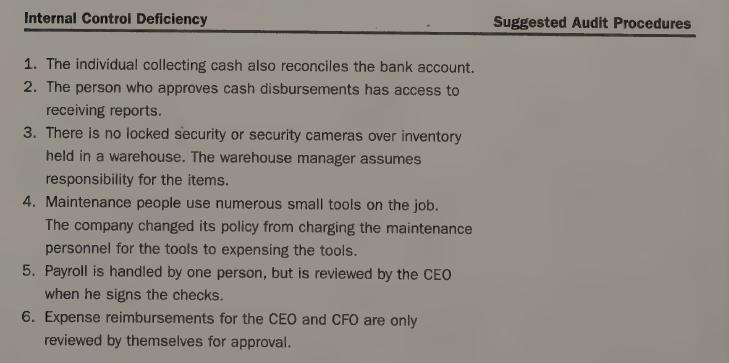

The auditor should consider known control deficiencies as part of the process of planning the audit.Requireda. A list of internal control deficiencies that were found at a small manufacturing business follows. For each deficiency listed, identify the fraud risk and identify the extended audit

Briefly define the following communication controls, and describe how they work:a. Encryptionb. Callbackc. Echo check

Why is ITF normally implemented by internal auditors rather than external au- ditors?

Assume that an internal audit department develops an integrated test facility (ITF) for use in performing continuous audits of the organization's mortgage pro- cessing system. The ITF has been in use for a few years. Assume the external au- ditor is satisfied with the competence and objectivity of

What kinds of system interdependencies are there in a vendor-managed inven- tory system like the one described in the text that exists between Wal-Mart and many of its larger vendors?

How can a tagging and tracing technique be used with an e-business client if the tagged transaction cannot be traced through the trading partners' computing sys- tem?

In an automated payroll system, all employees in the finishing department were paid at the rate of $7.45 per hour when the authorized rate was $7.15 per hour.Which of the following controls would have been most effective in preventing such an error? a. Access controls that would restrict access to

A deposit for Julie A. Smith at the local bank was inadvertently recorded as a de- posit in the account of June A. Smith. The control that would most likely have detected the error in depositing the amount to the wrong account would be:a. The use of self-checking digits on account numbers.b. Range

Which of the following independent errors would not be detected by batch con- trols? a. The computer operator added a fictitious employee to the processing of the weekly time cards. b. An employee who worked only 5 hours in the week was paid for 50 hours. c. The time card for one employee was

A mail-order retail organization sells complex electronic equipment through its catalogs. Orders are taken over phone lines and transmitted via terminal to the company's main warehouse for processing, shipping, and invoicing. Which of the following would be the most effective control procedure to

What factors determine the reliability of audit evidence? Give an example of two types of evidence, one that is more reliable and one that is less reliable.

What assertions are tested by confirmations sent to customers?

Which of the following is the least persuasive documentation in support of an auditor’sopinion?a. Schedules of details of physical inventory counts conducted by the clientb. Notation of inferences drawn from ratios and trendsc. Notation of appraisers’ conclusions in the auditor’s

An auditor determines that management integrity is high, the risk of account misstatements is low, and the client’s information system is reliable. Which of the following conclusions can be reached regarding the need to perform direct tests of account balances?a. Direct tests should be limited to

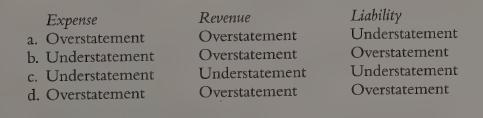

A test of an asset for overstatement provides corresponding evidence on: Expense a. Overstatement b. Understatement c. Understatement d. Overstatement Revenue Overstatement Overstatement Liability Understatement Overstatement Understatement Understatement Overstatement Overstatement

Observation is considered a reliable audit procedure but one that is limited in its usefulness. Which of the following does not represent a limitation of the use of observation as an audit technique?a. Individuals may act differently when being observed than they do otherwise.b. It is rarely

Confirmation is most likely to be a relevant form of evidence with regard to assertions about accounts receivable when the auditor has concern about the receivables’:a. Valuation.b. Classification.c. Existence.d. Completeness.

An auditor observes inventory held by the client and notes that some of the inventory appears to be old, but in good condition. Which of the following conclusions is justified by the audit procedure?I. The older inventory is obsolete.II. The inventory is owned by the company.III. Inventory needs to

Which of the following statements is not true concerning the auditor's documentation?a. The auditor should document the reasoning process and conclusions reached for significant account balances even if audit tests show no exceptions.b. Documentation review is facilitated if a standard

During the investigation of the Building and Land accounts, the auditor notes that one of the buildings was sold last year for a very large profit as authorized by the board of directors. The audit partner does not understand why the profit was so large.The partner instructs you to determine which

Which of the following statements regarding the incidence of fraud is incorrect?a. Fraud is estimated to cost U.S. businesses less than one cent on the dollar.b. Defalcations occur more often than financial reporting fraud.

Fraudulent financial reporting includes all of the following except: a. Misappropriation of assets for personal use. b. Manipulation, falsification, or alteration of accounting records or supporting documents. c. Misrepresentation or omission of events, transactions, or other significant in-

Which of the following statements is/are correct regarding the auditor’s use of materiality as it applies to a financial statement audit:a. The auditor is required to report all incidences of material fraud to the audit comunittee.b. The discovery of a material fraud indicates a company has a

An auditor discovers a material defalcation involving the theft of $500,000 of inventory. Restitution will not be made. Which of the following statements is not correct regarding the auditor’s responsibility for reporting the defalcation?a. Because theft was involved, the auditor must report it

Which of the following is not a correct statement regarding the use of brainstorming as part of a financial statement audit?a. It is required as a normal part of every engagement.b. It should include all members of the audit team.c. It should include an analysis of known internal control

The auditor notes the following changes in ratios:From just this information, the auditor should conclude all of the following about fraud risk except:a. Inventory has declined in quality because of the emphasis on increased sales.b. Accounts receivable growth may be caused by increased sales.c.

Which of the following would not be considered a motivation to commit fraud?a. Personal financial problemsb. Stock compensation programsc. Poor internal controlsd. Tight debt covenants

The accounting profession may have contributed to the downfall of Enron and the large public losses in all of the following ways except:a. Accounting became very rule-oriented and created a group of auditors that perceived value in finding the limits of the rules.b. Auditors were hired and fired by

The largest form of defalcation (both in dollars and frequency) is:a. Theft of cash directly from the company.b. Theft of cash through disbursement schemes.c. Theft of inventory and small tools.d. Theft of cash by taking customer receipts and writing off accounts receivable.

Green, CPA, has been engaged to audit the financial statements of Star Manufacturing, Inc., a medium-size entity that produces a wide variety of household goods. All acquisitions of materials are processed through the purchasing, receiving, accounts payable, and treasury functions.RequiredPrepare

(Internal Control Questionnaire-Purchases) Green, CPA, has been engaged to audit the financial statements of Star Manufacturing, Inc., a medium-size entity that produces a wide variety of household goods. All acquisitions of materials are processed through the purchasing, receiving, accounts

What is a control risk assessment? What is the importance of a control risk assess- ment in an audit engagement?

What are the requirements for the auditor to assess an entity's control environ- ment? Assume the auditor finds significant weaknesses in the entity's control en- vironment. Answer the following questions. What must be communicated to management and the audit committee? What must be communicated

The audit report described by the PCAOB is developed as part of an "integrated audit." Explain what is meant by the term "integrated audit."

What are the major elements of the auditor's report on management's assessment of internal control?

What kind of report should the auditor prepare if the auditor concludes that management's report on internal control omits significant deficiencies in either the design or operation of the entity's internal controls over financial reporting?

Does the auditor's report on internal control cover all internal controls or only those over financial reporting? Explain the difference.

Assume an auditor concludes that there are material deficiencies in an organiza- tion's internal controls over financial reporting. Management agrees and reports the weaknesses in its report to shareholders. The auditor concurs. How does this affect the nature of the auditor's report on internal

How should auditors use prior-year audit documentation in performing the con- trol risk assessment for the current year? What are the advantages and disadvan- tages of using prior-year documentation in performing this year's control risk as- sessment?

How does the auditor determine which controls need to be tested?

Describe a dual-purpose test. What is the purpose of such a test? Give an example of such a test.

What are the implications to the conduct of an audit and the auditor's assessment of internal control over financial reporting if the auditor concludes that an orga- nization's control environment does not promote strong control conscientious- ness on the part of employees? Give an example in your

The auditor concludes that a public company has significant deficiencies in its in- ternal controls over financial reporting. Which of the following is a proper re- sponse to this finding? a. Report the deficiencies to management and the audit committee. b. Report the deficiencies in the report

Which of the following would be considered a significant deficiency in an organization's control environment? a. The internal audit function is outsourced to a public accounting firm that is not performing the financial statement audit. b. Management has approximately 50 percent of its

An auditor finishes the audit of a company's financial statements and discovers a material misstatement that was due to recording revenue on a transaction to a regular customer twice. The client acknowledged the error and readily corrected the control deficiency before the financial statements were

Which of the following would not be considered an advantage of using an internal control questionnaire in understanding and documenting the controls in an important accounting application? Questionnaires can be: a. Computerized to provide linkages of weaknesses to particular types of errors that

Which of the following controls would be most effective in assisting the organi- zation in achieving the completeness objective? a. All employee time cards should be collected by the supervisor and transmitted directly to the payroll department for processing. b. All shipments must be approved by

Proper implementation of reconciliation controls would be effective in detecting all of the following errors except: a. Transactions were appropriately posted to individual subsidiary accounts, but because of a computer malfunction, some of the transactions were not posted to the master

Which of the following statements would not be correct regarding the authori- zation function as implemented in an organization? a. Blanket authorizations can be implemented in computer systems on the ap- proval of the user area. All changes to the authorization parameters embodied in the computer

Authorization of transactions in a computerized processing environment can take place in the form of: a. Computerized authorization in the form of user-approved blanket authoriza- tions. b. Electronic authorization of specific transactions carefully controlled by a pass- word system. c.

The accounts payable department receives the purchase order form to accomplish all of the following except. a. Compare invoice price to purchase order price. b. Ensure that the purchase had been properly authorized. c. Ensure that the party requesting the goods had received the goods. d.

Assume that you were given these five options to describe the tone at the top: Excellent Moderate Indifferent Nonexistent Machiavellian (do whatever it takes)Requireda. How would the auditor go about assessing which of the terms best describes the tone at the top?b. What effect would each

Brown Company provides the follow- ing office support services for more than 100 small clients: 1. Supplying temporary personnel 2. Providing monthly bookkeeping services 3. Designing and printing small brochures 4. Copying and reproduction services 5. Preparing tax reports Some clients pay

With your instructor's consent, identify a company and perform a background review of it to identify high-risk areas for an upcoming audit. Utilize all the electronic sources that have information available about the company. Obtain the latest financial results, either from the company's home page

Who is the audit client? Why is it important that the auditor understand who the true audit client is and why that party is the audit client?

Explain how "privileged communication" differs from confidential information.

Which of the following statements best explains why the CPA profession has found it essential to promulgate ethical standards and to establish means for en- suring their observance?a. Vigorous enforcement of an established code of ethics is the best way to pre- vent unscrupulous acts.b. Ethical

Which of the following is not a major threat to an auditor's independence?a. Audit partner's compensation based on obtaining and retaining clientsb. Becoming too friendly with the client's managementc. Significant time pressures to get the audit done quicklyd. Auditing records maintained by the

The Sarbanes-Oxley Act prohibits public accounting firms from providing cer- tain services to audit clients that are public companies. Which of the following services is not prohibited?a. Internal audit servicesb. Financial information systems design and implementation servicesc. Appraisal

According to the AICPA's ethical standards, an auditor would be considered in- dependent in which of the following instances?a. The auditor has an automobile loan from a client bank.b. The auditor is also an attorney who advises the client as its general counsel.c. An employee of the auditor

A violation of the profession's ethical standards would most likely have occurred when a CPA:a. Purchased a bookkeeping firm's practice of monthly write-ups for a percent- agc of fees received over a three-year period.b. Made arrangements with a bank to collect notes issued by a client in payment

A CPA is permitted to disclose confidential client information without the con- sent of the client to:I: Another CPA who has purchased the CPA's tax practice.II. Another CPA firm if the information concerns suspected tax return irregu- larities.III. A state CPA society's voluntary quality control

Manny Tallents is a CPA and a lawyer. In which of the following situations is Tal- lents violating the AICPA's Rules of Conduct?a. He uses his legal training to help determine the legality of an audit client's ac- tions.b. He researches a tax question to help the client make a management

CPA firms performing management consulting services can accept contingent fee contracts when:a. The amounts are not material in relationship to the audit billings.b. The consulting services are for clients for whom the auditor does not provide any form of attestation services related to a company's

Applying utilitarianism as a concept in addressing ethical situations requires the auditor to perform all of the following except:a. Identify the potential stakeholders that will be affected by the alternative out- comes.b. Determine the effect of the potential alternative courses of action on the

The following are situations in which auditors may find themselves.Situations: 1. Spencer is the partner in charge of the audit of Flip Company. He has half in- terest in a joint venture with Flip's CFO.2. Victoria is the senior in charge of the audit of Holder Company. During the past year, she

Following is a list of potential viola- tions of the AICPA's Code of Professional Conduct.Auditor Situations:1. T.O. Busy is unable to perform a service requested by a client. Therefore, Busy refers the client to Able, who pays Busy $200 for referring the business. Nei- ther Busy nor Able tells the

Two CPAs visiting at a recent meeting of the state CPA society were talking about accepting commissions and performing work on a contingent fee basis. The first one said he did not accept commissions for serv-ices provided to any client because it was unethical. The second one said she did accept

In analyzing the reported income of General Motors Corporation, Abraham Briloff reported that General Motors made only $22.8 million from the sale of cars:General Motors reported only $22.8 million as the amount earned from the corporation's production and sale of vehicles and related products. The

What are the eight elements of the COSO ERM model? Explain each component and its importance to effective enterprise risk management.

What are the major advantages to a company of implementing an effective enterprise risk management process?

How might an organization go about sharing or transferring risk?

Explain why it may be easier for the auditor to assess environment risk as opposed to separately assessing inherent risk and control risk.

4-32 Why is it important for the auditor to use risk analysis to develop expectations about client performance? 4-33 What background information might be useful to the auditor in planning the audit to assist in determining whether the client has potential inventory obsoles- cence or receivables

4-36 What ratios would best indicate problems with potential inventory obsolescence or collectibility of receivables? How are those ratios calculated?

Management integrity affects all of the following risks except: a. Enterprise risk. b. Financial reporting risk.c. Engagement risk. d. All of the above

A key element of the COSO ERM model is risk appetite. Risk appetite is a. Best determined by management with board of director review and concur- rence. b. An integral part of the risk culture. c. A necessary prerequisite to an ERM model. d. All of the above

4-41 An external auditor is interested in whether a company has implemented an ef- fective ERM because: a. It reduces the likelihood that an organization will fail. b. It provides a framework for the company to develop broad based controls. c. It provides a framework to reduce financial

Which of the following would not be a source of information about risk of a po- tential new audit client? a. The previous auditor b. Management c. The Internet d. The new auditor's permanent file

An engagement letter should be written before the start of an audit because: a. It may limit the auditor's legal liability by specifying the auditor's responsibili- ties. b. It specifies the client's responsibility for preparing schedules and making the records available to the auditor. c. It

If the auditor has concerns about the integrity of management, which of the following would not be an appropriate action? a. Refuse to accept the engagement because a client does not have an inalienable right to an audit. b. Expand audit procedures in areas where management representations are

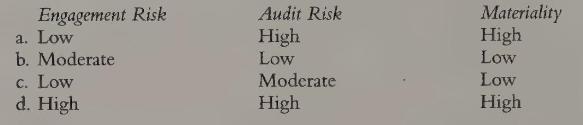

Which of the following combinations of engagement risk, audit risk, and mate- riality would lead to the most audit work? Engagement Risk a. Low b. Moderate c. Low d. High Audit Risk High Low Moderate High Materiality High Low Low High

Which of the following would not be considered a limitation of the audit risk model?a. The model treats each risk component as a separate and independent factor when some of the factors are related.b. Inherent risk is difficult, if not impossible, to formally assess.c. It is difficult, if not

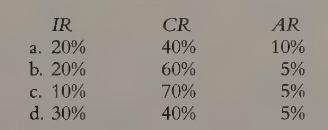

Which of the following models expresses the general relationship of risks associated with the auditor's evaluation of control risk (C R), inherent risk (I R), and audit risk (A R) that would lead the auditor to conclude that additional substantive tests of details of an account balance are not

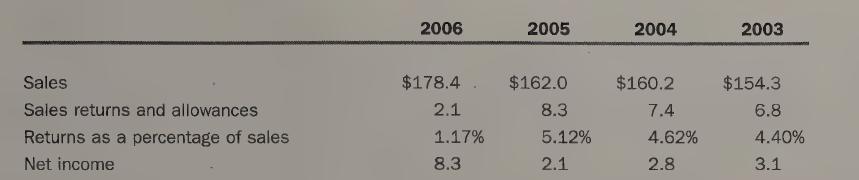

Comparing client data with industry data and with its own results for the previous year, the auditor finds that the number of days' sales in accounts receivable for this year is 66 for the client, 42 for the industry average, and 38 for the client's previous year. Inventory levels have remained the

Showing 600 - 700

of 795

1

2

3

4

5

6

7

8

Step by Step Answers