McCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include

Question:

McCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the-clock monitoring of patients are treated as overhead costs.

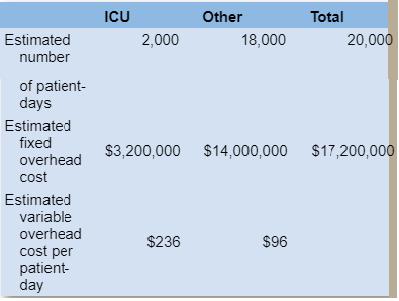

Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. For the most recent period, this predetermined rate was based on three estimates—fixed overhead costs of $17,200,000, variable overhead costs of $110 per patient-day, and a denominator volume of 20,000 patient-days.

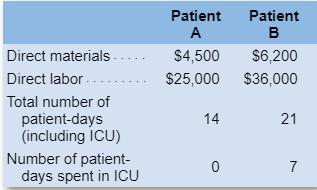

Recently a member of the hospital’s accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy of the costs allocated to patients. The first overhead rate would include all overhead costs within the Intensive Care Unit (ICU) and the second overhead rate would include all Other overhead costs. Information pertaining to these two cost pools and two of the hospital’s patients—Patient A and Patient B—is provided below:

Required:

1. Assuming McCullough continues to use only one predetermined overhead rate, calculate:

a. The predetermined overhead rate.

b. The total cost, including direct materials, direct labor, and applied overhead, assigned to Patient A and Patient B.

2. Assuming McCullough calculates two overhead rates as recommended by the staff accountant, calculate:

a. The ICU and Other overhead rates.

b. The total cost, including direct materials, direct labor, and applied overhead, assigned to Patient A and Patient B.

3. What insights are revealed by the staff accountant’s approach?

Step by Step Answer:

One Predetermined Overhead Rate a The predetermined overhead rate is calculated as follows Predetermined Overhead Rate Fixed Overhead Costs Variable O...View the full answer

Introduction To Managerial Accounting

ISBN: 9781265672003

9th Edition

Authors: Peter Brewer, Ray Garrison, Eric Noreen