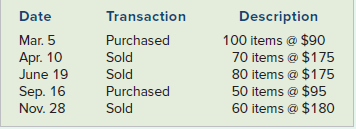

Donovan, Inc. had the following sales and purchase transactions during Year 2. Beginning inventory consisted of 120

Question:

Donovan, Inc. had the following sales and purchase transactions during Year 2. Beginning inventory consisted of 120 items at $80 each. Donovan uses the FIFO cost flow assumption and keeps perpetual inventory records.

Required

a. Record the inventory transactions in a financial statements model.

b. Calculate the gross margin Donovan would report on the Year 2 income statement.

c. Determine the ending inventory balance Donovan would report on the December 31, Year 2, balance sheet.

The ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =... Financial Statements

Financial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Donovan Inc Sales and Purchase Transactions for Year 2 Sales Purchases Cost of Goods Sold Inventory ...View the full answer

Answered By

Deborah Joseph

My experience has a tutor has helped me with learning and relearning. You learn everyday actually and there are changes that are made to the curriculum every time so being a tutor has helped in keeping me updated about the present curriculum and all.

I have also been able to help over 100 students achieve better grades particularly in the categories of Math and Biology both in their internal examinations and external examinations.

2+ Reviews

10+ Question Solved

Related Book For

Introductory Financial Accounting for Business

ISBN: 978-1260299441

1st edition

Authors: Thomas Edmonds, Christopher Edmonds

Question Posted: