Mathew Philp, president of North Mining Ltd, has made budgets a major focus for managers. Making budget

Question:

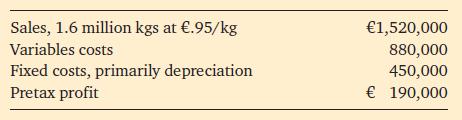

Mathew Philp, president of North Mining Ltd, has made budgets a major focus for managers. Making budget was such an important goal that the only two managers who had missed their budgets in 20X7 (by 2 per cent and 4 per cent, respectively) had been summarily fired. This caused all managers to be wary when setting their 20X8 budgets. The Red Mountain Copper Division of North Mining had the following results for 20X7:

Molly Stark, general manager of Red Mountain Copper, received a memo from Philp that contained the following: We expect your profit for 20X8 to be at least €209,000. Prepare a budget showing how you plan to accomplish this.

Stark was concerned because the market for copper had recently softened. Her market research staff forecast that sales would be at or below the 20X7 level and prices would likely be between €.92 and €.94 per kg. Her manufacturing manager reported that most of the fixed costs were committed and there were few efficiencies to be gained in the variable costs. He indicated that perhaps a 2 per cent savings in variable costs might be achievable but certainly no more.

1. Prepare a budget for Stark to submit to headquarters. What dilemmas does Stark face in preparing this budget?

2. What problems do you see in the budgeting process at North Mining?

3. Suppose Stark submitted a budget showing a €209,000 profit. It is now late in 20X8, and she has had a good year. Despite an industry-wide decline in sales, Red Mountain Copper’s sales matched last year’s 1.6 million kgs and the average price per kg was €.945, nearly at last year’s level and well above that forecast. Variable costs were cut by 2 per cent through extensive efforts. Still, profit projections were more than €9,000 below budget. Stark was concerned for her job, so she approached the accountant and requested that depreciation schedules be changed. By extending the lives of some equipment for 2 years, depreciation in 20X8 would be reduced by €15,000. Estimating the economic lives of equipment is difficult, and it would be hard to prove that the old lives were better than the new proposed lives. What should the accountant do? What ethical issues does this proposal raise?

Step by Step Answer:

Solutions and Analysis 1 Budget for Stark and Dilemmas Budget Sales16 million kgs same as 20X7 at 92...View the full answer

Introduction To Management Accounting

ISBN: 9780273737551

1st Edition

Authors: Alnoor Bhimani, Charles T. Horngren, Gary L. Sundem, William O. Stratton, Jeff Schatzberg