Consider the ARDL model Assume that (y_{t}) and (x_{t}) are I(1) and cointegrated. Let the cointegrating relationship

Question:

Consider the ARDL model

Assume that \(y_{t}\) and \(x_{t}\) are I(1) and cointegrated. Let the cointegrating relationship be described by the equation \(y_{t}=\beta_{1}+\beta_{2} x_{t}+e_{t}\).

a. Show that \(\beta_{1}=\delta /\left(1-\theta_{1}-\theta_{2}-\theta_{3}\right)\) and \(\beta_{2}=\sum_{r=0}^{5} \delta_{r} /\left(1-\theta_{1}-\theta_{2}-\theta_{3}\right)\).

b. Consider the corresponding error correction model \[

\Delta y_{t}=-\alpha\left(y_{t-1}-\beta_{1}-\beta_{2} x_{t-1}\right)+\phi_{1} \Delta y_{t-1}+\phi_{2} \Delta y_{t-2}+\sum_{r=0}^{4} \eta_{r} \Delta x_{t-r}+v_{t}

\]

Show that \(\delta=\alpha \beta_{1}, \theta_{1}=1-\alpha+\phi_{1}, \theta_{2}=\phi_{2}-\phi_{1}, \theta_{3}=-\phi_{2}, \delta_{0}=\eta_{0}, \delta_{1}=\alpha \beta_{2}-\eta_{0}+\eta_{1}\), \(\delta_{2}=\eta_{2}-\eta_{1}, \delta_{3}=\eta_{3}-\eta_{2}, \delta_{4}=\eta_{4}-\eta_{3}\), and \(\delta_{5}=-\eta_{4}\).

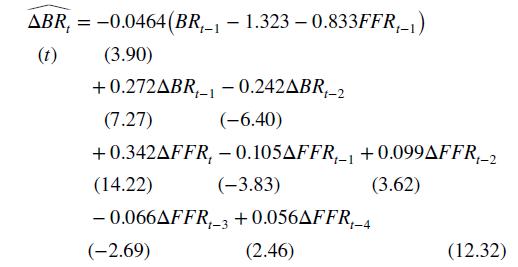

c. Using the data in usdata5, set \(y_{t}=B R_{t}\) and \(x_{t}=F F R_{t}\) and find least-squares estimates of the parameters in equation (XR12.18).

d. Use nonlinear least squares to estimate equation (12.32) in Example 12.9.

e. Substitute the parameter estimates of equation (12.32) obtained in part (d) into the expressions given in part (b) and compare the estimates you get with those obtained in part (c). What conclusion can you draw from this comparison?

Data From Equation 12.32:-

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim