Consider the ARDL ((2,1)) model with auxiliary AR(1) model (x_{t}=alpha+phi x_{t-1}+v_{t}), where (I_{t}=left{y_{t}, y_{t-1}, ldots, x_{t}, x_{t-1},

Question:

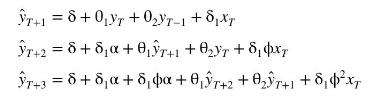

Consider the ARDL \((2,1)\) model

![]()

with auxiliary AR(1) model \(x_{t}=\alpha+\phi x_{t-1}+v_{t}\), where \(I_{t}=\left\{y_{t}, y_{t-1}, \ldots, x_{t}, x_{t-1}, \ldots\right\}, E\left(e_{t} \mid I_{t-1}\right)=0\), \(E\left(v_{t} \mid I_{t-1}\right)=0, \operatorname{var}\left(e_{t} \mid I_{t-1}\right)=\sigma_{e}^{2}, \operatorname{var}\left(v_{t} \mid I_{t-1}\right)=\sigma_{v}^{2}\), and \(v_{t}\) and \(e_{t}\) are independent. Assume that sample observations are available for \(t=1,2, \ldots, T\).

a. Show that the best forecasts for periods \(T+1, T+2\) and \(T+3\) are given by

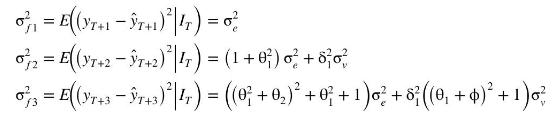

b. Show that the variances of the forecast errors are given by

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Anurag Agrawal

I am a highly enthusiastic person who likes to explain concepts in simplified language. Be it in my job role as a manager of 4 people or when I used to take classes for specially able kids at our university. I did this continuously for 3 years and my god, that was so fulfilling. Sometimes I've skipped my own classes just to teach these kids and help them get their fair share of opportunities, which they would have missed out on. This was the key driver for me during that time. But since I've joined my job I wasn't able to make time for my passion of teaching due to hectic schedules. But now I've made a commitment to teach for at least an hour a day.

I am highly proficient in school level math and science and reasonably good for college level. In addition to this I am especially interested in courses related to finance and economics. In quest to learn I recently gave the CFA level 1 in Dec 19, hopefully I'll clear it. Finger's crossed :)

2+ Reviews

10+ Question Solved

Related Book For

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim

Question Posted: