The change in the annual spending rate, in conjunction with the boards expectations regarding future enrollment and

Question:

The change in the annual spending rate, in conjunction with the board’s expectations regarding future enrollment and the need for endowment support, could justify that KUE’s target weight for:

A. infrastructure be increased.

B. investment-grade bonds be increased.

C. private real estate equity be decreased.

Rebecca Mayer is an asset management consultant for institutions and high-net-worth individuals. Mayer meets with Sebastian Capara, the newly appointed Investment Committee chairman for the Kinkardeen University Endowment (KUE), a very large tax-exempt fund.

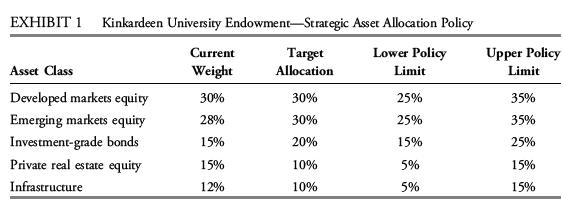

Capara and Mayer review KUE’s current and strategic asset allocations, which are presented in Exhibit 1. Capara informs Mayer that over the last few years, Kinkardeen University has financed its operations primarily from tuition, with minimal need of financial support from KUE. Enrollment at the University has been rising in recent years, and the Board of Trustees expects enrollment growth to continue for the next five years.

Consequently, the board expects very modest endowment support to be needed during that time. These expectations led the Investment Committee to approve a decrease in the endowment’s annual spending rate starting in the next fiscal year.

As an additional source of alpha, Mayer proposes tactically adjusting KUE’s asset-class weights to profit from short-term return opportunities. To confirm his understanding of tactical asset allocation (TAA), Capara tells Mayer the following:

Statement 1. The Sharpe ratio is suitable for measuring the success of TAA relative to SAA.

Statement 2. Discretionary TAA attempts to capture asset-class-level return anomalies that have been shown to have some predictability and persistence.

Statement 3. TAA allows a manager to deviate from the IPS asset-class upper and lower limits if the shift is expected to produce higher expected risk-adjusted returns.

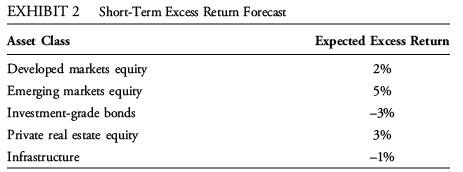

Capara asks Mayer to recommend a TAA strategy based on excess return forecasts for the asset classes in KUE’s portfolio, as shown in Exhibit 2.

Following her consultation with Capara, Mayer meets with Roger Koval, a member of a wealthy family. Although Koval’s baseline needs are secured by a family trust, Koval has a personal portfolio to fund his lifestyle goals.

In Koval’s country, interest income is taxed at progressively higher income tax rates.

Dividend income and long-term capital gains are taxed at lower tax rates relative to interest and earned income. In taxable accounts, realized capital losses can be used to offset current or future realized capital gains. Koval is in a high tax bracket, and his taxable account currently holds, in equal weights, high-yield bonds, investment-grade bonds, and domestic equities focused on long-term capital gains.

Koval asks Mayer about adding new asset classes to the taxable portfolio. Mayer suggests emerging markets equity given its positive short-term excess return forecast. However, Koval tells Mayer he is not interested in adding emerging markets equity to the account because he is convinced it is too risky. Koval justifies this belief by referring to significant losses the family trust suffered during the recent economic crisis.

Mayer also suggests using two mean–variance portfolio optimization scenarios for the taxable account to evaluate potential asset allocations. Mayer recommends running two optimizations: one on a pre-tax basis and another on an after-tax basis.

Step by Step Answer: