Let (left{X_{n}ight}_{n=1}^{infty}) be a sequence of independent and identically distributed random variables from a distribution (F) with

Question:

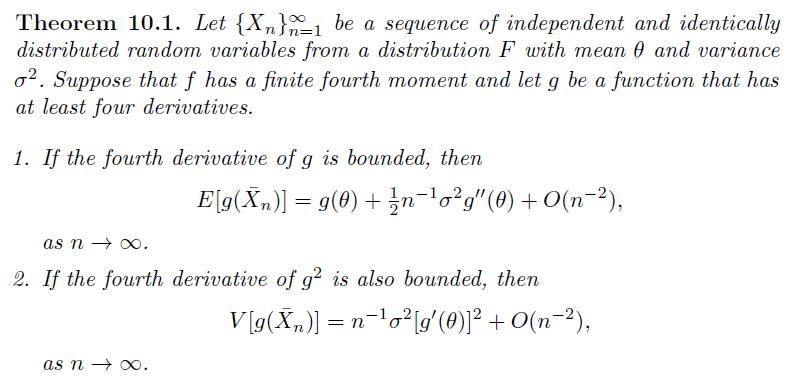

Let \(\left\{X_{n}ight\}_{n=1}^{\infty}\) be a sequence of independent and identically distributed random variables from a distribution \(F\) with mean \(\theta\) and finite variance \(\sigma^{2}\). Suppose now that we are interested in estimating \(g(\theta)=c \theta^{3}\) using the estimator \(g\left(\bar{X}_{n}ight)=c \bar{X}_{n}^{3}\) where \(c\) is a known real constant.

a. Find the bias and variance of \(g\left(\bar{X}_{n}ight)\) as an estimator of \(g(\theta)\) directly.

b. Find asymptotic expressions for the bias and variance of \(g\left(\bar{X}_{n}ight)\) as an estimator of \(g(\theta)\) using Theorem 10.1. Compare this result to the exact expressions derived above.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

ALBANUS MUTUKU

If you are looking for exceptional academic and non-academic work feel free to consider my expertise and you will not regret. I have enough experience working in the freelancing industry hence the unmistakable quality service delivery

178+ Reviews

335+ Question Solved

Related Book For

Question Posted: